Key points

- The 2024 Newton Charity Investment Survey revealed that charities are experiencing increased demand for their services, which is putting significant pressure on them to balance the needs of future and present beneficiaries.

- Charity investors will need to carefully consider the investment outlook to understand how returns could be affected.

- The policies of the last decade have contributed to a dampening of the economic cycle; however, we are now questioning whether we are returning to a world of heightened cyclicality and increased market volatility.

- Nevertheless, we think that the overall picture for investment income looks positive, with dividend growth expected to continue.

The 2024 Newton Charity Investment Survey revealed that, for the third year in a row, the majority of charities surveyed reported increased demand for their services. Most of these charities stated that this is the combined effect of increased demand from both existing and new beneficiaries. This appears to be corroborated by recent news reports of charities pausing or closing rolling grants programmes owing to unprecedented surges in demand. This situation places significant pressure on finance teams at charities to balance the needs of future beneficiaries against those of present beneficiaries, meaning that charity investors will need to carefully consider the investment outlook to understand how returns could be affected.

2025 investment outlook

Looking ahead, the investment environment is expected to change significantly from the decade preceding the Covid pandemic. We are moving from a period characterised by monetary policy, free trade in a globalised world, zero interest rates, and disinflation, to one dominated by fiscal policy, protectionism, deglobalisation, and potentially higher structural inflation.

The policies of the last decade have contributed to a dampening of the economic cycle. However, with these regime shifts, we are now questioning whether we are returning to a world of heightened cyclicality and increased market volatility.

While prices have finally cooled after a period of high inflation, and the economy has been relatively resilient thus far despite higher interest rates aimed at combatting this inflation, concerns about growth are now prominent.

We are starting to observe some early signs of weakening in the labour market. The economy is still adding jobs, but new job additions have been on the decline, which has reignited fears of a recession. Based on US data, workers are staying put for longer in their jobs, so the amount of moving around is decreasing.

While those in the top income brackets have seen a rise in real wages since the pandemic, the bottom quartile has not and has been facing the ‘big squeeze’ in the face of higher levels of inflation in recent years. This has been noted in a number of earnings calls, particularly from those companies that cater to the lower-income market.

In terms of interest rates, expectations for cuts have lowered. In the summer, seven US rate cuts were being priced in by the end of 2025. The market is currently pricing in four US rate cuts over the next five quarters (as of November 2024), which would leave the policy rate at around 3.8% by the end of 2025, but there is still a big debate around the path of these cuts. The trend appears broadly similar in the UK.

Some market participants believe that growth has been resilient even with higher rates, so any further rate cuts should not be too aggressive in order to ensure that the inflation genie is back in the bottle. On the other side of the debate, people are calling for more aggressive rate cuts in order to pre-empt a recession now that we see evidence of the labour market slowing.

But the ultimate question of both sides is: can the US Federal Reserve stick the soft landing? Can it maintain both low inflation and solid economic growth?

Political change

With Donald Trump as US president-elect, the market’s focus has shifted from political uncertainty to policy uncertainty. With the presidency and both chambers of Congress under Republican control, this political ‘trifecta’ will give Trump considerable authority to enact big changes in areas such as immigration, deregulation, taxes and fiscal spending.

In the UK, the Labour Party’s Budget in October delivered an increase of around £40bn in taxes.[1] Businesses are set to do the heavy lifting on this, with higher National Insurance (NI) contributions expected to bring in the bulk of that total.[2]

How employers absorb this additional NI burden remains a big question. It may end up being a drag on economic growth if businesses, especially employers of lower-paid workers, look to cap wage growth and limit hiring and investment.

The UK government also announced current (day-to-day) spending is projected to rise by £47bn (1.4% of GDP) by 2029/30.[3] The discrepancy between expected tax revenues and spending has meant higher borrowing, all at a point when borrowing costs are high.

The UK faces similar issues around fiscal deficits and government debt levels as the US. However, we are seeing divergent policies emerge between the UK and US economies, with the Trump administration laying plans to reduce public spending and maintain lower taxes, and the UK effectively doing the opposite.

If the UK Budget is not able to raise productivity and growth, these divergent policies could potentially lead to very different longer-term outcomes in growth and inflation for the UK and the US.

Portfolio withdrawal rates

Faced with increased demand and an uncertain investment outlook, many charities have been reviewing their spending plans. Part of this decision is knowing what a durable long-term annual withdrawal rate would be; that is, the amount that can be taken out from income or capital, without compromising the value of investments after inflation.

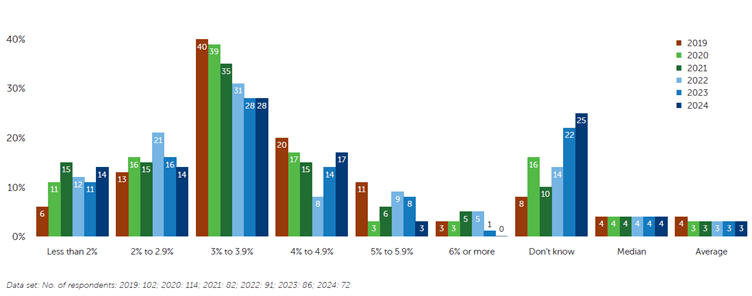

In our survey, we asked charities what level of withdrawal they considered to be maintainable. The figure has come down over the last five years, but the most popular answer is between 3% and 3.9%, closely followed by “don’t know”.

