Economic and market background

In August, new analysis revealed that the six-tonne Altar Stone, a massive slab of sandstone at the centre of the Stonehenge megalithic monument in Wiltshire, was probably transported over a distance of more than 400 miles to reach the site some 4,500 years ago. As the stone’s geochemical footprint was found to be a perfect match for bedrock found in northeastern Scotland, researchers struggled to comprehend the extraordinary journey, potentially over both land and sea, that the prehistoric site’s creators must have taken to move the hefty cargo.1

Although most major equity indices moved higher over the third quarter of 2024 in local-currency terms, and the consensus for an economic soft landing remained intact at the end of the period, market participants also faced a somewhat rocky journey over the period.

The quarter began with a volatile July that featured political uncertainty in the US and a technology sector sell-off as investors rotated into smaller companies that are viewed as potentially bigger beneficiaries of lower rates. Risk assets then experienced a sharp pullback in early August. A weaker-than-expected US payrolls report induced a growth scare, while the US unemployment rate moved higher than consensus estimates, triggering predictions of a recession. In addition, the strengthening of the Japanese yen and an interest-rate hike by the Bank of Japan at the end of July prompted fears of an unwinding of ‘carry’ strategies in which traders had taken advantage of Japan’s low interest rates to borrow in yen and buy risky assets. This led Japan’s Topix index to suffer its biggest daily drop since ‘Black Monday’ in 1987.2

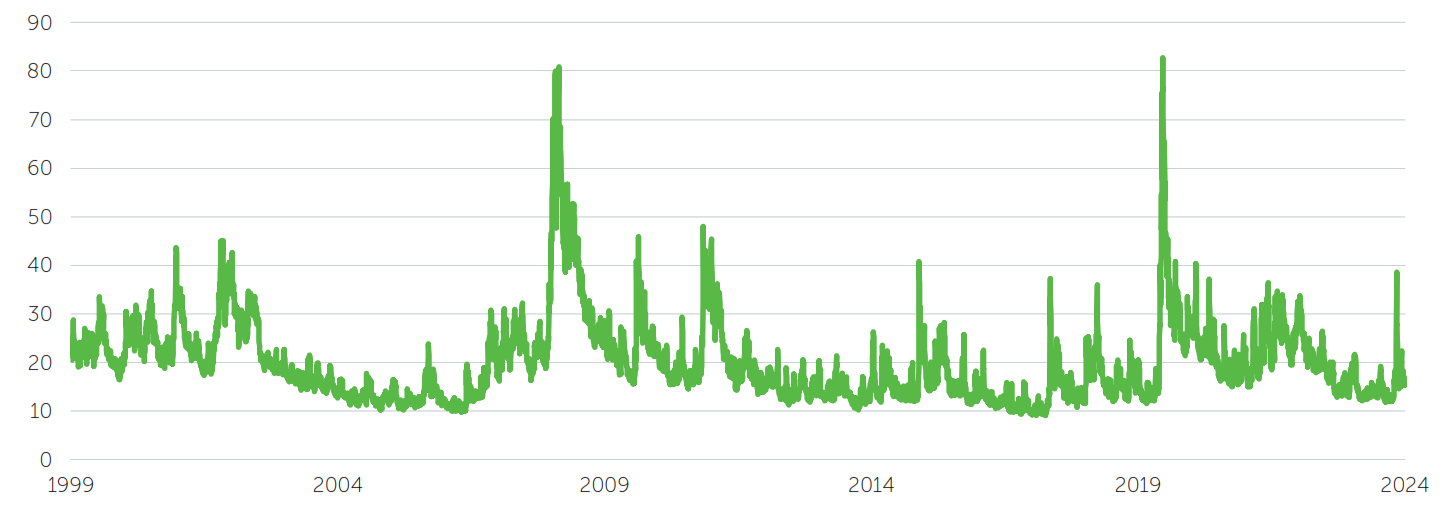

Amid this turbulence, which also saw the S&P 500 index of US equities decline by more than 6% during the first three trading days of August, the CBOE Volatility Index (VIX) experienced its biggest intra-day jump on record.3 While brutal in its intensity, the risk-off phase proved short-lived, with most major equity indices (apart from Japan) back in positive territory by the end of the month. The recovery was driven by the US Federal Reserve’s (Fed) indication that it would cut interest rates during September, as well as by a stabilisation in initial US jobless claims and upbeat US retail sales. Meanwhile, the Bank of Japan tempered its prior rhetoric of policy tightening.

