Key Points

- US large-cap returns have been driven to all-time highs by a narrow set of growth stocks dubbed the Magnificent Seven.

- The lack of breadth in the S&P 500® rally has led to a highly concentrated index and left some sectors and industries historically cheap relative to the broad market.

- In our view, investors can benefit by diversifying their broad US large-cap exposure by adding value-oriented stocks with solid fundamentals, attractive valuations, and business momentum.

- We believe the energy and financials sectors contain intriguing pockets of value.

The S&P 500 index has hit a series of all-time highs in 2024 but returns have been led by a handful of large growth stocks—the Magnificent Seven—whose performance has been driven by the promise of future growth from artificial intelligence. In our view, they are attractive businesses, but investors get plenty of exposure to them through broad US large-cap mandates.

These new record highs would suggest that the entire US equity market is expensive. However, lack of market breadth has been the key story of the recent equity rally. The performance dispersion has led to a disproportional rise in the valuations of the Magnificent Seven relative to the rest of the market. However, value opportunities exist in the US equity market for those prepared to look. Our value and income strategies seek to provide diversification to the S&P 500 index and those Magnificent Seven stocks.

Valuations

Growth investing flourished over the last decade owing to a combination of low interest rates, low inflation, and central-bank quantitative easing. But in the current environment of higher rates and inflation, US value stocks look quite inexpensive—as cheap as they were during the dot-com bubble in the late 1990s and early 2000s. Not coincidentally, the dot-com bubble was also characterized by extended valuations while index returns were dominated by a narrow set of stocks whose market capitalization grew significantly.

