Key Points

- Our multi-year regime change thesis remains intact as companies and investors continue to adjust to relatively more persistent inflation and higher interest rates.

- We expect dislocation, volatility and skepticism to drive a wider dispersion of stock-price returns, which can present a favorable environment for well-resourced active managers.

- The team focuses on investments at the nexus of strong fundamentals, attractive valuations and catalyst-driven business momentum.

At the start of 2023, we highlighted several elements that would likely influence investor sentiment and drive market direction and returns, including persistent inflation and tighter monetary policy. While neither was a concern in the preceding decade, they are now important variables in investment decisions. In short, we viewed 2023 as a year of transition for both companies and investors as they adjusted to “free money” no longer being free.

Looking ahead to 2024, we believe inflation and monetary policy will continue to be important considerations and would now include slowing economic growth as an additional driver of investor sentiment and returns. Our outlook is increasingly cautious given the market’s apparent lack of consideration for these factors, and we believe there remains much uncertainty in the direction and outcomes for each. Furthermore, while the Federal Reserve (Fed) has successfully begun lowering inflation, we believe further intervention may be required to reach the Fed’s inflation target and achieve an economic soft landing.

From an investment perspective, “balance” is a fitting word to describe our current approach to the market given this uncertainty. That does not mean we lack conviction. Instead, we consider these macro factors as we evaluate companies and determine the best potential investment outcomes, being selective in where and when to be offensive and defensive. We believe a greater emphasis and focus on strong balance sheets and liquidity will be key to achieving this balance. As always, we favor companies sitting at the nexus of strong fundamentals, attractive valuations and catalyst-driven business momentum.

Are We There Yet?

Over the course of 2023, the Fed raised interest rates four times, the Consumer Price Index (CPI) continued to moderate from its June 2022 peak, and the US consumer remained resilient as evident in spending and employment data. Despite inflation remaining above the Fed’s target rate, its downward trajectory was enough to inspire confidence within equity markets as many investors felt the Fed would be successful in achieving its goal of an economic soft landing. As we close out the year, markets now appear to be signaling that inflation has been tamed, peak interest rates have been realized, and the Fed should start to cut rates next year.

Not So Fast

While the Fed’s aggressive monetary policy has dampened inflation, we believe it remains to be seen whether an economic soft landing can truly be achieved; controlling inflation while avoiding an economic recession could prove difficult for the Fed.

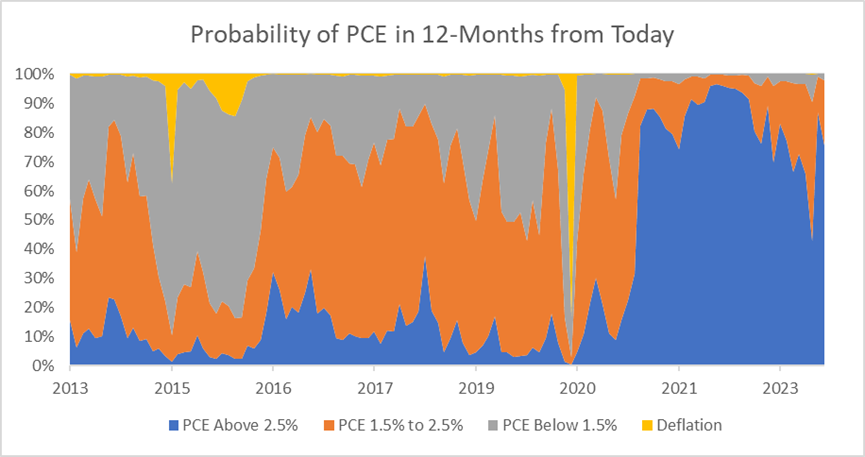

Despite some inflation moderation, prices continue to rise and are growing at a pace above the Fed’s target rate. According to its own data as shown in the graph below, there is still a relatively high probability that personal consumption expenditures (PCE), the Fed’s preferred gauge of inflation, will be above its target rate 12 months from now.

Probability of PCE in 12 Months from Today

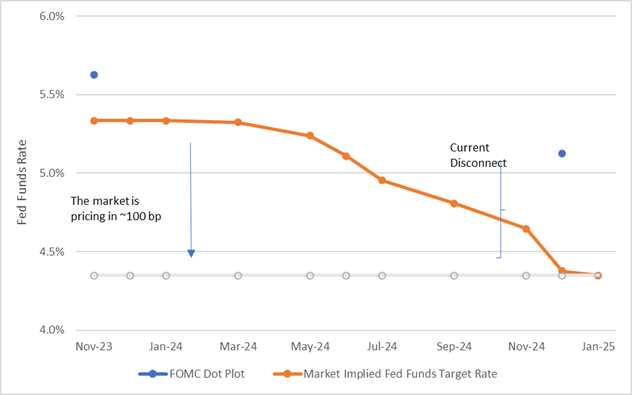

Meanwhile, financial markets are anticipating the Fed will cut interest rates by roughly 100 basis points over the course of 2024, completely reversing the 2023 increases—something it has not done in the last 30 years outside of the global financial crisis and the Covid pandemic. As shown in the graph below, when comparing the market’s expectations with the Federal Open Market Committee’s (FOMC) forecast for interest rates at the end of 2024, there is a roughly 75 basis point difference between them. We believe Fed Chair Powell is committed to achieving his inflation objective and therefore think rates will likely be higher than the market is current forecasting.

FOMC Expectations versus Implied Fed Funds Target Rate

We have seen this environment multiple times over the last two years. Financial markets, being forward-looking, are proactive and aim to position for what is next while the Fed, being data-dependent, is more backward-looking and reactive to what has already happened. These differing perspectives can often lead to dislocations between what the market thinks the Fed is going to do and what the Fed will actually do. The reconciliation of these dislocations often leads to periods of heightened volatility, which we expect to see throughout 2024—this is the basis of our balanced approach.

How to Position?

The silver lining of market volatility is that it often creates compelling investment opportunities. Heading into 2024, we are still finding more value in the financial, health care and energy sectors. Within financials, the varying degrees of cyclicality and market volatility among subsectors allow us to move within the broader sector to play offense or defense depending on economic and market momentum. In particular, we find the insurance space attractive as income from ‘float’ (money held by insurance companies that has not yet been paid out to claimants) has once again become more valuable. Within health care, there are several idiosyncratic opportunities in pharmaceuticals where business momentum has picked up among select names, while fundamentals and valuations within the medical-device space have grown very attractive. Decarbonization and energy transition are exciting long-term secular themes that we believe will benefit a number of traditional energy companies. In our view, this theme has largely overshadowed some company-level structural changes, making this an overlooked area of opportunity.

In addition to decarbonization and energy transition, we recognize a number of other secular themes that should likely provide tailwinds for select sectors and companies over the next year. These themes also inform our view that inflation should remain more persistent, and therefore a thorn in the side of the Fed. These themes include deglobalization (onshoring/reshoring), defense and destabilization (geopolitical risk), and divided wealth (populism/fiscal policy).

Above all, we believe an active, well-balanced process, with a focus on company fundamentals, valuations and catalyst-driven business momentum, is best suited for this environment. This can help sort through market skepticism and identify changes on the margin that can lead to better investment outcomes.

Authors

Newton US large cap value & income team

Insights from the Newton US large cap value & income team

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. Analysis of themes may vary depending on the type of security, investment rationale and investment strategy. Newton will make investment decisions that are not based on themes and may conclude that other attributes of an investment outweigh the thematic structure the security has been assigned to. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

Comments