Key Points

- Historical analysis indicates that when interest rates bottom following a rate-cutting cycle, the value index often experiences a greater percentage increase in 12-month forward earnings-per-share (EPS) estimates relative to the growth index.

- Value stocks generally outperform growth stocks in both rising and falling rate periods.

- The large-cap value universe typically contains companies with established earnings and robust cash flows, making them potentially more resilient in economic downturns.

- Value stocks tend to have lower valuations as they are less reliant on optimistic future growth expectations, providing a necessary buffer against market fluctuations.

The Federal Reserve’s (Fed’s) monetary policy has long been a force in shaping economic conditions and influencing financial markets. In addition to determining borrowing costs, the Fed’s interest-rate moves have historically had an impact on investment strategies and overall market performance. Over the last few years, the global pandemic, geopolitical tensions and supply-chain disruptions have also affected the investment backdrop, driving meaningful changes.

The Fed’s 50-basis-point rate cut in September had been a long-awaited and highly anticipated move, and rightfully so. Marking the first in four years, the rate cut was followed by a second cut of 25-basis points in November. These decisions, aimed at alleviating economic pressures, came amid an uncertain and volatile investment landscape. The first rate cut shifted market expectations, prompting investors to begin adjusting their portfolios to prepare for a potential ‘soft landing,’ in hopes that the Fed could circumvent a US recession. The second cut immediately followed the election of Donald Trump as the 47th US president. Post election, the 10-year Treasury rate has advanced, and market expectations for further aggressive cuts in interest rates have softened. In our view, if Trump’s policies prove to be inflationary, the bottoming of the rate-cutting cycle could come sooner than previously anticipated.

Where can investors turn for stability in this complex environment? We believe that strategically allocating capital to US large-cap, value-oriented stocks could be a compelling option.

History Can Rhyme

Our global research team employs a bottom-up, fundamentals-based research process. While our approach is largely centered on fundamentals, our research team also recognizes the importance of understanding how macroeconomic factors, such as interest-rate changes, can distinctly affect industry conditions.

In our view, history may not repeat itself to a tee, but it can sometimes rhyme. Thus, we thought it would be prudent to examine previous cycles of significant rate cuts, given the rate cuts projected between September 2024 and September 2025; in particular, we analyzed cycles when cuts in interest rates exceeded 200 basis points in a one-year period. Given that material cuts in interest rates over a relatively short period of time are usually associated with slowing economic growth (or the potential for it), we found that strategically allocating capital to US large-cap, value-oriented stocks could be beneficial for investors given their historical resilience, relatively more attractive valuations, and the potential for earnings downgrades.

