Key Points

- We believe investors should consider European infrastructure for greater diversification due to favorable valuations and lower exposure to the expensive artificial intelligence (AI) boom in the US.

- Tailwinds for European utilities include government incentives, sector dislocation and rising investment in energy independence.

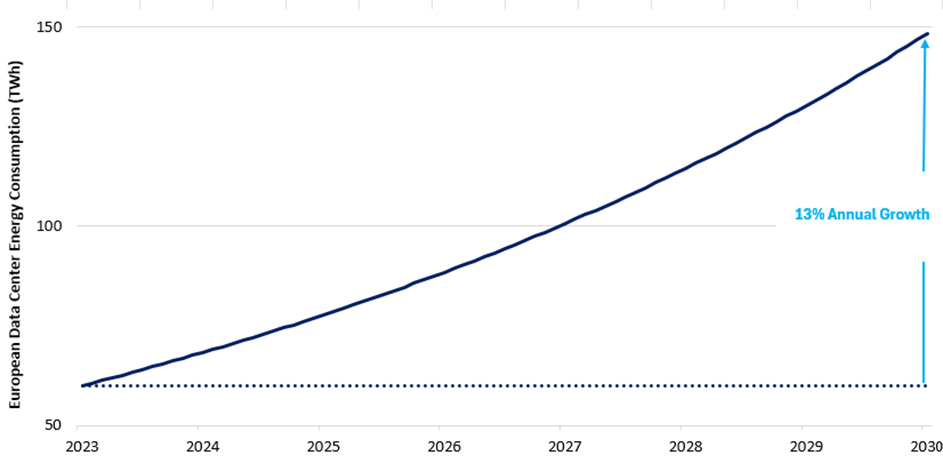

- Data-center growth is likely to drive significant power demand, creating long-term revenue growth opportunities for utilities and accelerating green-energy investments.

- The Nordic countries, due to their renewable-energy resources, cold climate and strong regulatory frameworks, are well positioned to benefit from the data center and AI boom.

In last year’s blog post, Coming to America: Investing in Utilities, we highlighted the tailwinds for US utility companies that included significant sector dislocation, government decarbonization incentives and investments in energy. However, the winds of change are at work once again, with the same drivers now appearing in Europe. We believe that investors should consider greater exposure to European infrastructure.

The Death of Equity Diversification–A Decade in Review

Global equities have recently hit a series of new all-time highs, as measured by the MSCI World Index, but returns have been led by a handful of large US growth stocks—the ‘magnificent seven’—whose performance has been driven by the promise of future growth from artificial intelligence (AI). These seven stocks have contributed 30% to global equities’ cumulative return of 155% over the past ten years through December 31, 2024, despite comprising only 11% of the benchmark, on average, during the period. The US has contributed 75% of the total returns with an average weight of 56%, while the US information technology sector has contributed 38% of global equity returns, with an average weight of 19%.

Not surprisingly, over the past ten years the US grew from 51% of the global equity market to 65%, while Europe decreased from 22% to 14%. Information technology increased from 14% to 26% of the MSCI World Index, while the combined weight of the industrials, utilities, energy and materials sectors fell from 27% to 20%.

The narrowness of the market rally was even more pronounced in the US, where the magnificent seven stocks contributed 29% of the S&P 500® Index’s cumulative 242% return over the previous ten years through December 31, 2024. The information technology sector grew from 19% of the S&P 500 to 33% over the same period and contributed 42% of S&P 500’s return despite an average weight of 25%. Together, the weight of the industrials, utilities, energy and materials sectors has fallen from 25% of the S&P 500 ten years ago to 15.5% at the end of 2024. The four infrastructure-exposed sectors started 5% bigger than information technology and ended 17% smaller.

New record highs would suggest that the entire US equity market is expensive. However, lack of market breadth has been the key story of the equity rally. The substantial weighting of these stocks has posed a challenge for investors who rely on the S&P 500 for diversification. Specifically, infrastructure stocks have become notably underrepresented within a typical S&P 500 equity allocation.

