Key Points

- Small-cap stocks may be well positioned to benefit from Federal Reserve (Fed) interest-rate cuts, as higher rates have challenged the asset class’s profitability and caused them to significantly lag their larger-cap counterparts.

- Initial public offerings (IPOs) are on the upswing; through the first half of 2024, 94 companies have gone public with $18.5 billion in capital raised, an 80% increase from the proceeds raised in the first half of 2023. Based on this data, the total number of IPOs in 2024 is projected to be 188 on an annualized basis, an improvement over 2022 and 2023 but still below the 254-per-year average of the last 20 years.1

- Despite challenges such as high interest rates, global economic shifts, employment trends and the upcoming US presidential election, US capital markets remain among the most robust worldwide. In our view, rate cuts and a stable, albeit slower-growing, economy following the election could support a further rebound in IPO activity in 2025.

In recent years, small-cap stocks have underperformed their larger-cap counterparts. Likewise, the initial public offering (IPO) market, which feeds fresh companies into the small-cap segment more than any other segment of the equity market, has been lackluster. Despite their lag in performance, small caps have always played an important role in portfolio diversification, providing investors with exposure to smaller but faster-growing companies with greater ties to the local economies in which they operate. Small-cap stocks are key to achieving proper diversification, particularly when paired with investments in larger, often slower-growing, multinational companies. Like large caps, small caps provide diversified exposure to equity markets, and, in our view, the relatively lower correlation between the two market-cap segments, historically, underscores the diversifying benefits of small caps.

Yet, over the last two decades as economic shifts have continued to reshape the financial landscape, small caps have largely been overlooked. In our view, this underdog scenario could present a compelling opportunity for investors, particularly in the new environment. The state of valuation discrepancies, monetary policies, interest rates and IPO activity all have implications for the small-cap market. As ongoing developments in the global economy continue to transform market dynamics, we believe that small caps are poised to benefit, with growing potential to capitalize on evolving opportunities.

As of July 10, we may have hit the start of an inflection between large and small caps. Is this a true pivot, or an anomaly? That is the question at hand. Nevertheless, in our view, the extended weakness in small caps, which is now in its 14th year by some estimates, is due for a correction.

Improving Market Conditions

We believe that multiple market conditions have aligned in a way that should favor small-cap stocks for the foreseeable future, especially given economic shifts that have ensued post pandemic. With the reopening of economies across the globe, and the resulting distortion in supply-demand dynamics, large-cap stocks have far outpaced their small-cap counterparts in valuation growth, leading to a disparity not seen since the dot-com bubble of the late 1990s. Interestingly, the technology sector has significantly contributed to the more recent upward trajectory of large-cap valuations, highlighting the skewed valuation dynamics across the broader market.