CBOE Volatility Index (VIX) – price

Source: FactSet, October 2024

When it arrived in September, the Fed’s rate cut was in the form of a larger-than-usual 0.5% reduction.4 The start of the US central bank’s first easing cycle in more than four years was broadly welcomed by market participants, as Chair Jerome Powell underlined the Fed’s commitment to maintaining a low unemployment rate against a backdrop of lower inflation.

While the second quarter of 2024 had been characterised by narrow market leadership and the dominance of mega-cap technology names, Q3 saw a broadening of participation, with solid performance from some more defensive areas of the market and smaller-cap stocks. Meanwhile, after an extended period of weakness, Chinese equities rallied in late September, with the blue-chip CSI 300 index of Shanghai and Shenzhen-listed companies posting its best day since 2008 and rising almost 30% from its trough in February.5 The surge was sparked after the country’s central bank announced its most extensive monetary stimulus measures since the start of the 2020 Covid pandemic, with the aim of restoring confidence in the economy.

Total returns (%) to 30 September 2024

| Asset class | Index | 3 months | 6 months |

| UK equities | FTSE All-Share | +2.3 | +9.9 |

| North American equities | FTSE World North America (£) | +0.1 | +15.5 |

| European ex UK equities | FTSE World Europe ex UK (£) | 0.0 | +7.2 |

| Japanese equities | FTSE Japan (£) | +0.7 | +7.1 |

| Asia-Pacific ex Japan equities | FTSE World Asia Pacific ex Japan (£) | +0.3 | +8.9 |

| Emerging-market equities | FTSE All-World Emerging (£) | +4.8 | +14.6 |

| UK gilts | FTSE Actuaries UK Conventional Gilts All Stocks | +2.3 | -0.2 |

| Corporate bonds | ICE BofA Sterling Non-Gilt | +2.3 | +2.2 |

| Overseas government bonds | JP Morgan Global Government Bond (ex UK) (£) | +1.0 | -2.8 |

| Gold (US$) | Gold ($/ozt SIX) | +13.3 | +27.6 |

| Gold (£) | Gold (£/ozt SIX) | +7.1 | +21.4 |

Source: FactSet, 1 October 2024. All equity market returns are sterling total returns.

The backdrop of declining interest-rate expectations was naturally favourable for bonds, with yields (which move inversely to prices) falling over the period, while the Japanese yen materially outperformed other major currencies. Elsewhere, gold delivered its largest quarterly increase since the first quarter of 2016,6 fuelled by falling interest rates and heightened tensions in the Middle East.

Sterling’s strength over the period meant that returns from overseas investments were muted for UK-based investors.

Regional overview

US Fed Chair Jerome Powell called the central bank’s half-percentage-point September interest-rate cut a “recalibration” intended to account for the sharp fall in inflation since last year, and indicated that the “strong start” to the easing cycle was intended to show policymakers’ commitment to keep any job market weakness at bay.7

Despite steady wage growth potentially boosting consumer spending and helping to ward off a recession, the US Bureau of Labor Statistics’ employment report released on 6 September indicated a slowdown in the labour market, with fewer jobs added in August than anticipated and downward revisions being made to June and July payroll growth figures.8

Powell stated that he thought the economy was still robust, noting that August’s data indicated a slight decrease in the unemployment rate to 4.2% from 4.3% in the previous month. Nevertheless, considering the time delay for monetary-policy adjustments to take effect and taking into account anecdotal reports from companies of reduced hiring rates, Powell argued for swift measures, stating that “the time to support the labour market is when it is strong, and not when you begin to see layoffs”.

The revised ‘dot plot’ projections by Federal Open Market Committee (FOMC) officials forecast that the benchmark interest rate would fall by another half percentage point by the end of this year and a full percentage point in 2025.

In Europe, despite a surge in the French services sector linked to the Olympic Games which bolstered the eurozone’s purchasing managers’ indices in August, September’s numbers revealed a significant contraction in the region’s business activity. Notably, Germany, the largest economy in the bloc, appears likely to have entered a recession as its large manufacturing sector has continued to struggle and growth has slowed in its services sector.