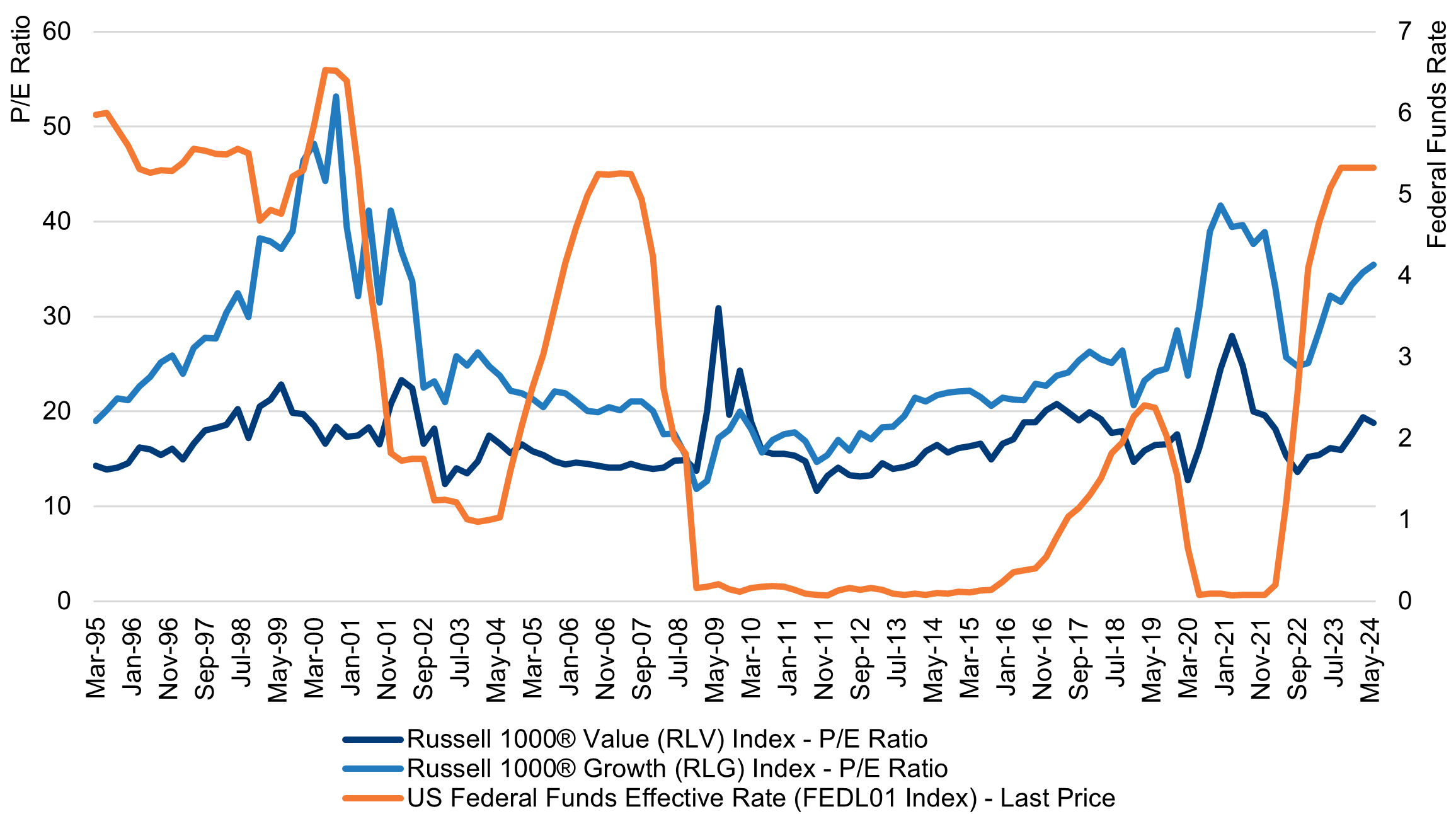

High Growth Valuations Amid Economic Uncertainty

In our opinion, attempting to time the market using valuation data is a futile exercise. However, valuations can help analysts and portfolio managers better understand company-specific factors in a broader context. Investors are currently navigating a landscape marked by exceptionally elevated valuations, particularly within high-profile growth stocks such as the ‘magnificent seven,’ which have contributed substantially to recent market gains. This surge has caused average price-to-earnings (P/E) ratios to exceed historical norms, reminiscent of the dot-com bubble when many technology stocks were valued at P/E ratios of above 50 times earnings. These heightened valuations, which contrast with the largely steadier valuations of larger-cap value-oriented investments, could prompt the market to adjust its expectations. This may be an opportune time for investors to reassess their allocations and consider the benefits of increasing value exposure to balance an investment strategy.

Against this backdrop, growth investors may be overexposed to stocks that are trading at unsustainable levels and susceptible to multiple contractions. During the dot-com bubble, P/E ratios for the Russell 1000® Growth (RLG) Index reached over 50 times earnings. Current ratios sit at around 35 times earnings, which is still far above the RLG index’s long-term average of 21 times earnings. Following the bursting of the dot-com bubble, P/E valuations for the RLG index plummeted, as depicted in the chart below. With P/E ratios for the index climbing to similar levels today, we believe now is a good time for investors to consider some diversification within their equity allocations.

This may be an opportune time for investors to reassess their allocations and consider the benefits of increasing value exposure to balance an investment strategy.

Price-to-Earnings (P/E) Ratios Through Time

Source: Newton Investment Management, Bloomberg, as of June 28, 2024.

