Key Points

- Looking ahead to 2025, navigating ‘known unknowns’ will require investors to be agile in order to capitalize on opportunities while avoiding sudden pitfalls from unforeseen outcomes.

- These known unknowns include how the new US administration may pivot its policies, how its pro-business agenda may influence the Fed, and whether corporate earnings growth can support lofty valuations.

- Investors should consider the implications of a shorter and more shallow monetary policy cycle for their investments, particularly in a market where valuations have become increasingly elevated.

At the beginning of 2024, we advised investors to adopt a ‘balanced’ approach to financial markets and value investing. This recommendation was based on several macro risks present in the market, particularly the uncertainty surrounding the Federal Reserve’s (Fed) ability to achieve a soft economic landing, the outcome of the US elections and the growing concentration of growth and technology stocks in equity indices and investor portfolios. Given the wide range of potential outcomes and the possible volatility associated with each, we believed this ‘balanced’ strategy was prudent to minimize macro risk while focusing on the idiosyncratic opportunities being captured by our investment process.

While some clarity on the aforementioned issues has been achieved, significant uncertainty and skepticism still persist. Looking ahead to 2025, navigating these ‘known unknowns’ will require investors to be agile in order to capitalize on opportunities while avoiding sudden pitfalls from unforeseen outcomes. We believe that experienced active managers with long-tenured teams employing a consistent and repeatable process are best positioned to achieve the right balance in such an environment. Additionally, we maintain that investing in companies characterized by strong and improving fundamentals, attractive valuations and catalyst-driven business momentum may deliver the best investment outcomes for our clients.

It Is Not Where You Start, but Where You End Up

Known: A new administration will take office.

Unknown: How will the policies and promises from the campaign trail change as the new administration looks to make a deal?

Inauguration Day is not until January 20, 2025, but that has not stopped the new administration from presenting ‘opening offers’ on policy and legislation. If President Trump’s second term mirrors his first, these initial offers will likely be negotiated, and likely softened, as he looks to secure favorable deals for the US.

In our view, the administration is attempting to capitalize on a relatively tight window when the government is unified in hopes of progressing its agenda ahead of the mid-term elections in 2026. Otherwise, it may face a divided government. Key priorities in 2025 are expected to include taxes, tariffs and regulation.

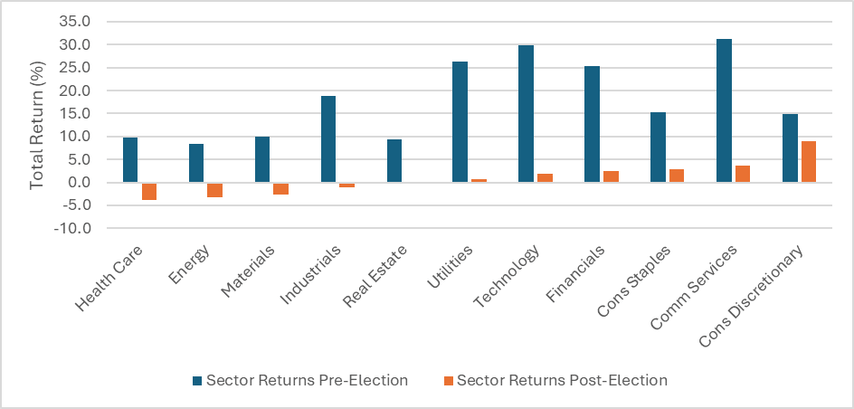

From an investing perspective, the financial markets have already started to price in some of the potential outcomes based on these opening offers. Since the election, consumer discretionary, communication services, consumer staples and financials have been the top-performing sectors, likely owing to expectations that these areas should benefit from a pro-growth agenda that includes maintained or reduced taxes and deregulation. Conversely, health care and energy have been the two weakest sectors, due to concerns they could be adversely affected by potential new policies and actions.

It is uncertain which campaign policies will become reality in 2025. However, skepticism is welcome as it may create attractive entry points, particularly among idiosyncratic opportunities.

S&P 500 Sector Performance Pre and Post US Election

Source: Newton Investment Management North America and Morningstar Direct, as of December 10, 2024.

The Fed and the Political Economy

Known: The US Federal Reserve is progressing toward achieving a soft landing for the US economy.

Unknown: How will the new administration’s pro-business agenda influence the Fed’s mandate of managing inflation while ensuring employment and fostering economic growth?

In addition to the uncertainty about the final form of legislation, there is also uncertainty regarding the impact of the new administration’s pro-business initiatives on economic growth, inflation and interest rates. Additionally, the effects of other initiatives, such as the proposed Department of Government Efficiency (DOGE), on key economic metrics such as employment are also unknown.

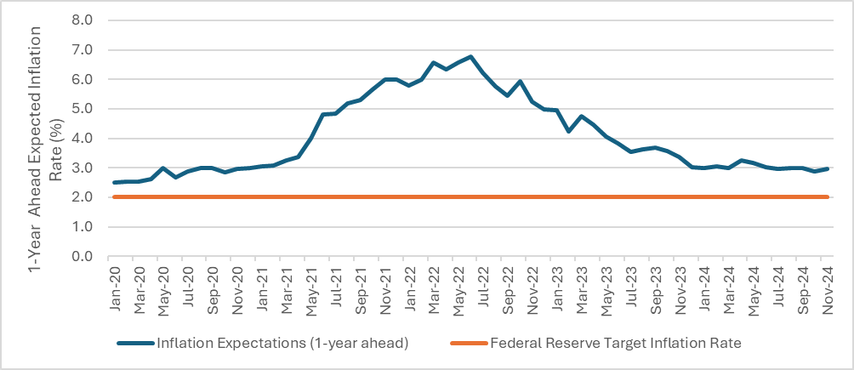

The market’s initial reaction, shown by the rise in the US 10-year Treasury yield after the election, suggests some policies might cause inflation and affect monetary policy. While we will be monitoring this very closely, we were already of the mindset that inflation would be higher and more persistent and, therefore, interest rates would need to be higher for longer.

