Economic and market background

In late December, NASA’s Parker Solar Probe made history by surviving the closest solar encounter ever attempted by a spacecraft. Travelling at 430,000 miles per hour, the fastest-ever human-made object endured temperatures of up to 982°C (1,800°F) and intense radiation as it entered the sun’s outer atmosphere in a quest to gain a better understanding of our star.1

During the final quarter of 2024, financial markets also broke some records, with the Nasdaq and S&P 500 US equity indices reaching all-time closing highs on 6 December,2 marking the peak of a rally that followed Donald Trump’s victory in the US presidential election. Nonetheless, market participants felt the heat at times too, notably in mid-December when attention turned to an increasingly hawkish Federal Reserve (Fed). Meanwhile, bond markets saw a sharp sell-off over the quarter, with yields rising as concerns grew over inflationary pressures and as the US economy demonstrated continued resilience.

After a bumpy October which saw a tense run-up to the US election and continued instability in the Middle East, US stocks soared in November as investors embraced the decisive election outcome and anticipated the incoming administration’s policy agenda of business-friendly tax cuts and deregulation. In the weeks following Trump’s win, some of the top performers included economically sensitive businesses and names that would benefit from a relaxation of the regulatory environment, such as banks and small-cap companies.

Outside the US, European and emerging markets struggled amid fears that proposed US tariffs could ignite a trade war and dampen growth elsewhere. Japanese equities fared relatively well over the quarter though, as they continued to rebound from their dramatic summer sell-off.

The Fed lowered interest rates at its December meeting, as widely expected, but its Chair Jerome Powell repeatedly emphasised caution, indicating that future reductions in borrowing costs would depend on further progress in reducing stubbornly high inflation.3 Although he expressed confidence that price pressures would continue to ease, he noted that policymakers were starting to consider how Donald Trump’s proposals relating to tariffs, tax cuts and tougher immigration policy might affect the outlook.

The Fed’s policymakers now project they will make only two 0.25% rate reductions during 2025 – a combined half a percentage point less than they had forecast when meeting in September. US stocks plunged sharply in the immediate aftermath of the Fed’s December announcement, and the traditional ‘Santa rally’ failed to materialise during the final trading days of the year.

Europe’s continued economic weakness was exacerbated by political turmoil over the quarter as the governments of two of its largest economies – Germany and France – collapsed, while Italy, which had experienced a relatively strong rebound following the Covid pandemic, showed new signs of stagnation.4 Meanwhile, escalating tensions between Russia and the West, following the use by Ukraine of US and UK-supplied missiles to hit targets inside Russia, dominated headlines.

While equities may have ended the year with a whimper, stock markets experienced a strong year overall, with North America once again the standout performer. 2024 was also notable for the strength of the US dollar, amid robust US growth, while gold logged its best year since 2010 and hit an all-time high on 30 October.5

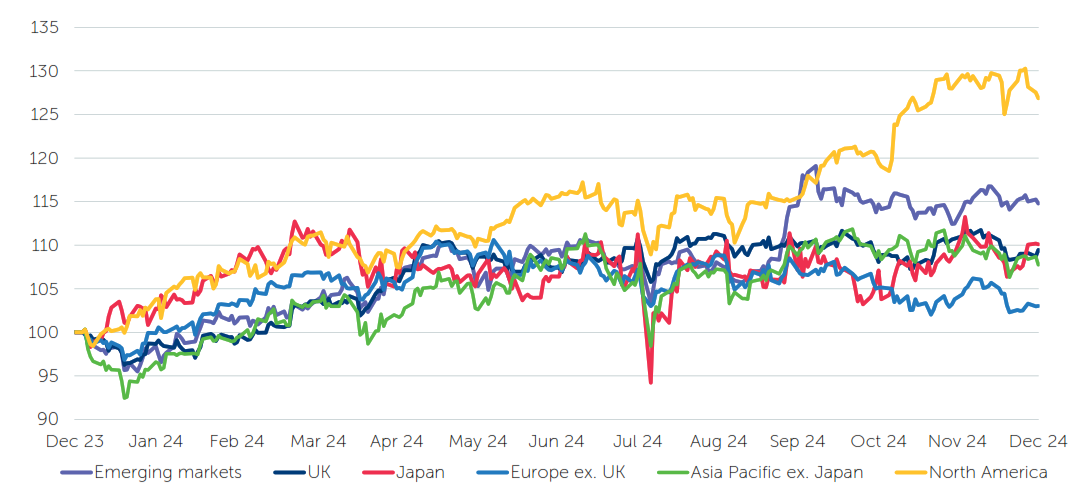

Equity markets

Total returns (£), rebased to 100 at 31.12.23

Note: all indices are FTSE series.

