Key Points

- We continue to see the potential for volatility, with rising inflationary pressures, geopolitical risks and monetary policy acting as key factors shaping market dynamics.

- Companies that pay and grow dividends tend to be more resilient in downturns as investors seek stability in uncertain times.

- As the market evolves, we will remain focused on delivering steady income and growth potential, ensuring we are prepared for what the year ahead may bring.

2024 has been characterized by pronounced volatility, affecting everything from interest-rate fluctuations and inflation expectations to the economic implications of artificial intelligence and shifting political landscapes. Heading into 2025, much of this uncertainty is likely to persist. With inflation remaining above pre-pandemic levels and geopolitical tensions continuing, the market faces continued dislocation. Amid these challenges, we remain steadfast in our balanced, risk-adjusted and dividend-focused approach, which is designed to deliver stability and competitive returns in volatile environments.

Inflation Unfolding

From a global perspective, the current environment is characterized by disinflationary growth, with inflation rates decreasing from the peak levels of 2022. However, there are concerns that inflation could pick up again in 2025, primarily due to President-elect Trump’s anticipated tariffs and their impact on the prices of goods and services. We anticipate that inflation should remain above consensus expectations, gradually rising from mid-2025 and ending the year between 2.5% and 3%.

The Second Act: A Stage Set for Uncertainty

Trump’s second term introduces additional ambiguity surrounding the future of interest-rate adjustments. While Jerome Powell remains Federal Reserve (Fed) Chair until 2026, Trump’s proposed policies could complicate interest-rate positioning for the central bank. We believe the Fed will largely overlook the increase in inflation, particularly if there is no substantial response from wages, indicating no second-round effects.

The market has already begun pricing in fewer interest-rate cuts as pro-growth policies could slow the rate-cutting process. We foresee the Fed’s cutting cycle in 2025 to be shallow and potentially paused early, with the federal funds rate likely settling around 3.75-4% by year end, aligning with current market pricing. We expect 10-year yields to trade near 4.5%, above the consensus forecast of 4.1%.

The risks to inflation and yields hinge on economic growth trends. If disinflationary growth deteriorates into deflation, we could see commodity prices fall, especially oil, which would likely push yields lower. Conversely, if the Trump administration pressures the Fed for aggressive easing and increases fiscal spending, bond markets may react negatively, causing yield-curve steepening and market volatility. Both scenarios are plausible in 2025.1

Heading into the coming year, we remain vigilant, understanding that continued volatility could lead to periods of heightened uncertainty, as well as opportunities for well-positioned investment strategies. We acknowledge the higher probability that inflation could persist, but we are prepared to manage these risks through our portfolio construction and broad risk controls.

As inflationary pressures and market volatility are expected to persist into 2025, a dividend-focused approach may prove even more valuable. In our view, dividends offer an essential hedge against inflation and provide a more reliable income stream, marking them as a key component of our strategy in uncertain times.