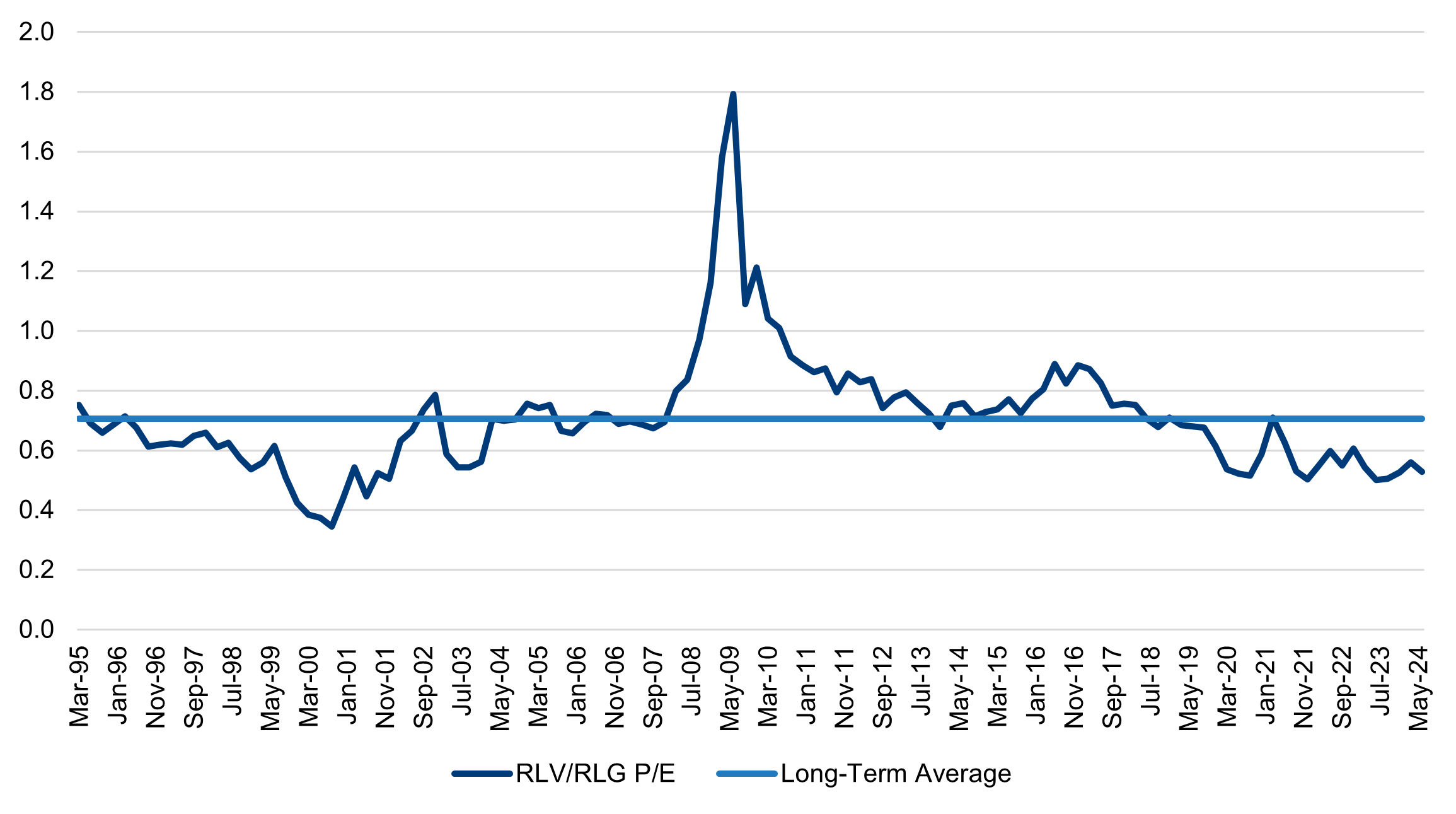

The Undervaluation of Value Stocks

The chart below shows the valuations of the Russell 1000® Value (RLV) Index relative to the RLG index over the last 30 years. Viewing these relative valuations throughout history highlights how undervalued value stocks are compared to growth stocks; currently, the discount sits at 0.53 versus the long-term average of 0.71. As market sentiment shifts, value stocks, and particularly those trading at low multiples, could see heightened interest from investors.