Source: FactSet, January 2025.

Total returns (%) to 31 December 2024

| Asset class | Index | 3 months | 12 months |

| UK equities | FTSE All-Share | -0.4 | +9.5 |

| North American equities | FTSE World North America (£) | +9.9 | +26.9 |

| European ex UK equities | FTSE World Europe ex UK (£) | -3.9 | +3.0 |

| Japanese equities | FTSE Japan (£) | +2.8 | +10.1 |

| Asia-Pacific ex Japan equities | FTSE World Asia Pacific ex Japan (£) | -1.0 | +7.8 |

| Emerging-market equities | FTSE All-World Emerging (£) | +0.2 | +14.8 |

| UK gilts | FTSE Actuaries UK Conventional Gilts All Stocks | -3.1 | -3.3 |

| Corporate bonds | ICE BofA Sterling Non-Gilt | -0.4 | +1.8 |

| Overseas government bonds | JP Morgan Global Government Bond (ex UK) (£) | +1.0 | -1.8 |

| Gold (US$) | Gold ($/ozt SIX) | -0.4 | +27.1 |

| Gold (£) | Gold (£/ozt SIX) | +6.5 | +29.3 |

Source: FactSet, 1 January 2025. All equity market returns are sterling total returns.

Regional overview

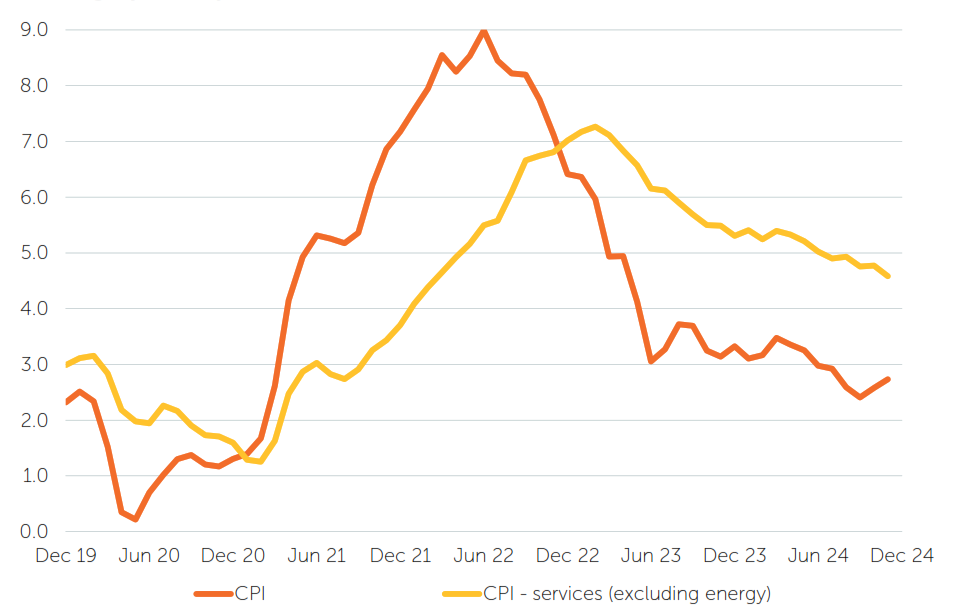

On 29 December it was announced that former US President Jimmy Carter, who later won the Nobel Peace Prize for humanitarian work, had died at the age of 100.6 While US consumer price inflation, which rose by 2.7% year on year in November,7 is far below the double-digit levels experienced during much of Carter’s 1977-1981 presidency, Fed Chair Jerome Powell has expressed disappointment at how inflation has moved “sideways” in recent months, hindering progress towards the central bank’s 2.0% target.

November’s consumer price inflation data did indicate that the increase in services inflation was slowing, with rents rising at the slowest pace in over three years. Furthermore, there were tentative signs that the labour market could be cooling, with unemployment rising to 4.2% in November from 4.1% in the previous two months. However, proposed trade tariffs from the incoming Trump administration have the potential to counter these disinflationary trends.

According to the US Bureau of Economic Analysis, the economy has remained robust and supported by consumer spending, with gross domestic product (GDP) increasing by 2.8% on an annualised basis in the third quarter, after expanding by 3.0% from April to June.8

US consumer price inflation (CPI)

% change, year on year

Source: FactSet, January 2025.