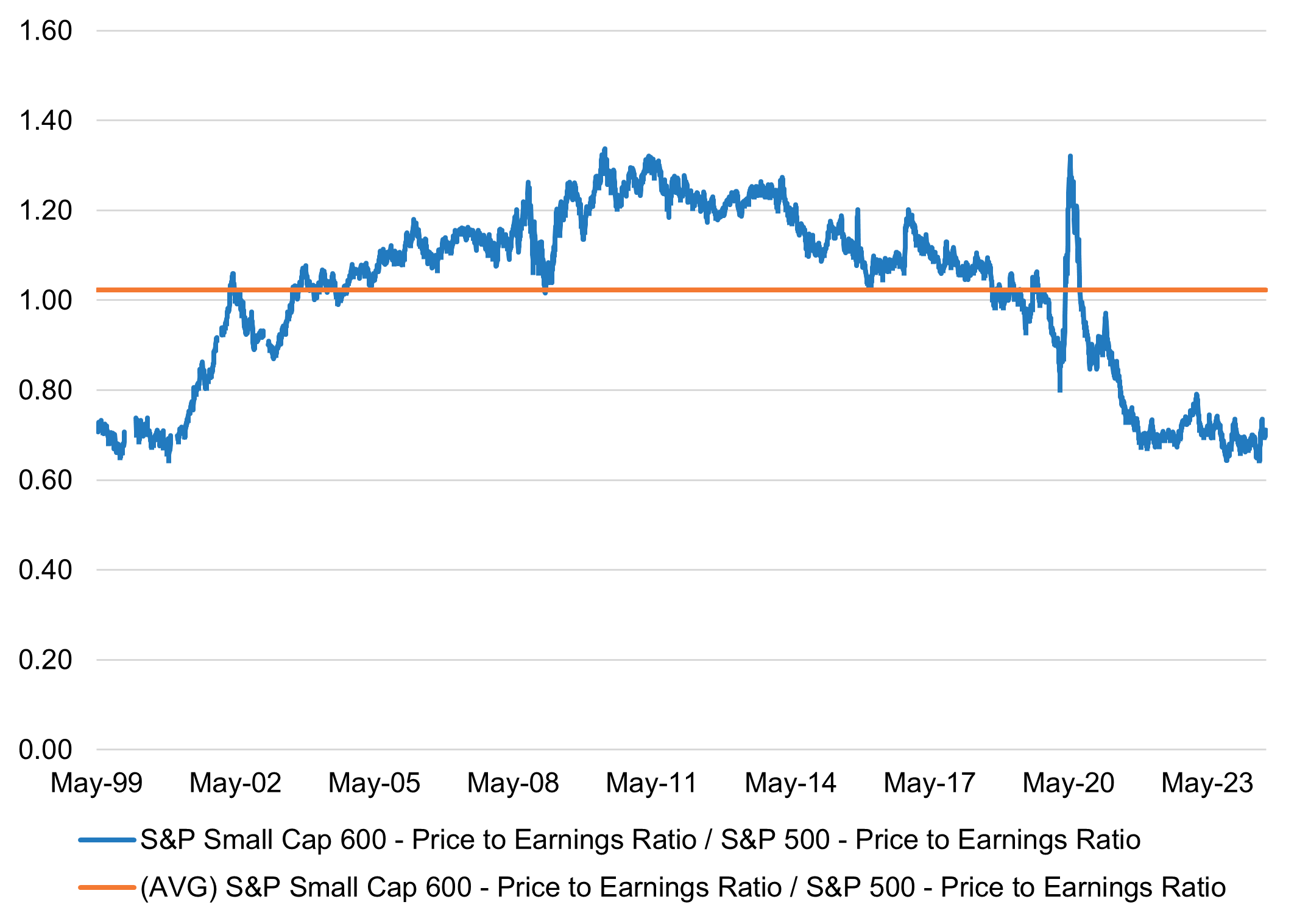

As the graph below illustrates, the current price-to-earnings (P/E) multiple discount of the S&P SmallCap 600® relative to the S&P 500® stands at around 0.71, compared to the long-term average of 1.02, which indicates that small caps are likely to be undervalued.

Forward Price to Earnings Premium/Discount (S&P 600 vs. S&P 500)

Source: FactSet. As of August 29, 2024.

This valuation gap presents an opportunity for small caps to potentially generate higher returns, as market forces attempt to correct this imbalance. At Newton, our dedicated small-cap analysts strive to consistently identify promising stocks that are often overlooked by the broader market to capitalize on these conditions. Despite the earnings-growth deceleration across small-cap companies in 2023, which was partially attributable to rising interest rates, we believe the combination of historically low valuations and potential for upward earnings revisions creates a more constructive investment environment for small-cap stocks. While small caps typically exhibit greater volatility, they also offer significant growth potential compared to their more established large-cap counterparts. This growth potential becomes especially attractive during market corrections, when undervalued small-cap companies can deliver substantial returns as valuations adjust.

At Newton, our dedicated small-cap analysts strive to consistently identify promising stocks that are often overlooked by the broader market to capitalize on these conditions.

Valuation Discrepancies: Public Versus Private Markets

Another notable valuation disparity exists between public and private markets. In recent years, private markets have witnessed a surge in both the number and value of deals transacted. This was especially true in 2021, when many private companies were accepting inflated valuations to emulate soaring public-market valuations. However, while public-market valuations have retreated from peak levels in recent years, private-company valuations have held relatively steady.