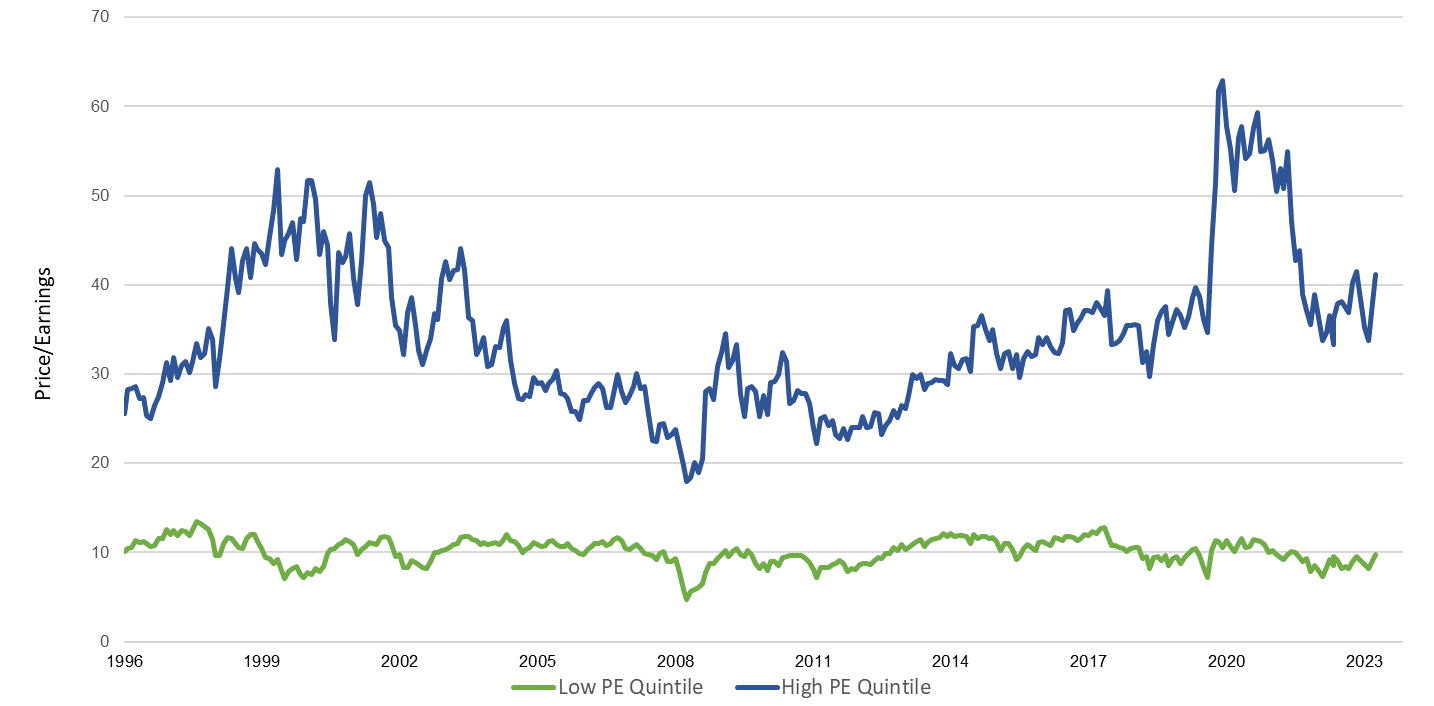

The chart below displays the wide gap between the most expensive and the cheapest quintiles of stocks in the S&P 500 based on price to earnings (P/E) valuation levels. The cheapest quintile appears inexpensive historically relative to the most expensive quintile. But the cheapest quintile also represents value relative to its own history, with a P/E of 9.5 compared with an historic average of approximately 10, also shown in the chart below.

Valuation Spreads Appear Attractive S&P 500 P/E Valuation Levels: September 31, 1996 – December 31, 2023 Low (Cheap) versus High (Expensive) Quintiles

Against this backdrop, we believe there is significant opportunity in quality companies that trade at high free-cash-flow yields and low P/E multiples that look attractive from an intrinsic valuation perspective. Additionally, we think there is ample opportunity to diversify into those low P/E stocks to offer some balance to the expensive names that are populating the S&P 500 index.

Sectors

Energy and financials are two sectors where the team is seeing value opportunities. Energy accounts for just 4.6% of the S&P 500 market capitalization but 11.1% of the S&P 500 index’s income as of December 31, 2023. Similarly, the financials sector comprises 21.6% of the S&P 500’s income but only 13.2% of the index’s market capitalization. By contrast, the Magnificent Seven stocks constitute 28.3% of the S&P 500 index by market capitalization but generate just 16.9% of the income.

In our view, energy companies tend to have good balance sheets and generate a significant amount of free cash flow with minimal net debt with a balanced oil supply and demand, leading to sustainability of attractive oil prices. Energy stocks are also appealing from a dividend perspective. There are multiple opportunities in the energy space that are delivering significant cash back to shareholders in the form of dividends. We discussed this further in in our blog ‘Not Your Parents’ Energy Sector.’

Within financials, we see opportunities in insurance companies and select banks. We believe the stocks are inexpensive, have good risk versus reward, and carry high dividend yields that are both sustainable and have the potential to grow.

Dividend Growth

While current dividend payout ratios in the US are low relative to those historically, we believe these ratios have room to increase. Dividend-paying stocks may be an overlooked option for investors looking to hedge against inflation. This is a key difference between equity and fixed-income yields: equity income does not have fixed coupons. Companies with pricing power—the ability to pass price increases along to consumers—may have a distinct advantage. In addition to pricing power, another competitive advantage is the ability to pay steady dividends. We think the US is poised to show material dividend growth over the next five to ten years relative to the current low payout ratios.

Conclusion

Outside of the Magnificent Seven, prices and valuations for the rest of the S&P 500 have faced pressure amid a surge in inflation and the Federal Reserve’s aggressive rate-hiking cycle. However, we believe there are multiple reasons why investors may want to look for opportunities to diversify beyond mega-cap technology companies by looking for value and income stocks.

Authors

Newton US large cap value & income team

Insights from the Newton US large cap value & income team

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR005908 Exp 03/29. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

Comments