Enrico Letta, former Italian prime minister and author of a report commissioned by the European Union (EU) on the future of the single market, has warned that the political crises in Germany and France should not be allowed to slow the implementation of much-needed economic reforms. A second report by former European Central Bank (ECB) President Mario Draghi presents detailed plans on how to improve European competitiveness. Although there is considerable uncertainty as to how the EU will implement these recommendations, it is widely acknowledged that substantial investment is necessary. This will be crucial as European productivity continues to lag the US, and Europe must also address potential increased US tariffs and growing trade tensions with China.

With inflation fears having largely subsided in December, the ECB cut interest rates for the fourth time in 2024 as the economy remained weak. Germany, the eurozone’s largest economy, is now expected to grow by only 0.2% in 2025.9

The UK’s economy also appeared lethargic towards the end of the year, unexpectedly shrinking for two consecutive months for the first time since the 2020 Covid pandemic, according to the Office for National Statistics.10 The declines were a setback for Chancellor of the Exchequer Rachel Reeves, whose first Budget on 30 October avoided increases to the main direct personal taxes but imposed higher costs on businesses.

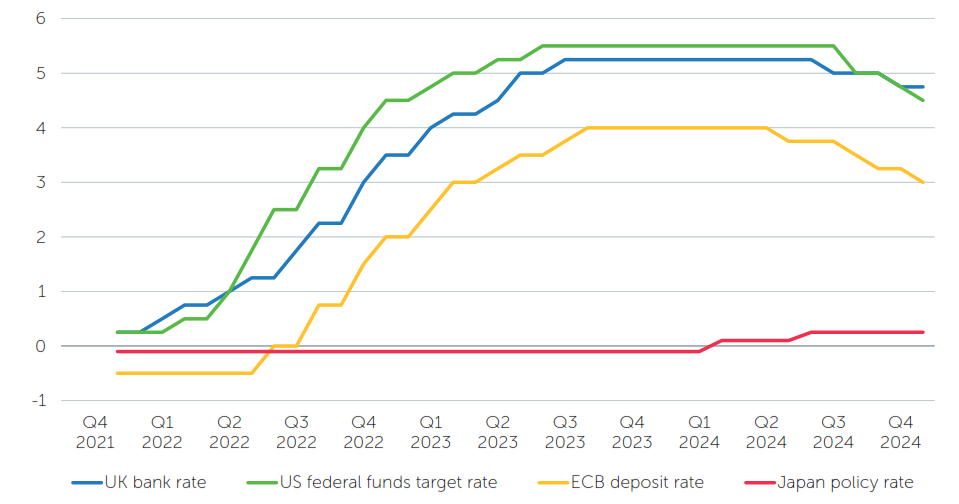

As part of that autumn Budget, the UK government reformed its fiscal rules in pursuit of faster economic growth through increased public investment and spending, but business groups have warned that employers may face challenges with higher social security contributions. Forecasts from the Office for Budget Responsibility (OBR) point to moderately higher borrowing requirements than previously expected each year, and inflation a little above target until 2028, potentially curtailing the ability of the Bank of England (BoE) to cut interest rates. The BoE kept its rate unchanged at 4.75% in December, although three of the nine Monetary Policy Committee members voted for a cut.11 It was less willing to reduce rates in 2024 than its US and European counterparts.

While the Bank of Japan’s (BoJ) governor Kazuo Ueda has resolved to continue raising interest rates from their current very low levels, the central bank opted to keep its short-term policy rate on hold at 0.25% at its December meeting.12 The timings of future rate hikes are likely to be linked to gaining further certainty over US President-elect Donald Trump’s economic policies, including the threat of higher tariffs, as well forthcoming wage negotiations. BoJ policymakers hope that workers’ regular pay, which has been increasing annually by 2.5-3%, will continue rising and support consumption. There are indications that companies plan to keep raising pay owing to growing labour shortages.

Japan’s GDP grew at an annual rate of 1.2% in Q3 2024, surpassing economists’ expectations, despite weak consumption.13 The yen has stayed close to historical lows in recent months owing to Japanese interest rates trailing behind those of other major economies, with currency weakness contributing to increased import prices.

On 29 January China will enter the lunar year of the ‘wood snake’, which typically signifies transformation and growth. The country expects its economy to have expanded by around 5% in 2024, in line with its official target,14 but there has been some venom from a prolonged property market downturn, increasing local government debt and subdued consumer confidence.

