Shifting Sentiment

Financial-market participants began 2025 with optimism. Republicans had won a decisive victory in November’s US election, and the expectation was that President Donald Trump would implement policies similar to those enacted during his first term, with a focus on reducing regulation and extending tax cuts. The read-across was that such a backdrop would be broadly supportive for equities.

However, as the first quarter progressed, this sentiment shifted significantly, notably as a result of the new administration’s volatile trade policies. In addition, US foreign and defense policies underwent a major realignment, prompting European countries to begin boosting defense spending. Germany’s incoming coalition government immediately committed to loosening the country’s rigid fiscal rules, paving the way for a €500bn multi-year investment in infrastructure. Finally, the long-running artificial intelligence narrative was disrupted by reports that the Chinese-backed DeepSeek large language model could perform in line with more established US offerings at a fraction of the cost.

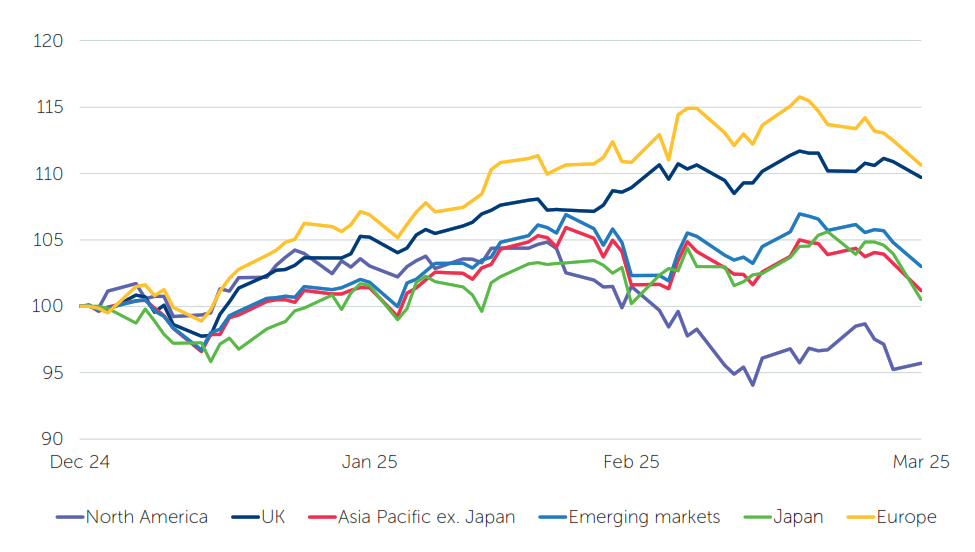

Equity Markets

Total returns (US$), rebased to 100 at 12.31.24

Note: all indices are MSCI series.

Source: FactSet, March 31, 2025.

In this environment, global equities overall declined over the three-month period, but a closer examination reveals a marked divergence between the performance of different regions and asset classes. The ‘magnificent seven’ US tech giants, which have been central to equity-market strength over the last two years, collectively entered bear market territory during the quarter.1 On the other hand, Europe’s pivot in favor of enhanced fiscal stimulus fueled optimism that the region’s economy could gain momentum, and propelled potential beneficiaries higher.2 The China-centric Hong Kong market also delivered strong returns.3

Meanwhile, gold, a traditional safe haven, experienced its best quarterly performance since 1986,4 boosted by concerns that the Trump administration’s tariff plans could widen the global trade war and trigger an economic slowdown. Benchmark 10-year US Treasury bonds ended the quarter with yields (which move inversely to prices) down over 0.35%.5 Conversely, Germany’s decision to lift its self-imposed debt brake for higher defense spending pushed German bund yields up.6 Elsewhere, 10-year Japanese government bond yields surged to their highest level since 2008, driven by expectations of further interest-rate hikes by the Bank of Japan.7

A New Era of Trade Tariffs

It has quickly become clear that President Trump’s second term in the White House will not be a rerun of his first, and that his administration is set to use of trade tariffs more broadly. However, the ultimate purpose of these tariffs is less certain. Is the purpose to generate revenue with the aim of reducing income taxes? Is it a negotiation strategy to persuade former allies, such as Canada and Mexico, to collectively impose tariffs on China as a North American trading bloc? Is the goal to rebalance global trade and incentivize the reindustrialization of the US? Is it all of the above?

