Key points

- As well as being an area of concern for charities, inflation forecasting is key to enable them to project grant giving, withdrawal rates and spending needs.

- While some structural trends remain disinflationary, particularly technological disruption and the integration of artificial intelligence, other trends such as deglobalisation have reversed.

- Provided that the Bank of England sticks to its inflation-targeting regime, it is likely to hold rates higher for longer to bring inflation down and combat the forces of ‘sticky’ inflation.

The 2024 Newton Charity Investment Survey revealed that, despite concern about inflation having declined, inflation remains a unifying issue across the sector. Its implications are significant for charities, as it affects their level of uncertainty about the future, and their ability to maximise the benefit of grants. While some of the concern is related to short-term spikes and the astronomic figures seen in 2022, our discussions with clients have highlighted that charities recognise the potential for inflation to reach a higher average level than it has in the past.

As well as being an area of concern for charities, inflation forecasting is key to enable them to project grant giving, withdrawal rates and spending needs. In response, we outline our views for the inflation and interest-rate outlook over the next five years to 2030. This long-term perspective is important – we are deliberately not forecasting short-term inflation in the current year which will be driven by short-term growth and monetary pressures. Our focus is to collate market forecasts and our view of the structural forces that will affect broad inflationary pressures and the interest-rate-setting policy response in order to assess where inflation in the UK may settle on average.

The policy-setting environment

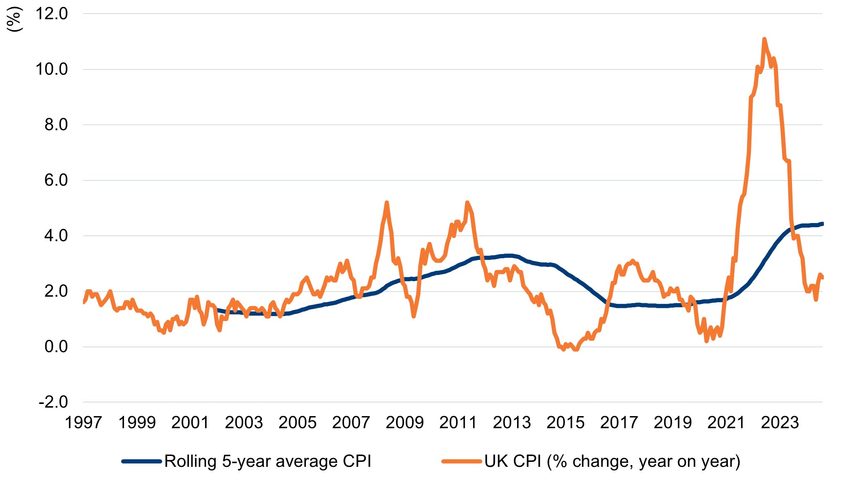

Interest rates and inflation are inherently linked, particularly in the UK where, unlike the US, the mandate of the central bank, the Bank of England (BoE), is focused solely on the delivery of an inflation target. In the UK, this is set by the government at 2% as measured by consumer price inflation (CPI), and any outcome that is 1% above or below this amount must be explained to the chancellor of the exchequer. In order to deliver the objective, the BoE relies on setting interest rates, albeit in recent years it has taken direct action in the gilt and corporate bond markets through quantitative easing (buying predetermined amounts of bonds in order to stimulate the economy and increase liquidity) and tightening (shrinking its balance sheet). The chart below shows annual UK CPI back to 1997, when the BoE was given independence from the government. This highlights the volatility in year-on-year changes in UK inflation as measured by CPI, as well as the considerable length of time when inflation either overshot or undershot this target. We have overlaid a five-year moving average rate.