We suggest that investors seeking greater diversification should consider the infrastructure sector and specifically should look to European infrastructure where valuations have not been amplified by the expensive AI power boom.

2024 in Review

In the year since we published Coming to America: Investing in Utilities, in which we laid out our case for infrastructure investment within the US, the valuation dispersion between US and European utilities has grown. Over the calendar year 2024, the S&P 500 utilities sector appreciated 27% while European utilities were flat. A key driver of the US appreciation and relative outperformance was the significant capital expenditure of US mega-cap technology companies to support the build-out of the AI ecosystem. These investments in infrastructure, especially related to power, show no signs of stopping. Independent power producers and electric-utilities companies have been among the biggest beneficiaries due to the rising demand for electricity. Hyperscalers’ willingness to secure power at above-market rates also plays a role as they seek to ensure the powering of large data centers in support of their AI aspirations.

So, why do we believe now is a good time to allocate to Europe?

European Competitiveness

The key reasons we believe there is opportunity for active managers in European utilities are identical to the reasons we were bullish on the US in 2024:

- Government incentives aimed at decarbonization can provide tailwinds for renewables-exposed utilities.

- We believe there is a significant sector dislocation in European utilities, potentially unlocking opportunity for active managers.

- We believe electrification and investments in energy independence may continue to drive European electric and gas utilities.

European Government Support

We believe that infrastructure support for AI is a global goal essential for maintaining competitiveness in leading-edge technology. In addition, due to data privacy concerns, we believe countries will want to control their own technology and data, which will require them to build data centers domestically. Europe has fallen behind technology leaders in the US and China, and European officials have become more vocal about the need to act. In January 2025, the areas we feel could provide support for European utilities, initially through sentiment and then through revenue and earnings growth, were outlined in the European Commission’s report, A Competitiveness Compass for the EU. In the report, the Commission concludes that Europe “must act now to regain its competitiveness and secure its prosperity.” It cites Europe’s inability to keep pace with other major economies over the past two decades, especially relative to the US in advanced technology owing to a lack of innovation and high regulations.[1] The report outlines key areas of focus and newly instituted acts for the next five years to “reignite economic dynamism,” which we believe will benefit European utilities and other infrastructure companies:

AI Factories Initiative, Q1 2025, and EU Cloud and AI Development Act, Q4 2025-Q1 2026: “Europe needs the computing, cloud and data infrastructures that AI leadership requires…the initiative establishes ‘AI factories’ to boost Europe’s computing power… the Commission will mobilize public and private initiative to establish new AI Gigafactories specialized in training of very large AI models enabling key AI ecosystems throughout the EU.”

Digital Networks Act, Q4 2025: “Closing the innovation gap will require investment in state-of-the-art digital infrastructure, including modern fiber networks, wireless and satellite solutions, investments in 6G and cloud computing capabilities… To correct course, a Digital Networks Act will propose solutions to improve market incentives to build the digital networks of the future.”

Industrial Decarbonization Accelerator Act, Q4 2025, and Electrification Action Plan and European Grids Package, Q1 2026: “This dependence (reliance on fossil fuel for 2/3 of its energy) can only be reduced over time, as a greater share of energy is produced from decarbonized generation in Europe. The EU must thus accelerate the clean energy transition and promote electrification” and “Europe must invest more in modernizing and expanding its network of energy transmission and distribution infrastructure, accelerating investment in electricity, hydrogen and carbon dioxide transport networks as well as storage systems.”

