Key points

- For retirees choosing to draw down their retirement portfolios, there is a complex set of trade-offs, which requires clarity on risk.

- A critical factor for the success of a decumulation portfolio is the sequence of returns the retiree experiences.

- However, conventional risk tools may have limited effectiveness in tackling sequencing risk and could result in under-investing a retiree’s decumulation portfolio.

- Decumulation portfolio design and management therefore demands a more comprehensive range of risk measures.

Saving for retirement in a defined-contribution (DC) pension plan is a well-studied topic that has resulted in two main types of investment solution:

- For individual plans, advisors typically suggest pooled mixed-asset portfolios that are risk-aligned to their clients’ risk appetite and capacity.

- For institutional DC pensions (master trusts and employer plans), lifestyle or target-date funds are used for default strategies. These recognise the changing balance of financial risk and human capital and aim to deliver a savings outcome that is palatable. Designed to suit the average plan member, they cater for savers who are, on the whole, disengaged and disinterested. Default-fund investing therefore dominates most pooled plans.

As individuals get closer to retirement, there is typically an increase in engagement with pensions that can be triggered by wake-up packs. These prompt near-retirees to select between pathways depending on their likely retirement choice (annuity purchase, encashment, deferral or drawdown). These pathways represent material differences that demand differently aligned investment strategies leading into retirement. For both institutional and individual DC plans, more specific and personalised choices become critical to bridge members and clients from the saving phase to the decumulation phase.

For the very wealthy, potentially with large DC savings, retirement lifestyle is unlikely to be wholly or even materially reliant upon the performance of their DC pension assets. To the extent that their investment choices are relevant, they are also more likely to seek or receive professional advice.

At the other end of the wealth spectrum, state benefits will underpin the majority of retirement income, and the minimal DC plan assets that do exist are less likely to make a material long-term contribution to retirement lifestyle. Understandably, therefore, full encashment, perhaps to repay debt, can be a sensible option, albeit taking care to avoid adverse tax and benefits impacts.

For those with aspirations for a retirement lifestyle beyond what is supported by guaranteed income sources (such as state benefits or a prior defined-benefit plan), there is increasing reliance on the quality of income that can be derived from DC investments. Those valuing predictability, stability and reliability over flexibility and inheritance appear destined for annuity purchase. However, most do not follow this path. Even with more appealing annuity rates now available, the irreversibility of this step remains unappealing to most retirees.

The majority appear to be attracted to flexibility, or perhaps just to deferring a tough decision. They continue to invest and, at some point, start to draw on their assets to maintain their lifestyle. They become heavily reliant on investment performance to deliver overall return so that they do not run out of assets, and a good sequence of returns so that their portfolio is not unexpectedly depleted.

These retirees face a complex set of trade-offs that good investment design can seek to help resolve:

- Maximising lifestyle and income reduces the potential for legacy and increases the chance of exhaustion of resources and penury in old age.

- Pensioners concerned about old-age poverty can live an unnecessarily frugal lifestyle.

- The potentially material impact of future bouts of inflation on the cost of living indicates a need for real-asset exposure. However, these assets tend to have less stable returns which could lead to sequencing risk that can deplete resources.

- The uncertainty of an individual’s lifespan can only be directly hedged by purchasing an annuity; however, this curtails flexibility and control. Those determined to remain ‘self-insured’ need, therefore, to take a precautionary approach: drawing a lower level of income so there is a higher chance of remaining financially solvent for as long as there is any material chance of remaining alive. This could mean a planning horizon of age 92+ if they seek a high (90%+) probability of remaining solvent in old age.[1]

Measurement and control of risk

Resolving the complex trade-offs faced by clients requires clarity on risk. When investment and risk are mentioned together, there is a tendency to think of evaluating risk in an established way. The first instinct is to focus on the uncertainty of annualised returns. The most common way to quantify this is volatility; however, a variety of other measures like Value at Risk (VaR), the Sharpe ratio and the Sortino ratio are closely mathematically related. This toolkit has served investors well in the context of wealth accretion and growth for decades.