UK consumer price inflation (% change, year on year)

Bank of England inflation forecasts

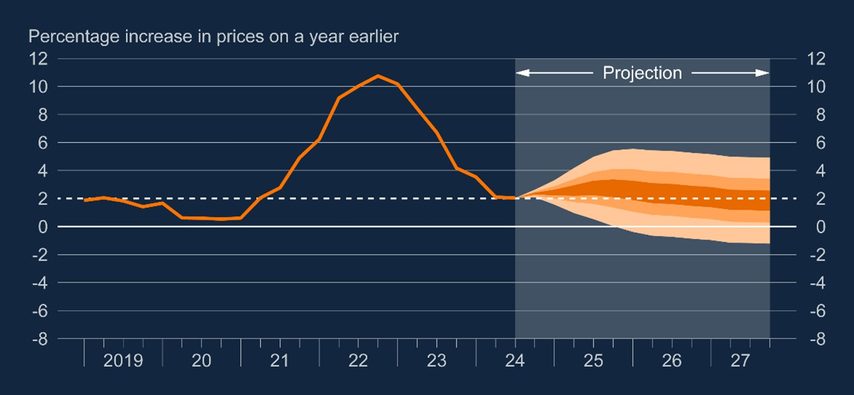

At its monetary-policy setting meetings, the BoE releases its forecasts for a range of economic variables, including inflation, for the next three years based on its interest-rate setting. The primary output for our purposes is the forecast inflation rate and the fan chart below, which conveys the uncertainty around the future path of inflation.

Bank of England CPI inflation projection

Given that the BoE sets interest rates according to a model which predicts what will happen to inflation under interest-rate scenarios, it is, in effect, marking its own homework, and inflation typically comes back to its target over the forecast horizon. The fan chart was subject to criticism from Ben Bernanke, a renowned economist, in his review of the BoE’s forecasting and communication.1

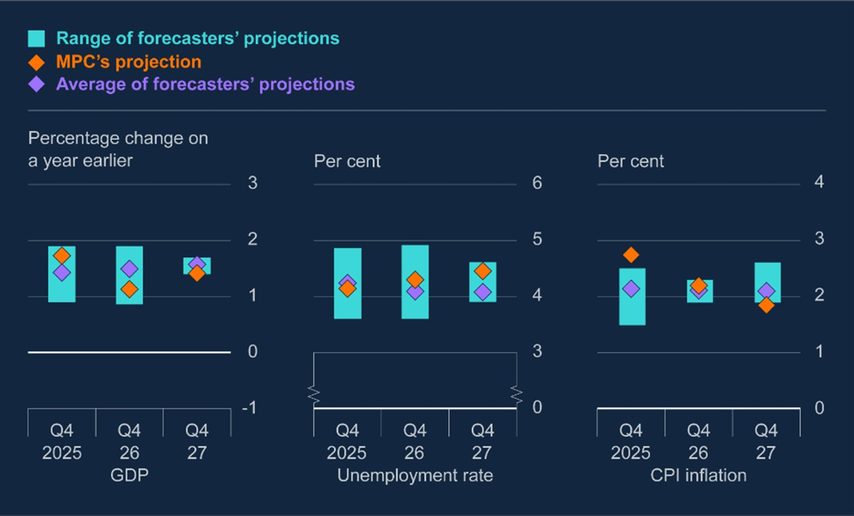

In its report, the Monetary Policy Committee (MPC) also includes the average of market forecasters’ predictions, provided by external researcher Consensus Economics. These are shown for the next three years in the chart below (the latest report is November 2024).

Bank of England summary of external forecasters

The table below shows the actual inflation data that the markers represent:

| Market forecasters | MPC’s projection | |

| 2025 | 2.1% | 2.7% |

| 2026 | 2.1% | 2.2% |

| 2027 | 2.1% | 1.8% |

For long-run inflation assumptions, most forecasters tend towards the BoE’s target, and setting a five-year average number different to that must be based on a view that inflation will consistently overshoot or undershoot the target. As at 28 January 2025, the Bloomberg consensus for CPI is 2.5% for 2025 and 2.2% for 2026.