Although an official target is unlikely to be announced until an annual parliamentary meeting in March, President Xi Jinping believes China will see a similar growth trajectory in 2025.15 This is despite the threat of high tariffs from the incoming US administration, which could damage exports, a key driver of the economy. In this context, stimulus measures are likely to focus on boosting consumption and expanding domestic demand. China has pledged to increase the budget deficit by issuing additional debt, and ease monetary policy.16 However, Beijing may delay implementing further direct fiscal stimulus measures until after the new US administration’s initial actions.

Investment implications

At the start of 2024, there was broad concern that a recession or a reacceleration of inflation would upset the global economy and equity markets. Instead, we have seen a continuation of the disinflationary growth that began in late 2022. Risk assets have spent the last 12 months climbing the proverbial wall of worry, and 2024 turned into a banner year for those invested in broad equities, with the MSCI AC World Index up 18% in US-dollar terms.17

Significant attention has been given to the narrow scope of the equity-market rally, specifically the notion that its progress was reliant on a limited number of individual securities. While this observation may have held true in the early part of 2023, last year witnessed a broadening of market participation. Although a relatively small number of stocks contributed disproportionately to the total market return, numerous equities have provided substantial returns throughout the year.

It is not only equity markets that have been on the front foot. Corporate credit spreads (the yield premium over government bonds) relentlessly narrowed over the course of the year, suggesting investors have grown increasingly sanguine about the risk of recession.

Contrary to the widespread pessimism at the beginning of 2024, investor optimism has increased alongside the rise in equity markets. Sentiment and positioning are now at the upper end of historical ranges by many measures. While this does not preclude further advances in risk assets, it presents a more challenging starting point compared to early 2024. The potential for disappointment is higher when expectations are generally positive.

Trump’s return

The general optimism regarding the US economy and equities is partially informed by the outcome of the US election. It is widely believed that Donald Trump’s first term as president from 2017-2021 had notable economic and market impacts, particularly owing to the Tax Cuts and Jobs Act. The expectation is that Trump’s second term will also be favourable to businesses, especially when compared to the previous administration. There is anticipation that regulations may be reduced in key economic sectors, with policies likely to encourage growth. Additionally, there have been significant nominations to positions such as Treasury Secretary and chair of the Council of Economic Advisers.

Nevertheless, various other factors contributed to the economic outcomes during Trump’s first term. The Fed had shifted to a more accommodative stance in early 2016, while the ECB and BoJ increased large-scale asset purchases. Consequently, global credit conditions were easing; China managed to complete the bailout of its financial system and implement a substantial stimulus programme, and bank lending was accelerating in the US and Europe as commercial banks had completed the process of repairing their balance sheets. By early 2017, the global economy was experiencing its first period of synchronised growth since the 2008 financial crisis. While the Tax Cuts and Jobs Act served to increase US corporate earnings, the foundations for the economic upswing in 2017 were established prior to Trump’s administration.

Today, the global economy has limited momentum. China continues to grapple with the burden of a deflating housing market, and Beijing has not yet implemented policy measures sufficient to reflate its domestic economy. Europe has significant structural issues, worsened by losing access to cheap Russian energy and with reduced demand for German exports from China. In the US, while the economy is stronger, it is in a mature phase of its cycle. This is not to suggest that a recession is imminent, but a reacceleration of the global economy as seen in 2017 appears unlikely in 2025.

The Fed’s divergent path

The divergent fortunes of the world’s economies are evident through the lens of central banking. Collectively, monetary authorities have been easing policy since 2023. However, they are on the cusp of charting different paths. While many central banks remain inclined to administer further reductions in their respective policy rates, the Fed has recently indicated that there may be fewer interest-rate cuts in 2025 than had previously been expected.

Fed Chair Jerome Powell outlined in his 18 December press conference that the Federal Open Market Committee was unhappy with the progress that has been made on inflation, which has remained above target in recent months despite a series of rate cuts. By the end of the press conference, the market was once again pricing in ‘higher-for-longer’ interest rates.

In the wake of the Fed meeting, the US dollar broke out from the range it had been in since early 2023 when the Fed’s dovish pivot brought the dollar bull market to an end. The renewed strength of the dollar contributes to tighter global credit conditions, which is a concerning development for the already weakening global economy.

Interest rates (%)

Source: FactSet, January 2025.

Bond vigilantes

In late 2018, Trump famously warned Powell to “feel the market” after Powell noted that the Federal Reserve was “a long way from neutral” amid declining US equities and widening credit spreads. On that occasion, Trump ultimately proved correct as Powell ended up performing a dovish pivot in the final days of 2018. However, this time the Fed chair may indeed be pre-emptively feeling the market.