This divergence has created a challenging environment for dealmaking in the venture-capital world. Bid-ask spreads have widened, as management teams resist lowering valuations and investors sidestep inflated prices. Deal activity has slowed, and as a result conditions for limited partners have tightened. This scarcity of capital has particularly affected late-stage private companies, contributing to the growing backlog of companies waiting to go public; consequently, the IPO market has remained subdued. In our view, this backlog could potentially spawn considerable investment opportunities once market conditions become more favorable.

IPO Market Activity

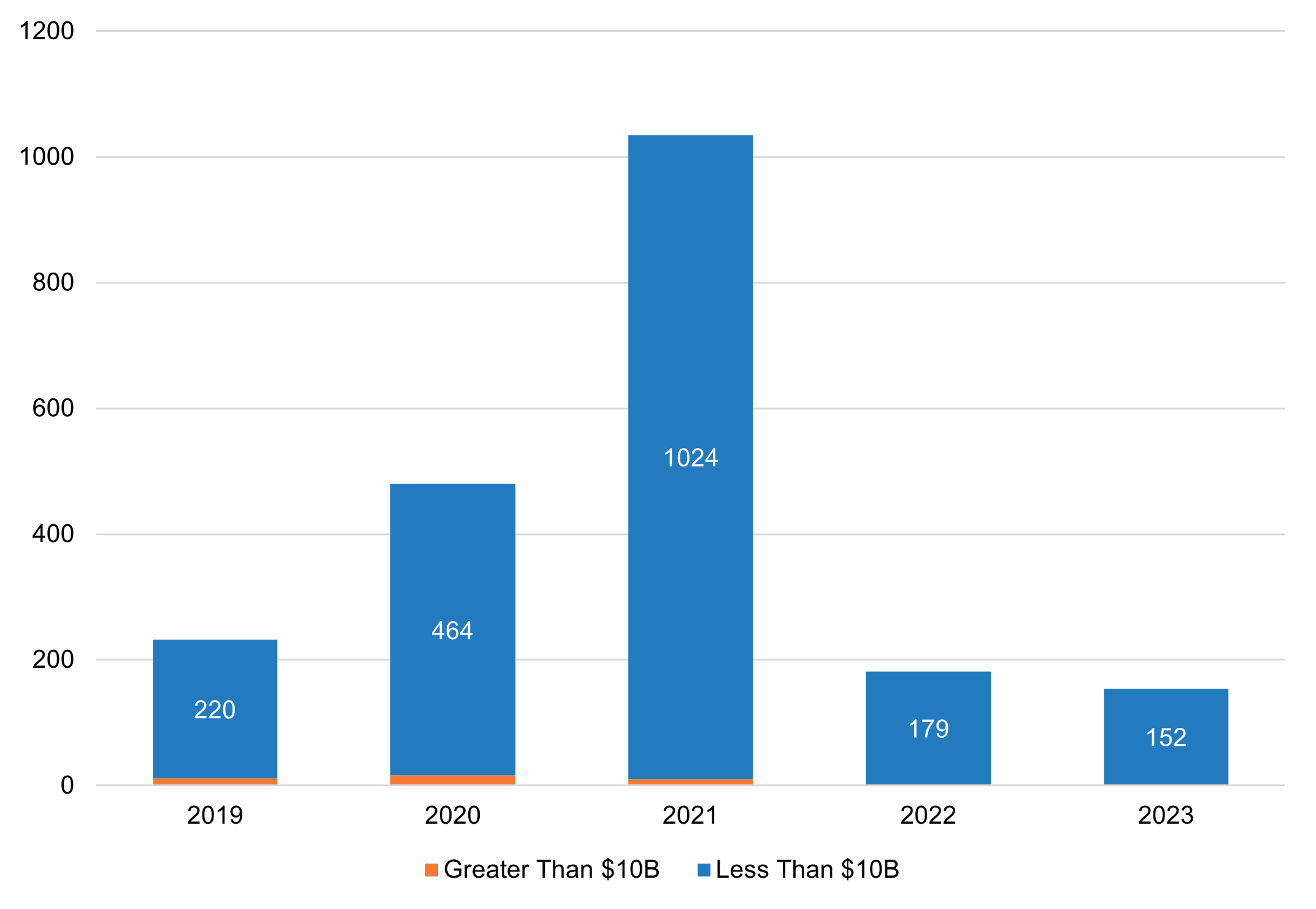

Over the last decade—with the exception of the 2021 boom in special purpose acquisition companies—the IPO market has been rather anemic. Many investors believe that IPOs tend to churn out new public companies at larger-cap valuations; on the contrary, IPOs are much more likely to feed directly into the small-cap market. As reflected in the chart below, which depicts the last five years of IPO activity by market cap, the majority of IPOs roll out at valuations of less than $10 billion.

Number of IPOs Last Five Years by Large Cap (>$10B) and Small-Mid Cap (<$10B)

Source: Stock Analysis, IPO Statistics. Data as of December 31, 2023.

Small Caps and IPOs

The relationship between the IPO market and small caps has always been symbiotic. Small-cap companies, which provide heavily idiosyncratic opportunities, are often relatively unknown to investors due to the lack of coverage by Wall Street. Street analysts are not just choosing to ignore small caps; there are simply too many companies to cover, particularly as research budgets have grown tighter over time.

The IPO market, which takes companies from being privately held to the public market, is an important feeder to the small-cap space. Despite pre-IPO roadshows and fanfare, public investors generally lack deeper knowledge into these companies, which often carry a heightened set of both risks and opportunities. Due to this lack of readily available information, small caps have typically represented one of the most fertile market segments for alpha generation across public equities.

A Brighter Outlook for IPOs

The IPO market is slowly showing signs of recovery, with a growing backlog of companies preparing to make their public debuts. Anticipated improvements in conditions surrounding inflation and interest rates are supporting the 2024 IPO outlook for the remainder of the year, though the US presential election and continuing geopolitical tensions could pose challenges. As market valuations normalize and bid-ask spreads narrow, the IPO market is expected to regain momentum either later this year or in early 2025. Historically, small caps have dominated the number of IPOs, suggesting that the resurgence of the IPO activity may introduce a new wave of small-cap companies into the market.

