Key Points

- Both President Biden and former President Trump support bringing jobs back to the US.

- Recent legislation has laid the foundation to create more US manufacturing opportunities while reshoring has also been accelerated by geopolitical concerns.

- We believe that public and private investment in infrastructure, onshoring and sustainability may provide a broad opportunity set to create value.

In an era where party lines can seem more polarized than ever, there is one topic where both sides come together—supporting a US manufacturing resurgence. President Biden, like President Trump before him, is pursuing a populist agenda, with a doctrine of bringing jobs back to the US.

Policy under the Biden administration has created favorable conditions for reshoring, the practice of bringing manufacturing and services back to the US from overseas, by way of the Infrastructure Investment and Jobs Act (IIJA), Inflation Reduction Act (IRA) and Creating Helpful Incentives to Produce Semiconductors and Science Act of 2022 (CHIPS). Each piece of legislation provides funding and tax incentives to spur domestic manufacturing in industries where the US has an excess dependency on imports.

Geopolitical disruptions are also driving companies to re-evaluate supply-chain priorities. Covid-19 shutdowns, the war in Ukraine, the Israeli-Hamas conflict and increasing tension over Taiwan have prompted companies to consider reshoring and near-shoring as insurance against further potential disruptions.

Fiscal Stimulus Kicking In

The significant fiscal stimulus that passed Congress in 2021-22 is now starting to kick into gear. The IRA of 2022 established a New Advanced Manufacturing Production Credit to incentivize the domestic production of various components, including applicable critical minerals used in renewable energy generation, storage and related manufacturing. Infrastructure spending from the IIJA is only beginning to be allocated, which should support US aggregate-oriented producers. The IRA also has approximately $3 billion in financing and facilitation tools to support the buildout of transmission lines across the country.

The IIJA provides historic funding levels to improve public works, including roads, bridges, highways and internet access, as well as to mitigate the effects of climate change. The legislation should have a significant positive impact for a range of industrial companies. While construction businesses are perhaps the clearest category that could benefit, so could companies throughout the industrial-supply chain, including steel and material suppliers, and engineering services firms.

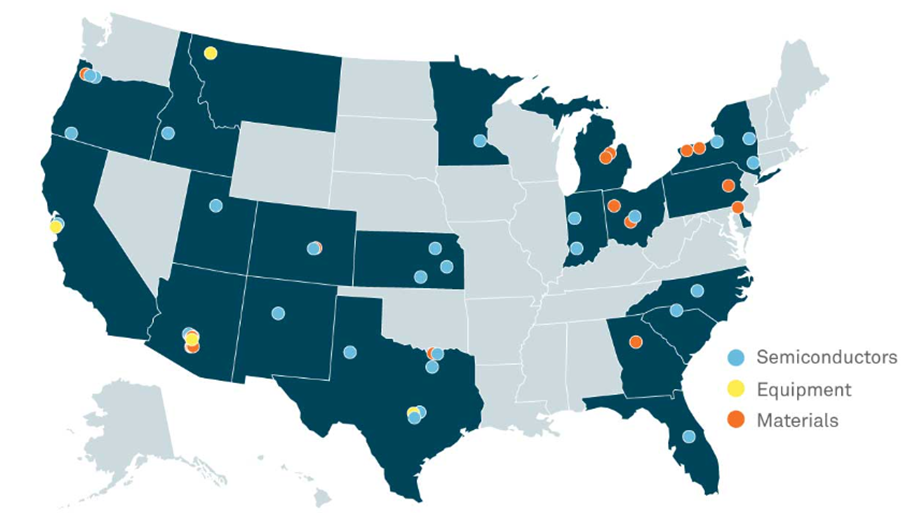

CHIPS aims to encourage investments in domestic semiconductor-manufacturing capacity. It also seeks to jump-start research, development and commercialization of leading-edge technologies, such as quantum computing, artificial intelligence, clean energy and nanotechnology. This investment is mainly driven by geopolitical risk given China’s potential interest in asserting control over Taiwan’s technology industry in an effort to gain technological supremacy over the US, Europe and other countries. We believe there is strong potential for semiconductor capital-equipment companies which manufacture the equipment used to make semiconductors.

Semiconductor Supply-Chain Manufacturing Investments Announced from May 2020 to June 2023

Conclusion

President Biden and former President Trump seemingly do not see eye to eye on many issues—however, there is one area of the economy that we believe is poised to thrive regardless of who wins the US election in 2024. After decades of underinvestment in the US industrial base, supply-chain difficulties during the pandemic and geopolitical tension have highlighted the advantages of greater US self-sufficiency. As a result, hundreds of billions of dollars in federal funding and other incentives are set to pour into infrastructure, onshoring/reshoring, and the “electrification of everything,” through legislation such as the 2022 IRA and the 2021 IIJA. We believe there is ample opportunity in a US manufacturing renaissance—no matter who is elected president in 2024.

Authors

Newton US large cap value & income team

Insights from the Newton US large cap value & income team

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR005981 Exp 04/29. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.