On 12 September, the European Central Bank (ECB) reduced interest rates by 0.25%,9 after a cut of the same magnitude in June, and hinted at further reductions owing to gradually falling inflation and faltering economic growth, with eurozone GDP set to expand by only 0.8% this year.10 ECB President Christine Lagarde observed that services sector inflation was still a concern, but that wage growth had slowed and corporate profits were absorbing rapid wage increases.

More dovish ECB policymakers, mainly from southern European countries, have argued that recession risks are increasing and that high interest rates are hindering growth excessively, increasing the potential for inflation to fall below the central bank’s target. This perspective was supported by Eurostat’s September data, which showed that headline inflation had dropped to 1.8%.11

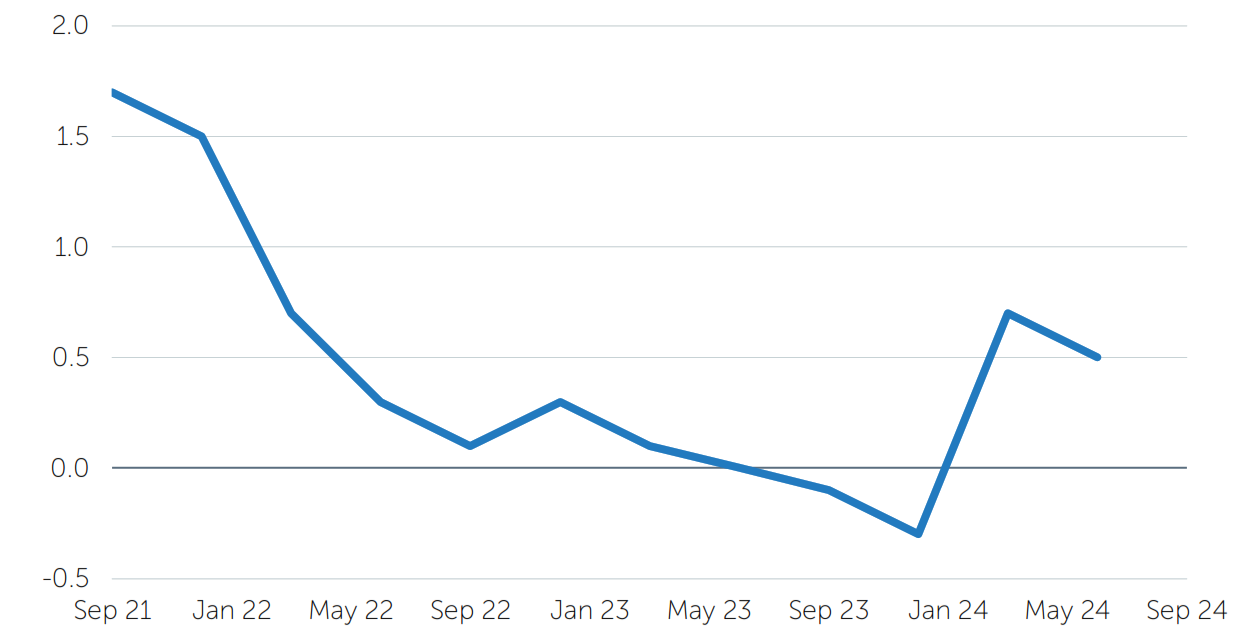

The UK’s economy grew by 0.5%in the second quarter, according to the Office for National Statistics,12 providing some comfort for the country’s new Chancellor of the Exchequer Rachel Reeves as she prepares for her first Budget in late October, when some taxes are expected to rise. In addition, an improvement in the household saving ratio and a robust jobs market could boost consumer spending.

UK GDP

% change, quarter on quarter

Source: FactSet, October 2024

However, in what will have been less welcome news for the chancellor, British government debt rose to 100% of GDP in August for the first time since monthly records began in 1993.13 Bank of England records show that debt was last consistently at this level in the early 1960s, when the UK was still managing the financial after-effects of World War Two.

At its September meeting, the Bank of England kept interest rates on hold following a quarter-point cut in August.14 Governor Andrew Bailey expressed caution owing to persistent wage growth and divided opinions among policymakers on the rate at which long-term inflationary pressures were easing. However, he said he was “optimistic” that rates would fall further.