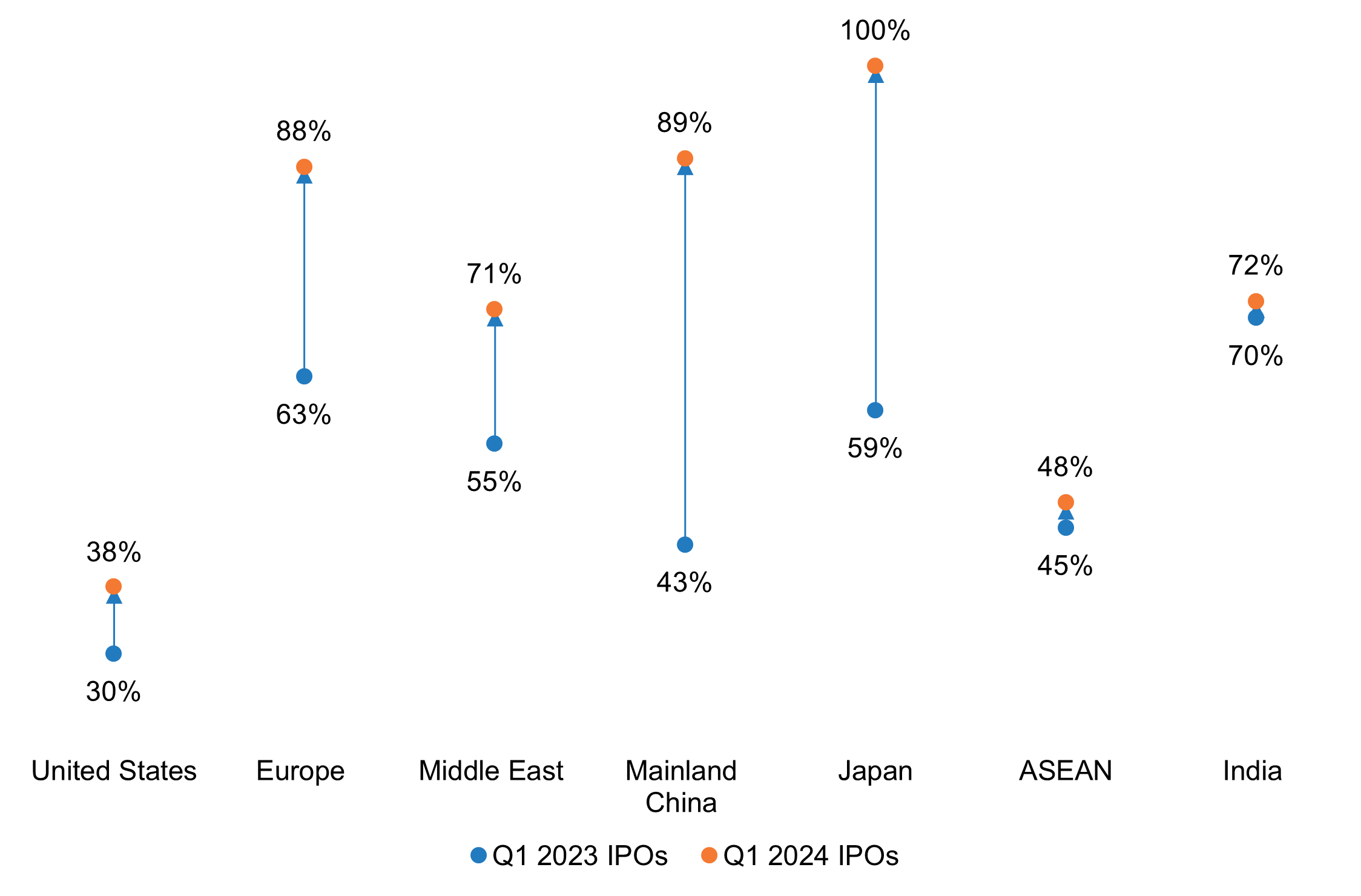

We believe a robust IPO market would benefit investors focused on small-caps stocks, providing access to a range of new companies with solid growth potential. The positive performance of recent IPOs, many of which have seen their stock prices exceed their offer prices (as depicted in the chart below), points to improving market valuations and investor sentiment toward riskier opportunities. A resurgence in the IPO market would also provide small-cap investors with enhanced liquidity, making it easier to buy and sell small-cap stocks, and thus leading to more efficient pricing in the market.

After-Market Performance by Region

Percentage of Current Share Price Above Offer Price

Data source: EY. As of March 27, 2024.

Interest Rates and Monetary Policy

Investor attention is currently focused on interest rates, with the Federal Reserve (Fed) announcing its decision to lower interest rates by half a percentage point on September 18, 2024. We believe small caps stand to benefit from a reduction in rates, as the decline in borrowing costs should offer greater relief to these companies that rely more heavily on external capital for funding their growth, expansion and innovation. Small-cap companies tend to be more exposed to higher interest rates, as they typically have higher leverage and more floating-rate debt than large caps.

Additionally, equities are usually more appealing to investors relative to fixed-income investments during periods of lower interest rates. Reduced interest rates help promote business expansion and assist in enhancing profitability for small-cap companies, making them a potentially attractive growth opportunity. Reduced borrowing costs could allow these companies to invest in new projects and expand operations more accessibly.

A Compelling Opportunity for Small Caps

In our view, the current market environment presents a compelling opportunity for small-cap companies. Due to the valuation disparities that exist between large and small caps, and between public and private markets, we believe that small caps could potentially outperform their large-cap counterparts in the future. We believe improvements in conditions surrounding interest rates and inflation could further benefit small caps. Additionally, the resurgence of the IPO market, which fuels the small-cap segment more than any other cap segment with new companies, underscores the potential for significant returns and highlights that this may be an opportune time to invest in small caps.

1 IPO Trends: First Half of 2024 and Beyond, Stout, August 26, 2024, https://www.stout.com/en/insights/article/ipo-trends-first-half-2024-beyond

Authors

John Porter III

Chief Investment Officer

George Saffaye

Global investment strategist

Meghan Bruni

Investment strategist

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR006613 Exp 09/29. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.