The Changing Appeal of Dividend Yield

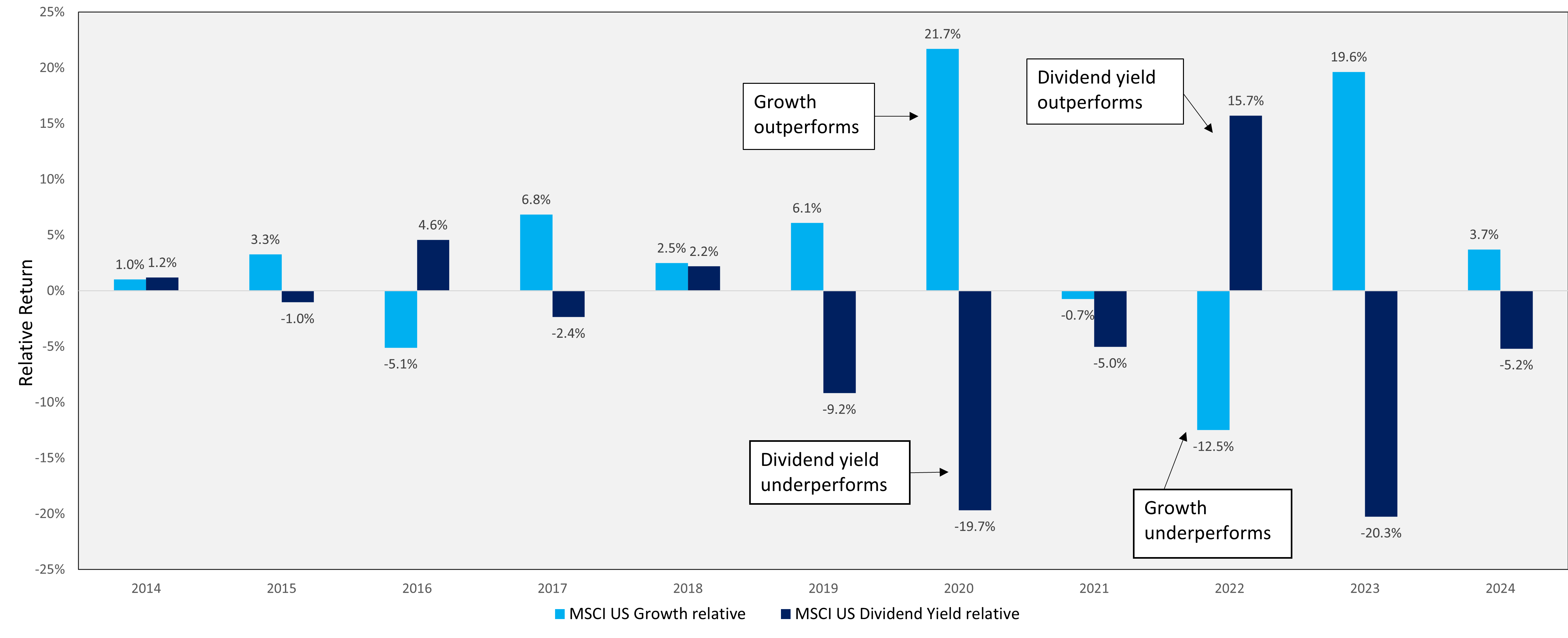

The demand of dividend-paying stocks is influenced by broad market investor sentiment. For much of 2024, dividend-paying stocks underperformed as investors favored high-growth companies. The shift from risk-on to risk-off and back to risk-on exemplifies the market’s current uncertainty.

As demonstrated in the chart below, the preference for dividend yield tends to undergo fluctuations over time. During phases when dividend-paying stocks lose their appeal, often due to a heightened focus on growth stocks, carefully designed risk controls can help investors adeptly navigate the shifting market sentiments, ensuring that portfolios remain resilient and well-positioned for long-term success

Shifting Investor Preference between Growth and Dividend Yield: MSCI Relative Returns

(December 31, 2014 – September 30, 2024)

Source: MSCI, as of September 30, 2024.

Why Dividends Are Set to Shine

The opportunity set within the S&P 500® has grown as more high-growth sectors, particularly information technology, health care and industrials, have seen an increased adoption of dividend payments. As of September 2024, around 80% of S&P 500 companies pay dividends, with 24% of those in the technology sector, up from 13% a decade ago. This shift highlights that growth and income can go hand in hand.2

Dividend-focused investing is particularly compelling in today’s market. Companies that pay and grow dividends tend to be more resilient in downturns as investors seek stability in uncertain times. These companies also have the ability to increase payouts in line with or above inflation, making them an appealing choice for income-focused investors. In a low interest-rate environment, where bond yields are less attractive, dividend paying stocks become even more compelling. With inflation remaining above pre-pandemic levels and potentially moving higher, these stocks are an effective hedge, further enhancing their appeal. Dividends remain a powerful tool for mitigating volatility, providing steady income and serving as a hedge against inflation.

Equities hold a unique advantage in their ability to adjust for inflation, unlike bond yields which remain static. Despite the current dividend yield standing at approximately 2.1%, and bond yields at around 4.2%, the S&P 500 has returned 28.1% year to date (through November 30, 2024), far surpassing the bond yield. This stark difference underscores the potential of equities not only to keep pace with inflation but also to significantly outstrip it, thereby preserving and enhancing the investor’s buying power. In contrast, bond holders may see their purchasing power eroded in an inflationary environment, making dividend-paying equities an even more compelling choice for those seeking both income and growth.

Looking Ahead to 2025

As we look to the year ahead, we continue to see the potential for volatility, with rising inflationary pressures, geopolitical risks and monetary policy as key factors shaping market dynamics. The ever-shifting developments surrounding these factors could drive uncertainty, but they may also create opportunities for investors focused on high-quality companies with reliable dividends. We remain committed to identifying these companies, maintaining a disciplined, dividend-focused approach as we traverse the uncertainty that lies ahead. As the market continues to evolve, we will remain focused on delivering steady income and growth potential, ensuring we are prepared for what the year ahead may bring.

1 Source: BNY Advisors Investment Institute.

2 https://www.ftinstitutionalemea.com/articles/2024/equity/four-reasons-dividends-matter-now

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR006962 Exp 12/29. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.