In late September, Shigeru Ishiba became Japan’s new prime minister, succeeding Fumio Kishida who resigned following a series of scandals. Speaking at a press conference, Ishiba emphasised the importance of boosting consumption to help Japan recover from prolonged economic stagnation.15 Japan’s economy grew by an annualised 2.9% in the second quarter, with real wages increasing for the second consecutive month in July, alleviating concerns about rising living costs affecting consumption.16 However, weak demand from China, slowing US growth and the yen’s recent recovery have posed challenges to the outlook.

Market volatility has remained a significant concern for Bank of Japan policymakers after the turbulence associated with the July interest-rate hike and hawkish comments from Governor Kazuo Ueda. The central bank maintained stable interest rates at its September meeting, and Ueda indicated that there was no immediate plan to increase borrowing costs further, particularly since the yen’s recovery had eased upward pressures on import costs. However, with data showing that Japan’s core consumer inflation accelerated for the fourth consecutive month in August,17 comfortably exceeding the central bank’s 2% target, expectations for additional rate hikes persist.

In a speech marking the 75th anniversary of the People’s Republic of China, the country’s President Xi Jinping warned of “rough seas” ahead,18 which many have taken as a reference to the country’s struggling economy, where deflationary pressures have persisted amid fears of a prolonged structural slowdown.

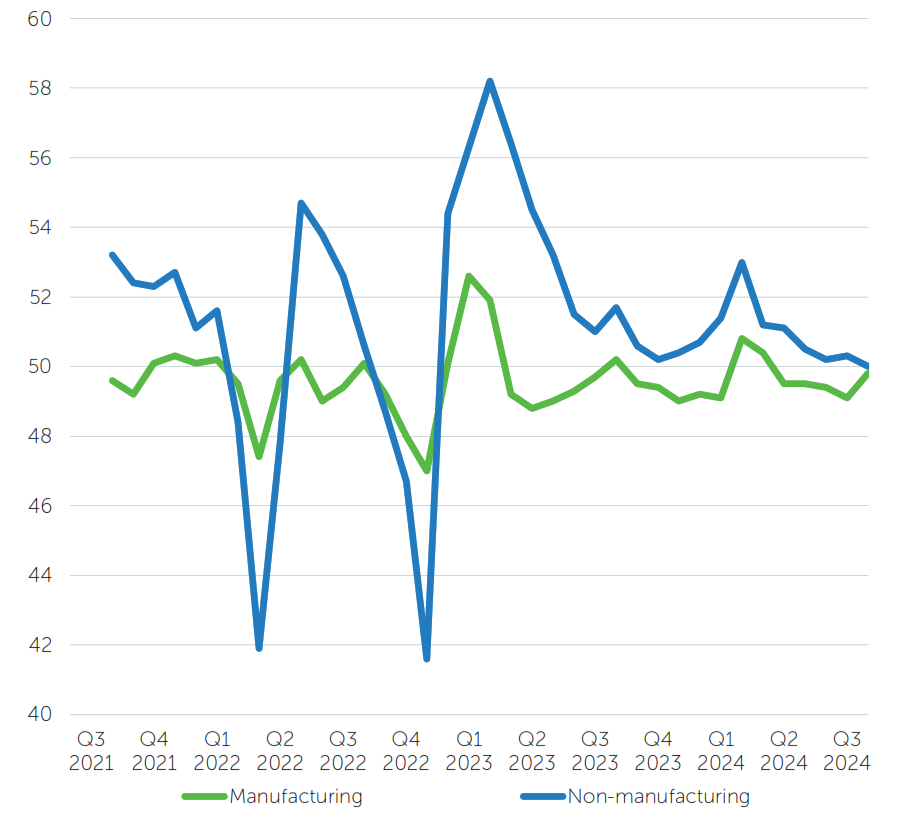

The People’s Bank of China’s extensive monetary stimulus package, announced in late September, includes plans to lower borrowing costs, enhance lending, and support the beleaguered property market. However, it remains to be seen whether it will sufficiently boost growth to meet the government’s annual target of around 5%, or whether further fiscal help will be needed to inject additional demand. Data from China’s National Bureau of Statistics showed that China’s factory activity shrank for a fifth successive month in September, while the services sector slowed.19

China purchasing managers’ indices

Source: FactSet, October 2024

Investment implications

The third quarter of 2024 gave investors plenty to sink their teeth into from a macroeconomic perspective. Perhaps most conspicuously, the Fed finally began to cut interest rates. The US central bank first indicated that its next move would be downwards as far back as December 2023. However, it has been cautious to pull the trigger after incorrectly understating the risk of inflation accelerating in 2021. Some perkier inflation data early this year checked the newfound dovishness, but since then price pressures have resumed their steady deceleration, with the Fed’s favoured measure of inflation – core personal consumption expenditures (PCE) – effectively back to target.