For those building pension drawdown portfolios, it is understandably tempting to reach for these familiar tools in the same way as has been done during the savings phase. However, this could lead to an unappealing negative feedback loop:

- In an attempt to protect retirees from the potential ravages of sequencing risk, a diverse and low-volatility portfolio is created.

- This limits real-asset exposure and is likely to have commensurately low return potential.

- As a result, the maximum safe withdrawal rate supported by the portfolio is unappealingly low.

- In addition, the payments, such as they are, have only scant protection from bouts of inflation that may be experienced during the course of 20 to 30 years of retirement.

- Retirees’ desire to maintain a given lifestyle may mean withdrawing at a higher rate than is durable, which raises the prospect of the portfolio being exhausted long before death.

A desire for low levels of risk has created a situation in which there is a high risk of old-age penury. Low-volatility assets are not necessarily a low-risk strategy.

What is the alternative?

We think the starting point is to reconsider the risk toolkit. The accumulation challenge rightly focuses on asset uncertainty (volatility); however, creating durable retirement income is rather different. We believe risk tools aligned with real-income uncertainty are better suited to serving the drawdown client’s needs.

A critical factor for the success of a decumulation portfolio (i.e. delivering the required real income for as long as needed) is found to be the sequence of returns the retiree experiences.

What is sequencing risk and how dangerous is it?

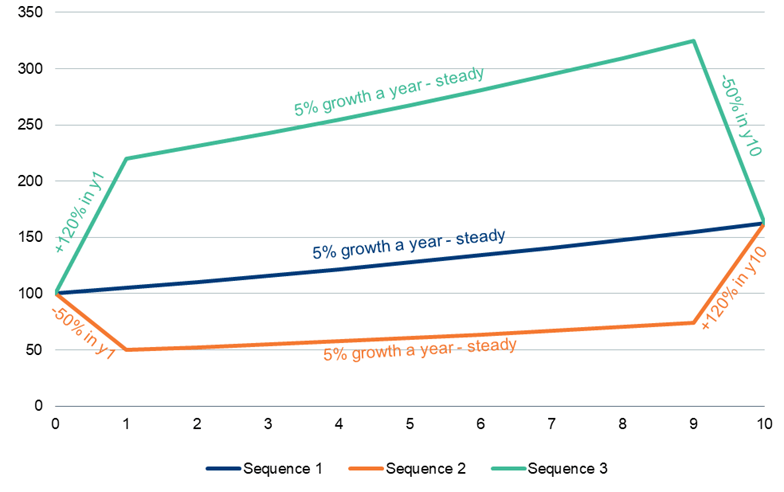

In exhibit 1 we illustrate three sequences of returns delivering the same accumulation outcome. All three deliver a 5% annualised return over a 10-year period: 100 grows to 163.

Green has a good year at the start and a bad one at the end whereas orange experiences the opposite. Irrespective of this, the outcome is the same.

Exhibit 1: Lump sum

Source: Newton, 2024.

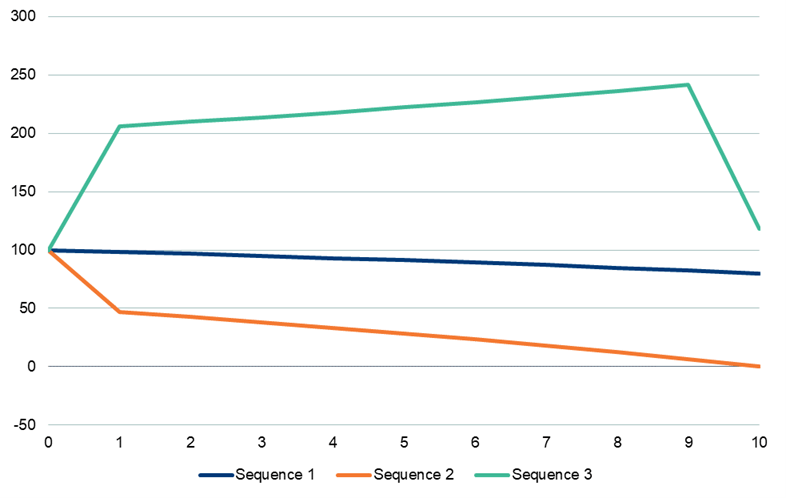

If, however, this portfolio is also supporting a drawdown of 6.3% each year, the same sequences of returns lead to starkly different outcomes, illustrated in exhibit 2. The orange portfolio is depleted entirely over the period whereas green, with the inverse sequence of returns, remains relatively healthy and outperforms blue, with steady returns.

