Key points

- The Office for Budget Responsibility (OBR) forecasts point to moderately higher borrowing needs than expected, and inflation to remain a little above target until 2028, potentially curtailing the ability of the Bank of England to cut rates.

- While Chancellor Rachel Reeves spoke, there was little reaction, but the OBR forecast and the UK Debt Management Office (DMO) revised supply guidance has caused a small sell-off in gilts.

- Key for the long term will be whether this budget and this administration delivers productive investment, or simply spending.

The long-awaited Budget, the first for the Labour government in over 14 years, was unveiled on Wednesday. The focus of the bond market has been on the widely telegraphed re-writing of the fiscal rules, the impact of investment and spending plans on near-term gilt issuance, and the short and medium-term impact on inflation and economic growth of the various measures announced. The outturn was directionally similar to market expectations; however, the Office for Budget Responsibility (OBR) forecasts point to moderately higher borrowing needs than expected each year, and inflation a little above target until 2028, potentially curtailing the ability of the Bank of England to cut rates. These two factors pushed yields up during the course of the afternoon.

The previous Conservative government had progressively eroded fiscal headroom and public investment had been falling in real terms, indicating a need for change. At the same time, the new Labour government has made clear political choices to focus on lower-income and unionised wage-earners and public-sector workers, possibly at the cost of older and, in some cases, asset-rich citizens.

The fiscal rules and many of the measures announced had been shared in advance, and the bond and currency markets had anticipated much of this, but the gilt market has reacted mildly negatively to the fact that gilt issuance will be at the upper end of what was feared.

Long-dated gilt yields had risen more than short-dated gilt yields since the UK election, partly in anticipation of higher spending and greater gilt issuance in future years. More recently, yields had risen a little faster for medium-dated maturities as some investors thought that the extra gilt supply may be concentrated in that area, to take advantage of lower yields in those maturities.

Sterling had strengthened modestly since the election, but this was more likely owing to expectations of a closer relationship with the European Union, and a period of relative stability after the election, rather than a clear verdict on growth or the interest-rate trajectory.

Immediate market reaction

While Chancellor Rachel Reeves spoke, there was little reaction, but the OBR forecast and the UK Debt Management Office (DMO) revised supply guidance has caused a small sell-off in gilts. Changes to the fiscal rules to the public sector net financial liabilities definition of borrowings created additional headroom, and the Chancellor has used most of this immediately. Expectations had been for tens of billions of pounds in extra borrowing each year compared to prior OBR forecasts. However, the reality is more in the range of £20-30bn per annum, which is larger than the supposed ‘black hole’, despite billions of pounds of tax increases.

Bank of England reaction function

On balance, the Bank of England has maintained a dovish stance. This week’s Budget may temper that, but the Bank of England governor Andrew Bailey has previously expressed less concern about higher public sector pay compared to private sector pay as an inflationary catalyst. In addition, tax increases are more front-loaded, while much of the investment spending will take longer to deploy, potentially keeping a lid on short-term growth.

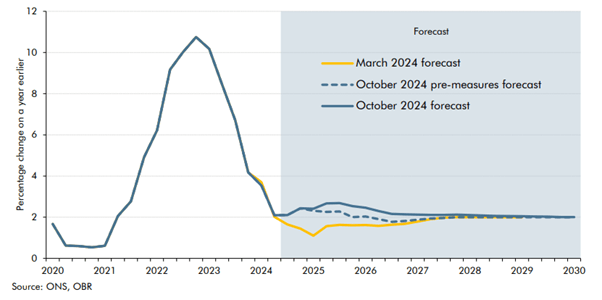

Inflationary pressures

The OBR has confirmed our expectation that the measures announced would tend to be inflationary. Avoiding the main direct personal taxes, but imposing higher costs on businesses (through higher employer national insurance contributions and an above-inflation increase in the living wage), as well as raising indirect taxes, is likely to result in higher prices.

Consumer Prices Index (CPI) inflation

Source: OBR

Productive investment or spending?

Key for the long term will be whether this budget and this administration delivers productive investment, or simply spending. Infrastructure upgrades would be welcome, as would measures to reduce the swollen ranks of those not in work owing to health issues. Increasing the pool of those able to work would reduce some of the upward pressures on employment costs linked to other measures.

Your capital may be at risk. The value of investments and the income from them can fall as well as rise and investors may not get back the original amount invested.

Authors

Howard Cunningham

Portfolio manager, Fixed Income team

This is a financial promotion. These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This is not investment research or a research recommendation for regulatory purposes. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. MAR006774 Exp: 10/2025.

Important information

Issued in the UK by Newton Investment Management Limited, 160 Queen Victoria Street, London, EC4V 4LA. Registered in England No. 01371973. Newton Investment Management is authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. ‘Newton’ and/or ‘Newton Investment Management’ is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021 and NIMJ was established in March 2023.