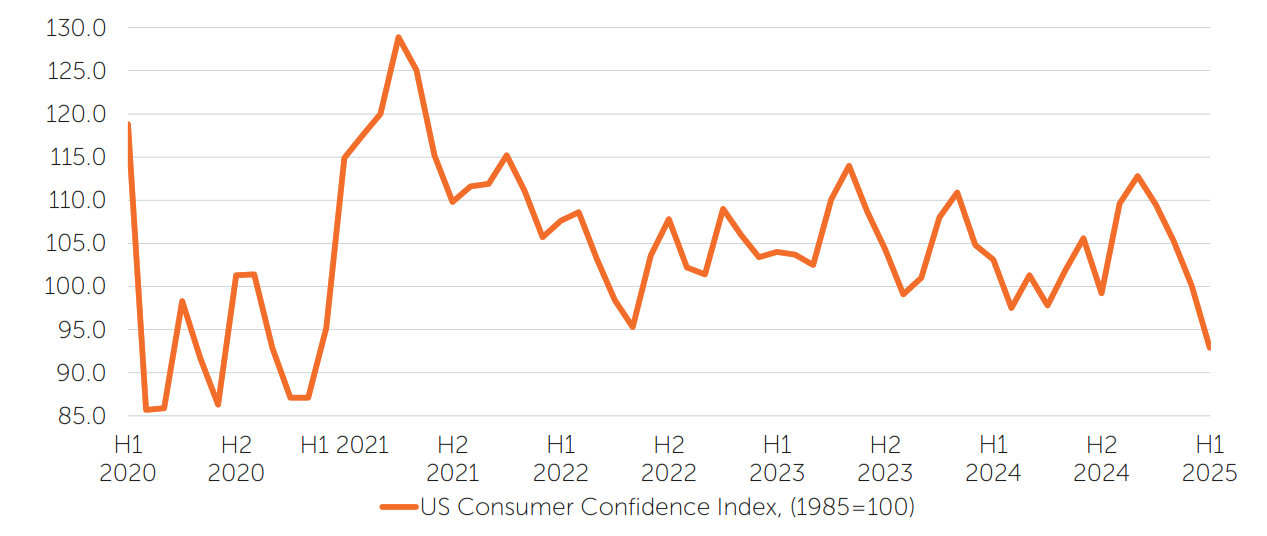

Economic Challenges in the US and Beyond

Regardless of the eventual outcome, the White House’s approach to trade policy is generating significant uncertainty for US companies and households. There are already observable signs of a material weakening in consumption, while consumer sentiment is beginning to turn sour.8

US Consumer Confidence Index

Source: US Conference Board, FactSet, April 2025.

With the growth of household incomes decelerating,9 an increase in prices due to tariffs, even if it occurs only once, is likely to exert substantial pressure on consumption. The downside risks to consumption will undoubtedly increase if businesses reduce hiring and investment.

The risks to the US economy are also influenced by the efforts of the newly established Department of Government Efficiency to pare back government spending. While there may be long-term benefits to reining in the size of the government, in the short term, reducing government expenditures is likely to decrease private-sector incomes and aggregate corporate profits, exerting additional pressure on the labor market and investment. During the first quarter, it has become apparent that the new administration is willing to endure short-term economic challenges in pursuit of longer-term objectives.