Bond market expectations

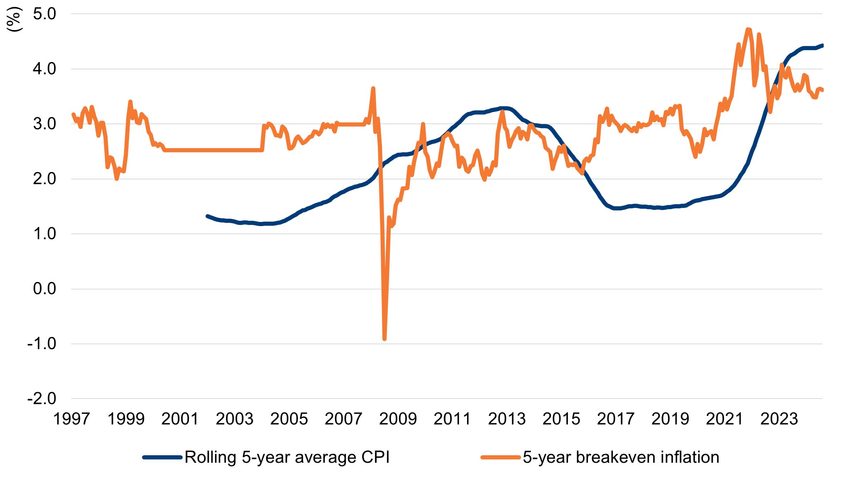

The bond market can be a useful source of forward inflation expectations, by considering what is priced into nominal gilt yields relative to inflation-linked gilts, as shown in the chart below and represented by the grey line, with data going back to 2000. This is calculated as the difference between the real yield (the yield accounting for inflation) received from buying an index-linked gilt, and the nominal yield (the yield before accounting for inflation) from buying a five-year conventional gilt.

Five-year inflation expectations derived from the gilt market2

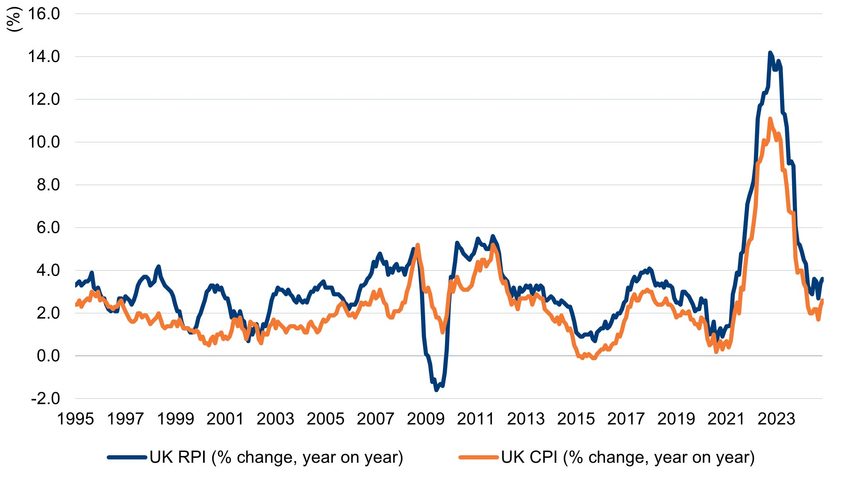

The ‘breakeven’ inflation rate is a measure of the fixed rate that market participants are willing to pay today in order to receive the actual inflation outcome over the subsequent five years. At the end of 2024 this was 3.6%, but while pricing in an active market is a useful starting point, there are reasons to treat this number with caution, as the breakeven level is typically higher than the outturn of inflation. First, buyers are willing to pay a premium for the certainty of receiving actual realised inflation and hedging their risk. This is particularly the case in the UK, where pension funds and insurers are dominant buyers of these assets to protect against liabilities. Secondly, index-linked gilt coupons and principal are currently linked to retail price inflation (RPI) rather than CPI, and for reasons related to different calculation methods and composition of the inflation baskets for the two indices, RPI tends to be higher than CPI. The situation is further complicated by the fact that RPI will be reformulated in 2030 (just beyond this five-year horizon) to be closer to CPI. At the end of 2024, RPI was exactly 1% higher than CPI, while the long-run average was 0.85% higher, as shown in the chart below.