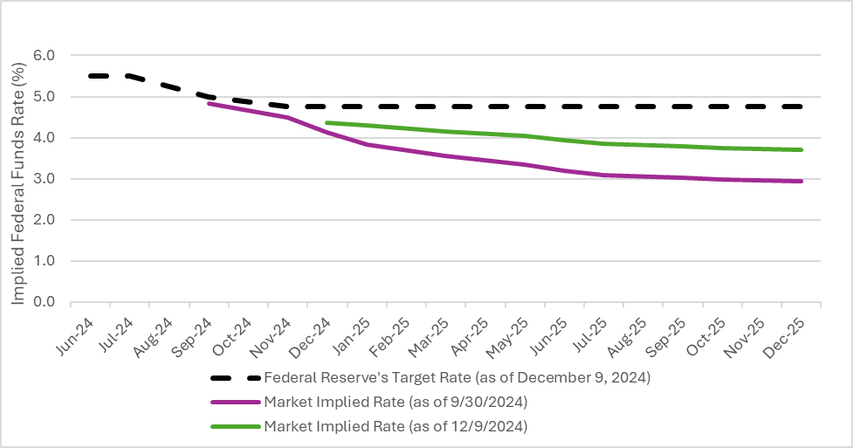

As noted in last year’s outlook, one area of persistent volatility is the ongoing disparity between market expectations for monetary policy and the actual decisions made by the Fed. While this is not a new risk, it is somewhat reassuring that market forecasts for rate cuts in 2025 have moderated. However, investors should consider the implications of a shorter and more shallow monetary policy cycle—where interest rates settle higher than anticipated—for their investments, particularly in a market where valuations have become increasingly elevated.

Inflation Expectations versus Federal Reserve Target Rate

Source: Newton Investment Management North America and Bloomberg, as of December 10, 2024.

Federal Funds Rate versus Market Expectations

Source: Newton Investment Management North America and Bloomberg, as of December 10, 2024.

Finding Value in an Increasingly Expensive Market

Known: US equity markets on aggregate are looking expensive on a valuation basis

Unknown: Can corporate earnings growth support lofty valuations (and expectations)?

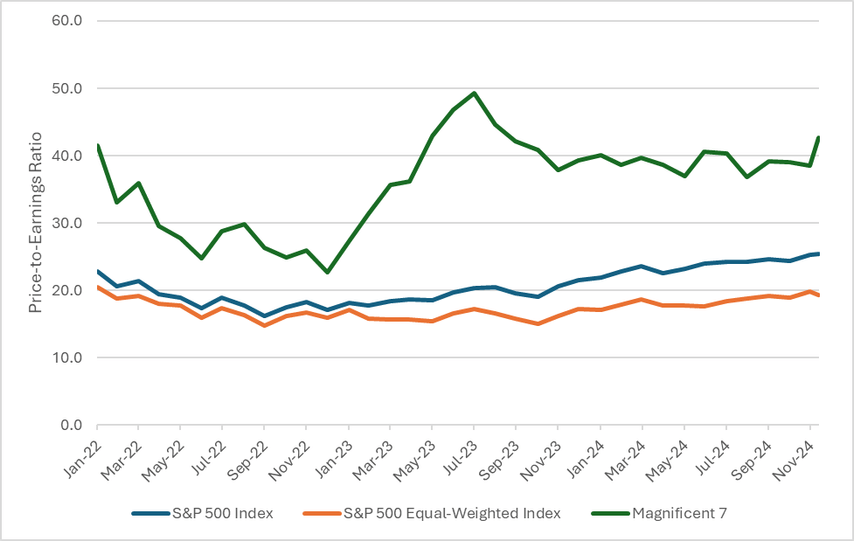

Throughout 2024, we were frequently asked if there were any pockets of value in an increasingly expensive and concentrated US equity market. As we highlighted in The Time is (Always) Right for Value Investing, expensive stocks have continued to rise in valuation. Meanwhile, US market indices and client portfolios have become more concentrated in growth, technology and artificial intelligence (AI)-related stocks.

As shown below, since the start of 2023, multiple expansion in the ‘magnificent seven’ technology stocks (green line) has pulled overall market valuations higher (blue line). The key unknown for 2025 may be whether their earnings can sustain lofty valuations, and if these stocks are already priced for perfection. Another unknown is what could trigger another period of multiple contraction and a growth-led market drawdown, similar to what occurred in 2022.

Market Valuations Pulled Higher by Magnificent Seven

Source: Newton Investment Management North America and Bloomberg, as of December 10, 2024.

How to Position?

We find value throughout the market, but it requires looking below the index level and on a stock-by-stock basis to find it. The silver lining of this uncertainty may be a resulting market volatility that creates compelling investment opportunities.

Active managers often claim the year ahead will favor stock pickers. Given the unknowns articulated above, it is wise to have a flexible manager that can identify opportunities for growth during market upswings while protecting capital during downturns.

Above all, we believe an active, well-balanced process with a focus on company fundamentals, valuations and catalyst-driven business momentum is best suited for this environment. This helps address market skepticism and identify marginal changes for unlocking opportunity.

Authors

Chris Hazelton

Global investment strategist

Newton US large cap value & income team

Insights from the Newton US large cap value & income team

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR006956 Exp 12/29. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.