The economic impact of tariffs will not be borne solely by the US, especially if other countries reciprocate with similar measures. The White House may be employing tariffs as a means to encourage other countries to lower their own tariffs. While this may ultimately be successful, there is also a possibility that both sides may perceive the other as having initiated the conflict. Consequently, US reciprocal tariffs could represent the first shots fired in an ongoing trade war.

Higher barriers to trade are likely to have a negative impact on global hiring and investment. Although there has been an easing of fiscal policy in Germany and a seemingly more unified Europe, the likelihood of the US experiencing a significant economic slowdown – and potentially a recession – while the rest of the world does not is low. Nonetheless, as it becomes increasingly evident to other nations that they can no longer depend on the US in the same manner as before, countries are having to take matters into their own hands.

Investment Opportunities amid a Divergent Backdrop

In this environment, we observe increasingly divergent monetary and fiscal policies. For several years, we have maintained that peak globalization is in the rearview mirror, with the global order shifting towards increasing divergence. This perspective has gradually proven accurate, and the current US administration’s approach is accelerating this trend. Consequently, investors should encounter a broader range of opportunities across different regions, as the world’s primary economic blocs become progressively less synchronized.

The outlook for equities in the upcoming months, and potentially quarters, may be adversely affected by central banks’ caution. For now, at least, these policymakers are equally concerned about the inflationary pressures posed by tariffs as they are with the potential decline in economic growth. ‘Uncertainty’ is the watchword of major central banks, with the US Federal Reserve (Fed) notably adopting a ‘wait and see’ approach.10 In our view, there is a risk that should the Fed delay interest-rate cuts until economic indicators justify such action, any resultant economic slowdown may be more severe than it might have been with earlier intervention.

From a long-term perspective, investors face two contrasting potential outcomes. On the one hand, an intensifying trade war could cause a prolonged global recession. On the other, assertiveness from the US in trade policy might prompt other nations to reduce their trade barriers, potentially fostering increased globalization.

It is virtually impossible to predict how the current backdrop will evolve, and it is therefore prudent to exercise caution and refrain from assuming more knowledge than we possess. In this context, and considering the potential for significant geopolitical developments, we believe that the attributes of resilient, liquid and diversifying portfolios are likely to come to the fore. Furthermore, we think a discerning approach to security selection will be crucial in identifying those investments that can harness their unique strengths and adapt to changing market conditions. Prized characteristics such as durable business models, robust cash generation and solid balance sheets should help investments to navigate a potentially volatile backdrop.

1 Source: FactSet, March 31, 2025

2 European Stocks Surge Ahead Of S&P 500 In Q1 2025, Forbes, March 31, 2025

3 Chinese investors pour record funds into Hong Kong stocks in first quarter, Reuters, March 28, 2025

4 Source: FactSet, March 31, 2025

5 Source: FactSet, March 31, 2025

6 Markets in Q1: Everything’s been Trumped!, Reuters, March 31, 2025

7 Source: FactSet, March 31, 2025

8 Rising fears of tariffs pummel US consumer confidence to four-year low, Reuters, March 25, 2025

9 Threats to U.S. Household Income Growth, Moody’s Analytics, February 11, 2025

10 Fed in no rush to cut rates; Trump disagrees, Reuters, March 20, 2025

All data is sourced from FactSet unless otherwise stated. All references to dollars are US dollars unless otherwise stated.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC (“NIMNA” or the “Firm”). NIMNA is a registered investment adviser with the US Securities and Exchange Commission (“SEC”) and subsidiary of The Bank of New York Mellon Corporation (“BNY”). The Firm was established in 2021 and is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand “Newton” or “Newton Investment Management”. Newton currently includes NIMNA, Newton Investment Management Ltd. (“NIM”) and Newton Investment Management Japan Limited (“NIMJ”). This document is provided for general information only and should not be construed as investment advice or a recommendation. You should consult with your advisor to determine whether any particular investment strategy is appropriate. Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that portfolio holdings and positioning are subject to change without notice. In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario, including the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations. MAR007229 Exp 04/2026.