Alongside the continuing decrease in inflation, there has been clear evidence of a cooling in the US labour market. The US continues to create jobs, but there is now a more obvious equilibrium between supply and demand. At the August Jackson Hole Economic Symposium, Fed Chair Powell made it clear that the risks related to the Fed’s dual mandate of price stability and maximum employment had achieved a balance. This scenario prepared the way for the Fed to commence rate cuts at its September meeting, with Powell emphasising that at this point the greater risk was failing to adequately bolster the economy.

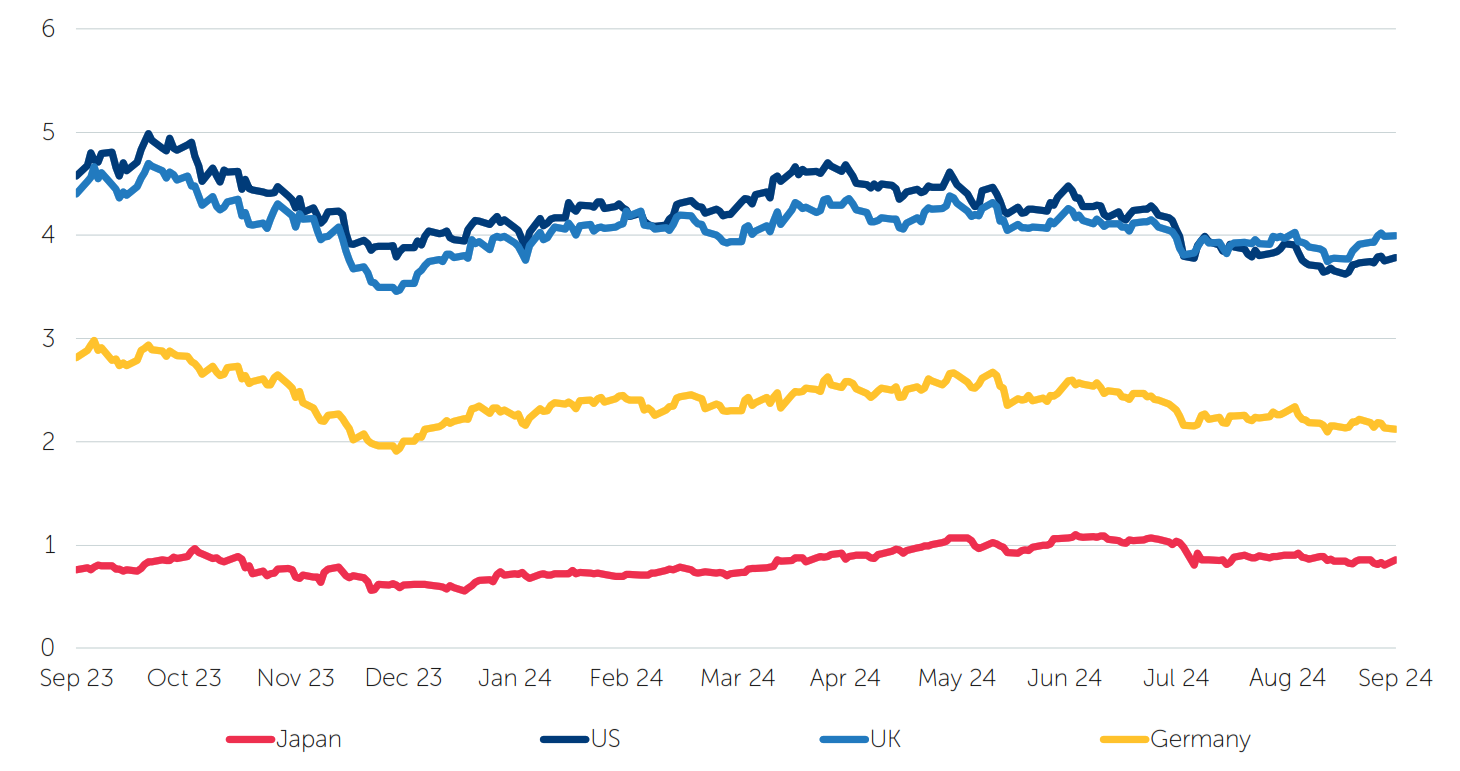

The debate has now moved on to where the terminal rate will land. The market has already priced in what the Fed expects to deliver in the rest of 2024 and 2025, but for yields to continue to decline it is likely that we will need to see signs of a recession in the US economy, which the data does not really support. Although the economy has decelerated, the slowdown might have been expected considering the rapid growth spurred by substantial monetary and fiscal stimulus as the US emerged from Covid lockdowns. While every economic cycle has its idiosyncrasies, it is reasonable to argue that this one has had more than most. Although a continuing slowdown does not necessarily guarantee a recession, many indicators typically associated with recessions are present, thereby raising the likelihood of one in the coming quarters.

10-year government bond yields (%)

Source: FactSet, October 2024

We have previously argued that certain global structural changes would lead to increasingly asynchronous economic cycles between regions. Supporting this view was the Bank of Japan’s (BoJ) decision to raise interest rates at its July meeting. Japan has been the poster child for lower interest rates, but a number of structural and cyclical developments mean that its central bank is likely just to be starting the process of hiking them. The BoJ is likely to move cautiously as it embarks on a rate-raising cycle; nevertheless, divergence between two systemically important central banks (in Japan and the US) is a sign of the times.

The yen appreciated into and out of the BoJ meeting, with the latter stages of the move in the currency coinciding with a spike in cross-market volatility, sparking fears of an unwinding of the yen carry trade. Although this trade deeply influences global financial markets, and more market volatility could result from a stronger yen, we do not believe it poses a systemic risk by itself as some suggest. Instead, it can be seen as an opportunity. Many investors complained that central banks manipulated markets with overly loose monetary policy following the 2008 global financial crisis, and in this context we believe a normalisation of monetary policy can only be a good thing for economic vitality.

Typically, the Fed kicking off a rate-cutting cycle with a jumbo half-percentage-point cut would be the most notable macro development. However, on this occasion, Beijing was unwilling to allow Powell the stage to himself, and the quarter ended with a slew of policy announcements intended to resuscitate the ailing Chinese economy and financial markets.