Valuations Favor Europe

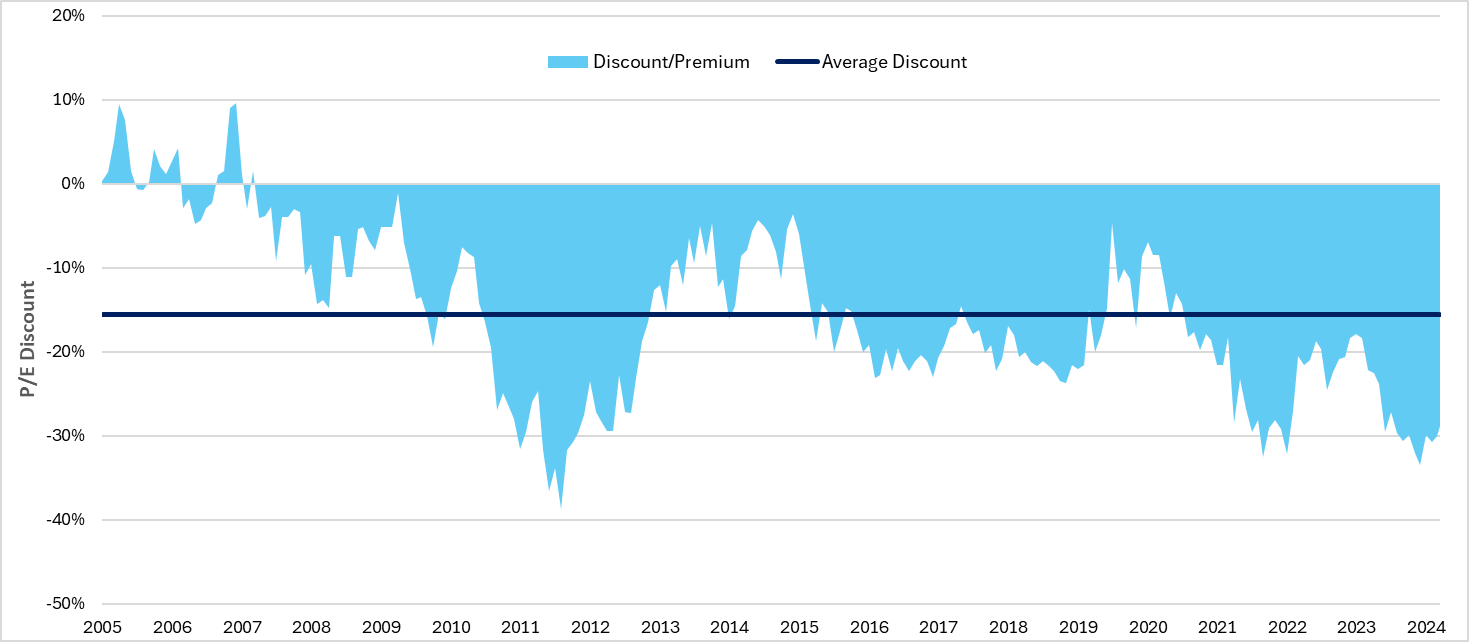

In the past 11 months, price-to-earnings (P/E) ratios of US utilities have rerated by 17% versus 3% for their European counterparts. European utilities currently trade at a 31% P/E discount relative to US utilities, which is more than twice as large as the long-term average of 15%.