Since the central bank began cutting interest rates, the US yield curve has steepened as longer-dated yields have moved sharply higher. Bond yields started to rise before the election result, moving up from the lows of September when markets were concerned about growth, but they have continued to climb since the election, and the relentless supply of government bonds, both in the US and globally, is likely to remain a significant macroeconomic trend in the coming years. The bond market is finding it challenging to determine an interest rate that adequately compensates investors amid sustained fiscal expansion and persistent inflation above target levels. In this context, monetary and fiscal policy are likely to remain at odds in the foreseeable future.

US 10-year Treasury yield (%)

Source: FactSet, January 2025.

Not all plain sailing

Equity-market volatility remained relatively low during 2024, a characteristic often observed during periods of disinflationary growth and accommodative monetary policy. However, with the Fed’s shift towards a more hawkish stance, it is likely that markets will no longer receive the same level of support. This change in US policy is expected to tighten global credit conditions at a time when the global economy is far from robust. As evidenced by the events of 2018, external economic and market weaknesses can eventually affect the US. Despite investors’ generally optimistic outlook for 2025, it is unlikely that sailing will prove to be as smooth as it was in 2024.

Conclusion

Investors enter 2025 against a backdrop that appears relatively constructive, at least in the short term. The US economy has remained resilient, and the incoming US administration has a policy agenda focused on growth and deregulation. This environment is likely to present significant investment opportunities, particularly in areas that benefit from technological advancements and policy support.

Nevertheless, several challenges lie ahead. Notably, the Fed’s more cautious stance on interest-rate cuts indicates a tighter monetary-policy environment, which could affect global credit conditions. Meanwhile, the large and growing fiscal impulse, as well as the prospect of trade tariffs, could allow inflation to reassert itself.

Outside the US, the global economy has limited momentum, as China and Europe grapple with their respective structural issues. Meanwhile, geopolitical tensions pose significant risks, as the conflicts in Ukraine and the Middle East, and possible changes to US/China trade relations, have the potential to cause disruption globally.

In this context, we consider it crucial to maintain flexibility and conduct thorough evaluations of the attributes of individual securities in order to unlock investment opportunities.

We must adjust to changing times and still hold to unchanging principles.

Jimmy Carter, US president 1977-1981

1 NASA’s Parker Solar Probe Makes History With Closest Pass to Sun, NASA Science, 27 December 2024

2 S&P 500, Nasdaq hit record closing highs; Lululemon gains, data supports rate cut view, Reuters, 7 December 2024

3 Fed lowers rates but sees fewer cuts next year due to stubbornly high inflation, Reuters, 19 December 2024

4 Italy’s growth bubble bursts to reveal fragile outlook, Reuters, 17 December 2024

5 Source: FactSet, 31 December 2024

6 Former US president Jimmy Carter dies aged 100, Financial Times, 29 December 2024

7 US consumer prices post largest rise in seven months; rents finally slowing, Reuters, 11 December 2024

8 US third-quarter economic growth unrevised at 2.8%, Reuters, 27 November 2024

9 Germany faces lethargic growth, potential hit from Trump, Bundesbank says, Reuters, 13 December 2024

10 UK economy suffers first back-to-back declines since 2020, Reuters, 13 December 2024

11 Bank of England keeps rates steady, policy split widens, Reuters, 19 December 2024

12 Bank of Japan keeps rates unchanged with few clues on next move, Reuters, 19 December 2024

13 Japan revises Q3 GDP higher, keeps alive BOJ rate-hike expectations, Reuters, 9 December 2024

14 China’s GDP growth expected around 5% this year, senior official says, Reuters, 14 December 2024

15 Xi says China’s economy on course to expand by 5% despite Trump concerns, The Guardian, 31 December 2024

16 China pledges more debt, rate cuts to counter Trump’s tariff threats, Reuters, 12 December 2024

17 Source: FactSet, 31 December 2024

All data is sourced from FactSet unless otherwise stated. All references to dollars are US dollars unless otherwise stated.

Important information

These opinions should not be construed as investment or other advice and are subject to change. This document is for information purposes only. This is not investment research or a research recommendation for regulatory purposes. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Issued in the UK by Newton Investment Management Limited, The Bank of New York Mellon Centre, 160 Queen Victoria Street, London, EC4V 4LA. Registered in England No. 01371973. Newton Investment Management Limited is authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. This material may be distributed by BNY Mellon Investment Management EMEA (BNYM IM EMEA) in the UK to professional investors. BNYM IM EMEA, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. ‘Newton’ and/or ‘Newton Investment Management’ is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021 and NIMJ was established in March 2023. MAR006978 Exp 01/2026.