The Chinese economy has experienced a relative malaise since 2021. Initially this was attributed to draconian Covid lockdowns, but as China exited the pandemic it became clear that its underlying economy was weak versus recent history. In summary, we have been of the view that China has found itself in a ‘balance-sheet recession’ – a recession driven by high levels of private-sector debt (the term was coined by economist Richard Koo in his diagnosis of the Japanese economy after the bursting of its bubble in the late 1980s/early 1990s). Additionally, given the state of the national balance sheet, China has been unable to use fiscal and monetary policy to support the economy while the Fed has been running tight monetary policy. It is not coincidence that China turned its hand to stimulus on the heels of the Fed beginning its rate-cutting cycle.

Although China’s economy still faces structural issues, significant policy easing could bring cyclical improvements. Nevertheless, there are still question marks over whether words will be backed up by action. Historically, this has not always happened, and President Xi has been hesitant to boost the property sector. Even if he has had a change of heart, it is unclear whether the population still trusts property as an instrument of speculation after the authorities’ attempts to deflate property prices. While extreme positioning and negative sentiment towards Chinese equities means the policy inflection has scope to realise a significant equity-market rebound, overcoming the deeper structural challenges facing the Chinese economy is an altogether different challenge.

To summarise, a decisive policy pivot has taken place during the third quarter. The start of the Fed’s easing cycle has paved the way for other central banks, many of which have already begun cutting interest rates, to lower policy rates too. Despite the deliberate economic decoupling of the US and China over almost a decade, the respective economies remain deeply intertwined. Since 2021, China has acted as a deflationary force globally, countering the inflationary trends originating primarily from developed economies, in particular the US and Europe. It would be ironic if an uptick in China’s economy were to reignite global inflationary pressures at a cyclical level just as market participants are becoming confident that the inflation issue has been resolved.

If the Fed’s action successfully halts the nascent deterioration in the labour market, the US economy might achieve a soft landing. Economic acceleration could follow if interest-rate-sensitive sectors respond to Fed easing, potentially extending the cycle. Additionally, with bipartisan agreement in Washington on the merits of using fiscal policy to support the economy, we are likely to see more ‘priming of the pump’, regardless of the outcome of the upcoming presidential election. On the other hand, it is also possible that the Fed’s move has come too late, meaning the die has already been cast for a US recession in the quarters ahead, particularly if China’s stimulus efforts prove inadequate.