European Utilities P/E Discount (-) / Premium (+) Relative to US Utilities

Yield Spreads

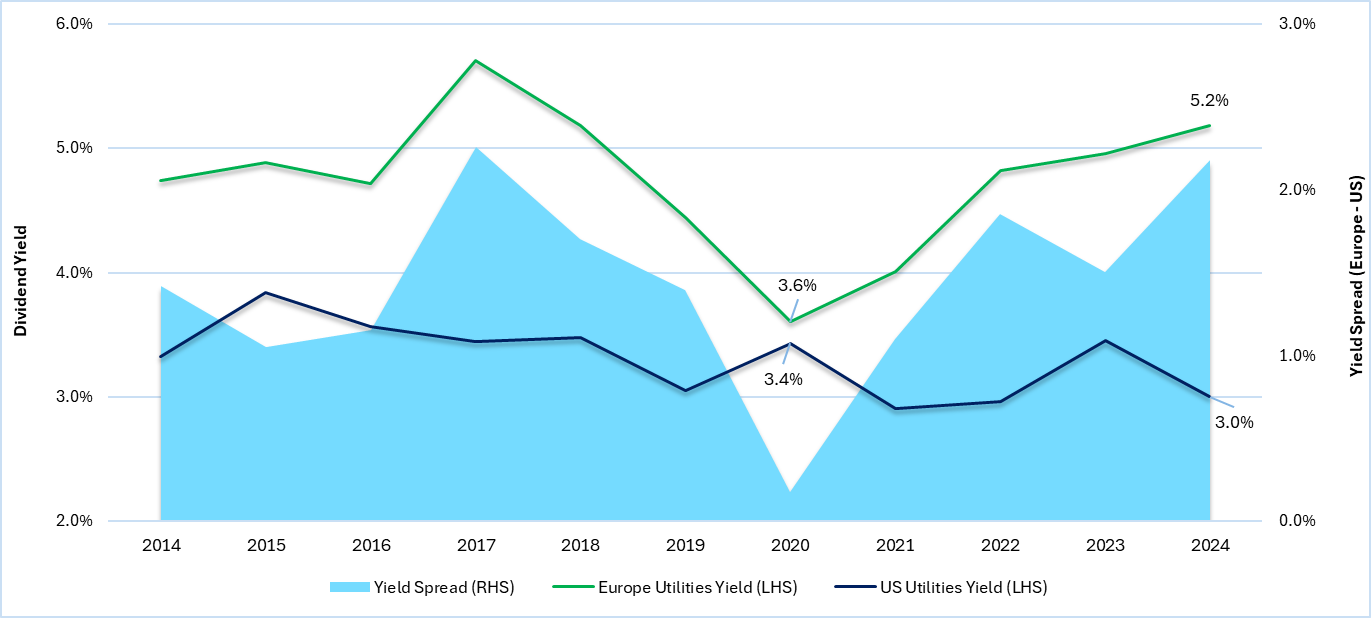

Given the movement in markets, the spread between dividend yields of European and US utilities has moved from 20 basis points (bps) to 220 bps over the past four years, creating opportunities to find promising value investment opportunities in the European utilities sector. This is especially pertinent given the secular tailwinds we expect in the coming year(s), which are identical to the tailwinds that are currently playing out in US markets and driving shares across the infrastructure space.

Dividend Yields and Spread: US vs. Europe

Based on the strength of the US utilities sector driven by the AI power boom, and relative valuations, we have increased our conviction within Europe.

Data Centers Should Create Value

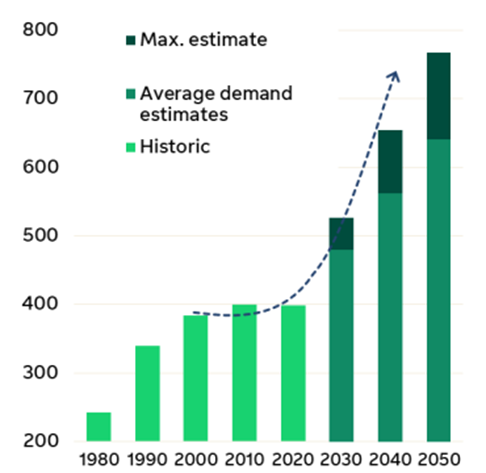

Data-center power demand is surging as the need for greater computing power grows, driven by digitalization, cloud migration and AI. AI is a major contributor to this demand due to its significantly higher power-density requirements stemming from the latest generation of graphics processing unit (GPU) chipsets.

While the growth in data-center build-out may likely be strongest in the US, Europe has ample opportunity to grow its market and further stimulate its technology ecosystem in three key areas:

Increased electricity demand: Data centers are likely to drive a significant rise in power consumption, creating long-term revenue growth opportunities for utilities.

Acceleration of green-energy investments: The shift toward sustainability will spur investment in renewable energy, grid modernization and energy storage solutions.

New infrastructure development: Expanding transmission networks and upgrading substations will be necessary, creating opportunities for infrastructure projects.

Power Demand for Data Centers is Projected to Rise Materially in Europe

Utility companies that proactively invest in renewable energy, grid capacity and innovative solutions like demand response and energy storage should be well positioned to capitalize on data-center growth. Strategic partnerships with data-center operators and governments will also be crucial to ensuring a stable and sustainable power supply. The most successful European utilities will likely be those that can balance rapid infrastructure expansion with the transition to renewable energy sources, while navigating complex regulatory environments and managing water resources effectively.