Exhibit 2: 6.3% decumulation

Source: Newton, 2024.

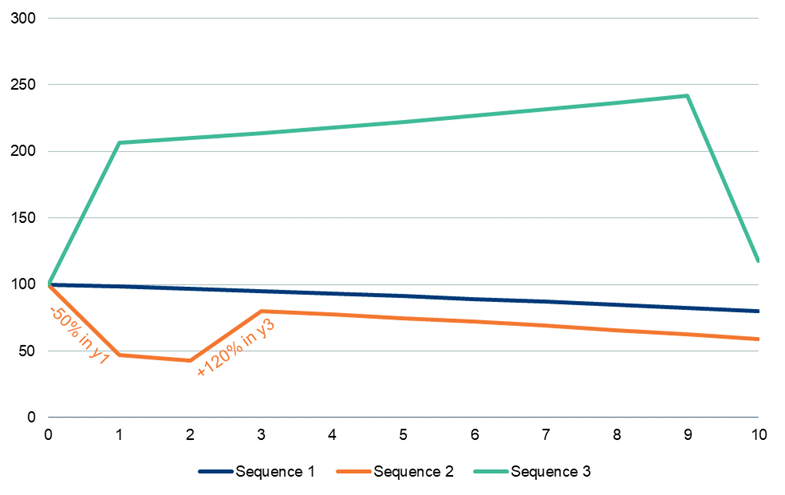

The impact of sequencing risk on decumulation portfolios depends not only on when rises and falls occur, but also on how long an adverse drawdown event lasts. Exhibit 3 shows the improved outcome for orange of an earlier recovery, in year 3 instead of year 10. The annualised return overall is unchanged but, in this situation, the orange portfolio is no longer exhausted entirely.

Exhibit 3: 6.3% decumulation with an earlier recovery

Source: Newton, 2024.

Sequencing risk is particularly dangerous because conventional tools for measuring and managing risk are prone to offering false signals.

The volatility of orange and green pathways in every case above is identical (40%). The blue paths have zero volatility. This ubiquitous measure of portfolio risk has failed to differentiate between the markedly different outcomes experienced by drawdown investors with different sequences of returns; it does not differentiate between the orange pathways in exhibits 2 and 3 that differ only in the length of delay before recovery.

Other conventional risk measures are also exposed to the same flaw. For example, maximum drawdown in the green and orange pathways is also the same at -50%.

Even worse, the conventional evaluation of risk and reward together, the Sharpe ratio, also evaluates the same outcome for green and orange pathways. This is because they both deliver a 5% return and 40% volatility. There is no recognition of the money-weighted value/cost of excess/negative returns.

The conventional approach to avoiding the asset exhaustion seen in the orange portfolio in exhibit 2 is to reduce investment risk by lowering volatility. This appears logical as the blue portfolio, with zero volatility, offers a better outcome.

Sequencing risk is particularly dangerous because conventional tools for measuring and managing risk are prone to offering false signals.

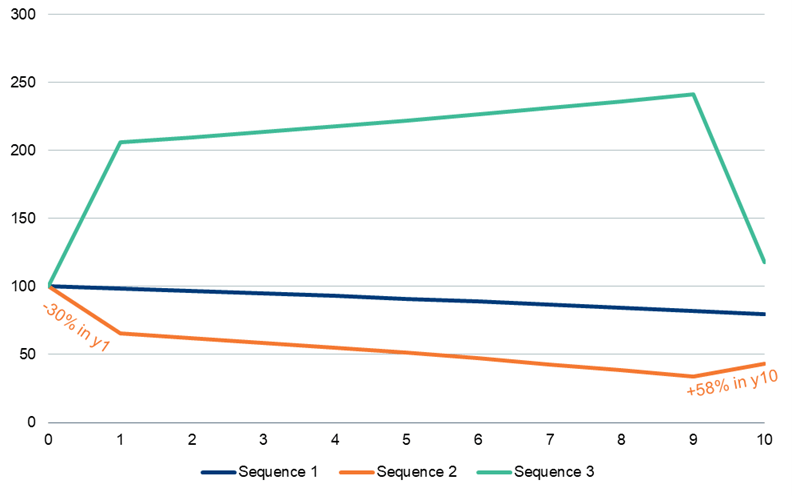

To what extent does lower volatility affect the outcome?