Figure 1: What do you consider to be a sustainable/balanced withdrawal rate (comprising income and/or capital) from your portfolio over the long term to ensure that your portfolio does not reduce in value in real terms (i.e. after inflation is factored in)?

Source: The 2024 Newton Charity Investment Survey

We published a paper on withdrawal rates for charities earlier this year, using forward-looking returns. To calculate a durable long-term withdrawal rate, we made a number of assumptions. We used the dividend yield plus the expected dividend growth rate for global equities, the gross redemption yield for bonds, net initial yield for property, and cash plus 3% for alternatives – all adjusted for inflation at 2.5%. We assumed that the real long-term return on cash would be zero as we expected interest rates to fall.

We then combined these returns using the average charity asset split. According to our research, 3.1% is the likely long-term return rate, aligning with the most popular range selected by charities in our survey, with income comprising 2.5% of this.

Income outlook

Many charities rely heavily on the income produced by their investment portfolio.

Global dividend payouts are expected to grow by 4.2% over 2024, or 6.4% on an underlying basis (that is, excluding special dividends), driven by first-time payers such as Meta, Alphabet and Alibaba.[4] It is noteworthy that these major media-technology companies have reached a maturity level at which they use dividends to return surplus cash to shareholders. The overall trend is one of broad-based growth, with banks an important driver of higher payouts, particularly in Europe.

In the UK’s more concentrated market, the three biggest sectors for dividends are mining, banks and oil. Headline dividend growth for 2024 is expected to be just 2%, because of continuing cuts in distributions from miners, combined with the strengthening of sterling over the summer (two-fifths of UK dividends are declared in US dollars). However, the prospective yield on the UK market is 3.7%, well above the yield available in most overseas markets.[5]

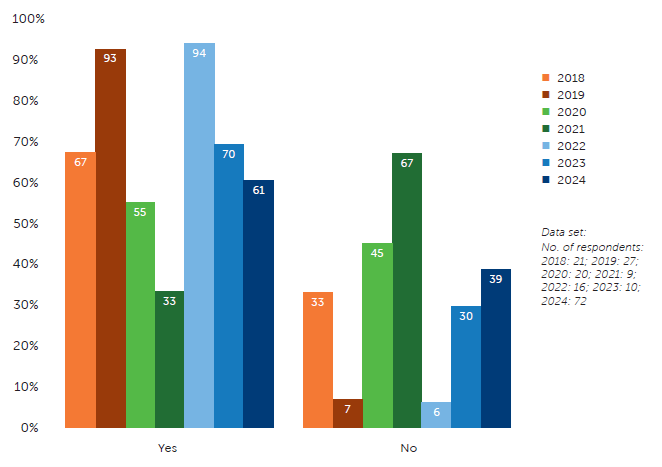

Nevertheless, the proportion of charities reporting that the income produced by their investment portfolios is able to meet the obligations and commitments of their charity has fallen for the second year running, to 61%.

Figure 2: Do you feel that the income produced by your investment portfolio is sufficient to meet the obligations and commitments of your charity?

Source: The 2024 Newton Charity Investment Survey

We previously saw particularly low levels in 2020 and 2021, which was understandable – investment income fell drastically during the lockdowns, as companies cut dividends to conserve cash, or rebased dividends to more durable levels. This particularly affected the UK, which had, to a degree, been overdistributing. In fact, UK dividends are still below the levels of 2019, though they are not far short. Global dividends recovered far more quickly and are now well ahead of 2019 levels, and investors are able to get decent yields on cash and bonds, which they could not in 2020.

We think that the overall picture for investment income looks positive, with dividend growth expected to continue. The recovery in investment income in 2022 has continued since, but at the same time the proportion of charities feeling that it was sufficient has fallen.

Therefore, we think that the reason for income being inadequate more recently must be more of a reflection of the fact that demands on charities have increased, rather than because of falling income over the last two years. If the UK economy picks up, and wage growth continues at a higher rate than inflation, this will hopefully bring some relief for individuals depending on charities such as food banks for their basic needs.

[1] Guardian. Budget 2024: Reeves reveals £40bn in tax rises as she promises to rebuild public services. 30 October 2024.

[2] FT. Businesses and wealthy bear brunt of £40bn tax increases in UK Budget. 30 October 2024.

[3] Capital Economics. Despite large rise in taxes, Budget still boosts economy. 30 October 2024

[4] Janus Henderson Global Dividend Index, November 2024.

[5] Computershare, UK Dividend Monitor – Q3 2024.

Authors

Janice Kim

Associate Portfolio manager, Mixed Assets team

Hilary Meades

Head of Charities Investment

These opinions should not be construed as investment or other advice and are subject to change. This material is for information purposes only. This is not investment research or a research recommendation for regulatory purposes. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. MAR006942 Exp: 12/25.

Important information

Issued in the UK by Newton Investment Management Limited, 160 Queen Victoria Street, London, EC4V 4LA. Registered in England No. 01371973. Newton Investment Management is authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. ‘Newton’ and/or ‘Newton Investment Management’ is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021 and NIMJ was established in March 2023.