Nordic Countries to Benefit

We believe the Nordic countries (Sweden, Norway, Finland, Denmark and Iceland) are exceptionally well positioned to capitalize on the data-center and AI boom for several compelling reasons.

Norway and Sweden have extensive hydropower infrastructure, providing stable, renewable baseload power. Denmark is a leader in wind energy, with offshore wind farms supplying growing portions of its grid. Finland has a diverse energy mix including nuclear, hydro and biomass, which allows data centers to meet their sustainability commitments due to the renewable-rich mix.

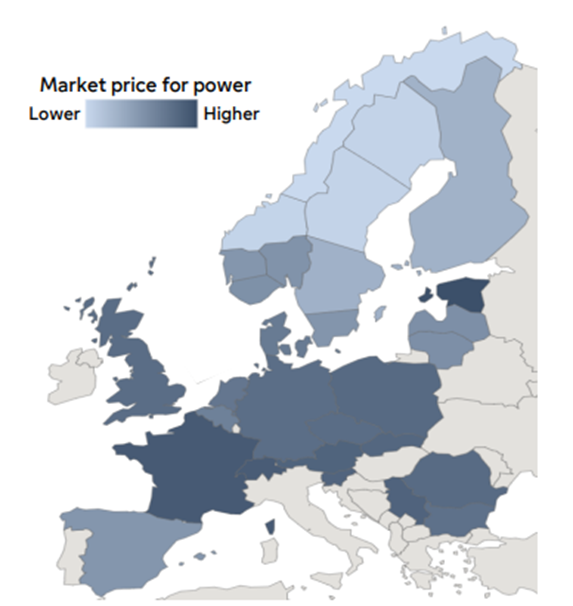

The Nordic Region is a Source for Competitive and Clean Energy

Nordic Power Demand is Driven by Decarbonization and Electrification

Cold ambient temperatures for six to eight months of the year dramatically reduce cooling costs, which typically account for 40% of data-center energy consumption. Several facilities in the region use “free cooling” techniques, drawing cold air or water directly from the environment, representing significant operational cost savings compared to facilities in warmer regions.

Strong regulatory frameworks provide assurance for long-term infrastructure investments, and there is low geopolitical risk compared to many other regions. Additionally, transparent business practices as well as strong workforce education levels and technical expertise, contribute to political and economic stability in the region.

The region boasts excellent fiber-optic infrastructure connecting to major European markets and proximity to submarine cable landing stations for international connectivity. Its strategic position linking Europe to North American markets also enhances its connectivity advantage. Sweden’s “Node Pole” region has attracted major investments from US tech companies.

Norway offers low electricity prices, often 50% lower than the EU average, and 98% renewable generation. Finland provides tax incentives specifically for data centers and direct connections to Russian and Baltic markets. Denmark benefits from strong interconnection with the German grid, providing stability. Iceland has unique geothermal energy resources and 100% renewable electricity.

Seeking Greener Pastures

The global economy is increasingly driven by rapid advancements in technology and infrastructure, with AI and data centers at the forefront. As the demand for energy and technological connectivity grows, strategic investments in infrastructure, particularly renewable energy and grid modernization, become crucial. In our view, Europe, with its government support, competitive advantages and commitment to decarbonization, is well positioned to capitalize on these trends.

In our view, utilities and infrastructure companies that embrace innovation and sustainability should thrive in this evolving landscape. The Nordic countries, with their renewable energy resources, favorable climates and regulatory stability, stand out as leaders in this sector. Investors seeking diversification and growth opportunities should consider the potential of European infrastructure, as it offers promising return potential and can contribute to a more resilient future.

In summary, the intersection of technology and infrastructure presents a unique opportunity for growth and innovation. By investing wisely and strategically, Europe can regain its competitive edge and pave the way for a prosperous future.

[1] Source: European Commission, https://commission.europa.eu/document/download/10017eb1-4722-4333-add2-e0ed18105a34_en

Authors

James A Lydotes

Head of equity income and deputy chief investment officer, equity

Brian Blongastainer

Global Investment Strategist

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR007137. Exp 3/30. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

Comments