Comparison of UK CPI and RPI

While the five-year RPI breakeven rate at the end of 2024 was 3.6%, that would indicate breakeven market expectations for CPI at around 2.8%. Adjusting for market structure considerations would reduce that expectation further.

Structural considerations

The quantitative easing years which followed the global financial crisis led to rapid asset-price inflation, but not goods-price inflation, which consistently undershot its target. In the early 2000s, the emergence of China as a manufacturing and export centre kept inflationary pressures at bay, boosting corporate profit margins and consumers’ real incomes. Since the Covid-19 pandemic, there has been a regime shift and there are reasons to believe that inflation will now be structurally higher than during the prior two decades.

Some trends remain disinflationary, particularly technological disruption and the integration of artificial intelligence. The adoption rate of this technology in areas previously reserved for humans could have a dramatic impact on labour supply and wage inflation.3 However, other long-term trends have reversed.

Deglobalisation has been replaced with protectionism and reshoring, going against the traditional mantra of comparative advantage in favour of domestic employment. Asia’s role as the global manufacturing centre is changing, and while it remains dominant, local growth and inflation has reduced the cost advantage enjoyed by Western companies. In recent years, there has been a growing focus on investment in decarbonisation initiatives, electrification and reindustrialisation. In the long term, as costs of energy production from renewable sources fall, there is potential for technological disruption. In the short term, however, the impact could be inflationary, with lower investment in fossil fuels while the world remains reliant on them, and a shortage of key minerals such as copper for electrification.4 The peace dividend and low levels of geopolitical risk enjoyed for a long time has changed dramatically in the last few years, and with defence spending on the up and commodity prices more volatile, the inflationary aspects of geopolitical uncertainty are likely to be seen in the data.

We expect inflation data to be more volatile and to settle at a rate above the Bank of England’s target over the five-year forecast period

As a result, we expect inflation data to be more volatile and to settle at a rate above the BoE’s target over the five-year forecast period. Where the average rate settles will depend partly on the reaction function of central banks and their willingness to sacrifice short-term employment and growth for lower levels of inflation. The BoE’s credibility and belief in the mantra of inflation targeting will be on the line.

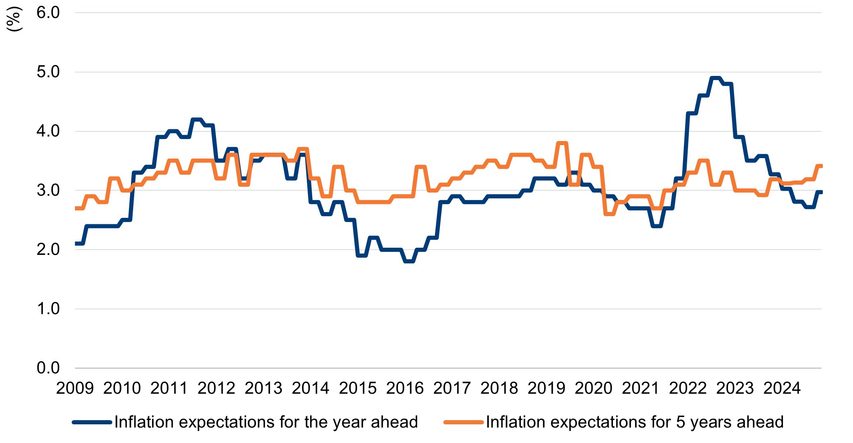

In the short term, measures announced in October’s Budget are likely to push up inflation. According to the British Retail Consortium, 67% of leading retailers stated that they would raise prices as a result of the increase in employer National Insurance contributions and other costs.5 Household inflation expectations have also nudged up, which may feed through to higher wage demands.

Bank of England short and long-term inflation expectations

Interest-rate implications

Interest rates are the BoE’s primary tool to control the price of money and, so the theory goes, the level of inflation through economic activity. We expect policy setting to face very different challenges over the next few years compared to the last 20 years, with the government debt-to-GDP ratio at 100%, stubborn twin deficits (fiscal and trade), a structurally slower economy relative to history, and substantial expected gilt supply. The net result is that investors are demanding higher yields on UK bonds and cash than might otherwise be the case, such that forward interest-rate expectations are currently elevated.