Conclusion

After journeying through an eventful third quarter, investors find themselves facing a different set of questions. The Fed’s initiation of a rate-cutting cycle, marked by a notable half-percentage-point reduction, reflects a shift towards easing monetary policies globally, with the ECB and Bank of England among those central banks also cutting rates over the summer.

Policymakers’ key concern over the last couple of years – inflation – has significantly receded but not vanished entirely. Meanwhile, although an economic soft landing remains in prospect for the time being, labour markets are beginning to slow down. Central bankers are therefore striking a delicate balance as they seek to foster continued economic growth while keeping inflation within its target range.

Investors must navigate other developments that create the potential for heightened volatility, including political uncertainty in the US and the escalating conflict in the Middle East. Additionally, the effects of China’s stimulus on both its own and global economies should be closely monitored.

Given this rapidly evolving investment landscape, investors will need to remain vigilant and adaptable in seeking to identify the opportunities and avoid the hazards over the final months of 2024.

It is good to have an end to journey toward; but it is the journey that matters, in the end.

Ursula K. Le Guin, US author, 1929-2018

1 Stonehenge’s hefty Altar Stone came all the way from Scotland, Reuters, 14 August 2024

2 US stocks finish sharply lower to close out global market rout, Financial Times, 5 August 2024

3 Source: FactSet, 30 August 2024.

4 Stocks shine, Treasury yields rise as rate cut stokes risk appetite, Reuters, 19 September 2024

5 China stocks surge in biggest single-day rally since 2008 on stimulus cheer, Reuters, 30 September 2024

6 Source: FactSet, 30 September 2024

7 Fed unveils oversized rate cut as it gains ‘greater confidence’ about inflation, Reuters, 19 September 2024

8 Unemployment falls, suggests orderly US labor-market slowdown, Reuters, 6 September 2024

9 ECB cuts interest rates as growth dwindles, Reuters, 12 September 2024

10 ECB cuts growth forecasts, still sees inflation at target in late 2025, Reuters, 12 September 2024

11 Euro zone inflation dips below 2%, strengthening rate cut case, Reuters, 1 October 2024

12 UK revises down economic growth but signs of strength remain, Reuters, 30 September 2024

13 UK debt hits 100% of GDP, adding to Rachel Reeves’ headache, Reuters, 20 September 2024

14 Cautious Bank of England hold rates, extends bond reduction plan, Reuters, 19 September 2024

15 Shigeru Ishiba to be Japan’s leader, winning on fifth attempt, Reuters, 27 September 2024

16 BOJ signals no rush in raising rates again, keeps policy steady, Reuters, 19 September 2024

17 Japan’s core inflation accelerates for 4th month in August, Reuters, 20 September 2024

18 Xi Jinping forecasts ‘rough seas’ on 75th anniversary of People’s Republic of China, The Guardian, 1 October 2024

19 China’s factory, service sector activity skids, Reuters, 30 September 2024

All data is sourced from FactSet unless otherwise stated. All references to dollars are US dollars unless otherwise stated.

Important information

These opinions should not be construed as investment or other advice and are subject to change. This document is for information purposes only. This is not investment research or a research recommendation for regulatory purposes. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Issued in the UK by Newton Investment Management Limited, The Bank of New York Mellon Centre, 160 Queen Victoria Street, London, EC4V 4LA. Registered in England No. 01371973. Newton Investment Management Limited is authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN and is a subsidiary of The Bank of New York Mellon Corporation. This material may be distributed by BNY Mellon Investment Management EMEA (BNYM IM EMEA) in the UK to professional investors. BNYM IM EMEA, BNY Mellon Centre, 160 Queen Victoria Street, London EC4V 4LA. Registered in England No. 1118580. ‘Newton’ and/or ‘Newton Investment Management’ is a corporate brand which refers to the following group of affiliated companies: Newton Investment Management Limited (NIM), Newton Investment Management North America LLC (NIMNA) and Newton Investment Management Japan Limited (NIMJ). NIMNA was established in 2021 and NIMJ was established in March 2023. MAR006683 Exp 10/2025.