Premium/Discount for Price-to-Earnings (P/E) Ratio: Russell 1000® Value (RLV) Index Vs. Russell 1000® Growth (RLG) Index

Source: Newton Investment Management, Bloomberg, as of June 28, 2024.

Estimate Revisions

In our opinion, the graph below further supports a strategic shift to increased large-cap value exposure. Historical analysis indicates that when interest rates bottom following a rate-cutting cycle, the RLV index often experiences a greater percentage increase in 12-month forward earnings-per-share (EPS) estimates relative to the RLG index. Given the likelihood that Trump implements policies that prove to be inflationary, this trough in the rate-cutting cycle could come sooner than initially expected. Following the bottoming of interest rates in the aftermath of the 2008 global financial crisis, the RLV index saw an increase of 84% in 12-month forward EPS estimates, while the RLG index saw gains of 47%. Similarly, following the end of the rate-cutting cycle in 2020, the RLV index saw 12-month forward EPS estimate growth of 53%, while the RLG index saw growth of 37%.

12-Month Forward Earnings-Per-Share (EPS) Estimates

Source: Newton Investment Management, Bloomberg, as of June 28, 2024.

Continuing economic uncertainty exacerbates this risk of earnings revisions. Currently, US real gross-domestic-product (GDP) growth is expected to slow from above trend in 2024 to below trend in 2025; in addition, real income growth has softened, and the labor market is showing signs of cooling.1

The Resilience of Large-Cap Value

Amid the continuing uncertainty and shifting interest-rate dynamics, large-cap value stocks have consistently demonstrated their resilience across various market conditions. In analyzing performance of the cheapest 30% of US stocks versus the most expensive 30% of US stocks sorted by price-to-book ratio during previous rate cycles, research reveals an interesting dynamic: value stocks generally outperform growth stocks in both rising and falling rate periods. In nine out of the 11 periods of falling rates analyzed, value outperformed growth.2 This consistent outperformance supports our conviction in the enduring strength of US large-cap, value-oriented stocks. It also underscores the appeal of value stocks as a long-term investment strategy, especially given the unpredictability of the current environment.

The stability of value stocks offers several advantages in times of market volatility. The large-cap value universe typically contains companies with established earnings and robust cash flows, making them more resilient in economic downturns. Value stocks tend to have lower valuations as they are less reliant on optimistic future growth expectations, providing a necessary buffer against market fluctuations, as we mentioned in our previous blog post. Additionally, the Fed has embarked on what is expected to be a steady series of interest-rate cuts, and although this rate-cutting cycle could be shorter than initially expected, it makes the dividends offered by many value stocks more attractive, particularly in low interest-rate environments when investors seek steady income and growth over time in favor of fixed-income investments.

Positioning for Future Success

We believe that the current economic climate, marked by inflated growth-stock valuations, the potential for earnings revisions and the historical strength of large-cap value stocks, presents a compelling case for large-cap value investing. By strategically allocating to larger-cap, valued-oriented stocks, investors may find some stability and growth amid the uncertainty of the investment landscape.

Our approach, focused on finding value at the intersection of strong and improving fundamentals, attractive valuations and positive business momentum, positions us to benefit from these strengths as the landscape continues to evolve. We believe large-cap value investments allow us to capitalize on current market dynamics, while also providing a level of protection against inevitable fluctuations in the future environment. In our view, as markets continue to adjust to interest-rate changes and the potential for economic shifts, large-cap value stocks stand out as a pillar of resilience.

1 Economic Outlook US Q4 2024: Growth and Rates Start Shifting to Neutral, S&P Global, September 24, 2024, https://www.spglobal.com/ratings/en/research/articles/240924-economic-outlook-u-s-q4-2024-growth-and-rates-start-shifting-to-neutral-13258419

2 History Bodes Ill for Growth Stocks After Big Rally: Nir Kaissar, Bloomberg Opinion, January 2, 2024

Authors

Chris Hazelton

Global investment strategist

Meghan Bruni

Investment strategist

Newton US large cap value & income team

Insights from the Newton US large cap value & income team

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR006856 Exp 11/29. For additional Important Information, click on the link below.