In exhibit 4, the overall annualised returns in each of the pathways remains 5%. However, in this case, the orange portfolio experiences half the previous level of volatility. The fall in year 1 is only 30% and a commensurate recovery in year 10 of 58% results in the same 5% per annum, as in previous cases. The orange sequence volatility is now 20% compared with 40% before.

Exhibit 4 illustrates that even at a much lower volatility level, with an adverse sequence of returns, we still see a worse outcome than those with higher volatility with better sequences or faster recoveries seen previously.

Exhibit 4: 6.3% decumulation with lower volatility

Source: Newton, 2024.

Halving the volatility has been less effective than improving the sequence of returns.

The implications for portfolio construction, manager selection and financial advice are material. In a decumulation setting we can no longer entirely rely on conventional risk evaluation tools:

- Volatile assets may not need to be avoided if they tend to recover quickly from drawdowns.

- Managers adept at building portfolios that recover quickly, for a given level of volatility, can potentially offer clients a better outcome.

- Investment suitability for a client’s risk appetite/capacity in decumulation needs to be evaluated in terms beyond simply a volatility target range.

Decumulation portfolios may be invested more conservatively than necessary

Exhibit 4 illustrated that halving volatility gave some improvement to the orange portfolio versus exhibit 2 (but not as much as the better sequence in exhibit 3). However, the charts assumed equivalent annualised returns in all portfolios. Lowering portfolio volatility is ordinarily linked to lower real-asset exposure, which could lead to a reduction in return potential.

If we assume the risk premium in these models was originally, say, 3%, with cash rates at 2%, the consistent outcome for the orange portfolio in exhibit 4would be 25% smaller still.

We see a vicious spiral where the desire for low sequencing risk, delivered by lowering volatility, drives down portfolio risk-taking and generates lower overall returns with less potential to keep pace with real-world inflation.

Using conventional risk tools that have limited effectiveness in tackling sequencing risk may result in under-investing a retiree’s decumulation portfolio. In other words, a risk-averse retiree who is currently advised to have a low-volatility portfolio could potentially access the higher return potential of a higher-volatility portfolio that is specifically designed to recover quickly from market stresses.

Durable decumulation

Decumulation portfolio design and management is distinct and demands a more comprehensive range of risk measures. We need ways to properly evaluate and control sequencing risk. With sequencing risk in check, we can seek to unlock additional return potential for retirees. This could result not just in higher long-term withdrawal rates, but also in the potential for retirement income to keep pace with long-term inflation, thereby creating ‘durable decumulation’.

[1] Source: Newton calculations based on data provided by the Faculty of Actuaries.

Authors

Christopher Nichols

Global Investment Strategist, Mixed Assets Team

This is a financial promotion. These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This material is for professional investors only. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that holdings and positioning are subject to change without notice. MAR006420 Exp: 07/2029.

Important information

Issued by Newton Investment Management Ltd. ‘Newton’ and/or ‘Newton Investment Management’ is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021 and NIMJ was established in March 2023. In the United Kingdom, NIM is authorised and regulated by the Financial Conduct Authority (‘FCA’), 12 Endeavour Square, London, E20 1JN, in the conduct of investment business. Registered in England no. 01371973. Registered office: 160 Queen Victoria Street, London, EC4V 4LA, UK. NIM and NIMNA are both registered as investment advisors with the Securities & Exchange Commission (‘SEC’) to offer investment advisory services in the United States. NIM’s investment business in the United States is described in Form ADV, Part 1 and 2, which can be obtained from the SEC.gov website or obtained upon request. NIMJ is authorised and regulated by the Japan Financial Services Agency (JFSA). All firms are indirect subsidiaries of The Bank of New York Mellon Corporation (‘BNY’).

Comments