To assess where interest rates are likely to settle is to consider the neutral interest rate – the level at which monetary policy is neither stimulating nor restricting economic growth. This is a hotly debated topic, but we would estimate that the neutral rate in the UK is approximately 3% on a nominal basis. The evolution of demographic trends, productivity growth and the savings and investment balance has brought the neutral interest-rate level down over time, in a similar manner to the reduction in the structural growth rate of the economy.

Current interest rates and gilt yields are therefore in restrictive territory and would be expected to slow activity, particularly in the context of a highly indebted economy such as the UK. Reducing nominal and real interest rates back towards neutral will require a restoration of fiscal credibility, and presents the BoE with the challenge of keeping interest rates high for long enough to calm inflation, but not so long as to drive the economy from low growth to negative growth.

Our estimate

The average levels of inflation and interest rates over the next five years are closely linked subjects. It is likely that cash rates will remain above inflation, creating a positive real return in line with the pre-global-financial-crisis years and without the financial repression of the 2008-2023 period. Provided that the BoE sticks to its inflation-targeting regime, it is likely to hold rates higher for longer to bring inflation down and combat the forces of ‘sticky’ inflation. The path to lower inflation, and whether a recession can be avoided, will rely on the BoE’s policymaking skills. Given the global and local structural factors noted above, we would place a higher probability of inflation reaching an above-target average level than an at-target or below-target level, particularly in the shorter term.

In terms of our forecast point estimate, we believe a 2.5% inflation rate to be reasonable within a 2-3% range for the five-year average. There is a high probability of inflation printing outside of this range within any 12-month period. We would expect the accompanying average BoE base rate to be between 3.5% and 4%, implying real yields of 1-1.5%. Clearly, a recession would change these forecasts, as would a sustained risk premium in the bond market. Forward market pricing of short-term rates is currently in the low to mid-4% range, but this reflects current angst around fiscal policy and could easily drop with a credible fiscal plan or an economic slowdown.

Glossary

Visit our knowledge centre for a glossary of common investment terms and to learn more about key investment concepts.

1. Forecasting for monetary policy making and communication at the Bank of England: a review, Bank of England, 12 April 2024 (https://www.bankofengland.co.uk/independent-evaluation-office/forecasting-for-monetary-policy-making-and-communication-at-the-bank-of-england-a-review/forecasting-for-monetary-policy-making-and-communication-at-the-bank-of-england-a-review)

2. Note that the severe negative rate relates to the global financial crisis of 2008 when market pricing ceased to work effectively.

3. See, for example, Klarna’s announcement that it cut its spending on external marketing suppliers by 25%; even creative industries may see the impacts of generative artificial intelligence: Klarna touts ‘brutally efficient’ AI-enhanced marketing, WARC, 20 May 2024 (https://www.warc.com/content/feed/klarna-touts-brutally-efficient-ai-enhanced-marketing/en-GB/9541)

4. For more on this subject we recommend a very readable speech by the European Central Bank: A new age of energy inflation: climateflation, fossilflation and greenflation, 17 March 2022 (https://www.ecb.europa.eu/press/key/date/2022/html/ecb.sp220317_2~dbb3582f0a.en.html)

5. National Insurance increase will force retailers to raise prices, British Retail Consortium, 15 January 2025 (https://brc.org.uk/news-and-events/news/corporate-affairs/2025/ungated/national-insurance-increase-will-force-retailers-to-raise-prices/)

Authors

Michael Spinks

Portfolio manager, Mixed Assets and Charities team

Howard Cunningham

Portfolio manager, Fixed Income team

These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This is not investment research or a research recommendation for regulatory purposes. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. MAR007057 Exp 01/2026.

Important information

Issued in the UK by Newton Investment Management Limited, 160 Queen Victoria Street, London, EC4V 4LA. Registered in England No. 01371973. Newton Investment Management is authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. ‘Newton’ and/or ‘Newton Investment Management’ is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021 and NIMJ was established in March 2023.