Key points

- Growth stocks have posted outsized returns, but a changing economic outlook and elevated valuations could limit future gains.

- Slowing earnings-growth momentum and concerns about lofty valuations lead us to reiterate our view that investors should rebalance toward value-oriented stocks.

- We believe companies with strong and improving fundamentals, attractive valuations and business momentum will prove to be solid investment opportunities and lead to better investment outcomes for our clients.

In late 2024, we made a case for US large-cap value investing in The Time Is (Always) Right for Value Investing. We believed that a return to a pre-2008 global financial crisis macro environment would normalize growth/value performance. Second, we observed a rising concentration risk, as equity markets—and investor portfolios—were increasingly exposed to the “magnificent seven” (M7), a narrow group of expensive large-cap growth stocks. We argued for rebalancing, rather than fully rotating, toward US large-cap value as we did not see an obvious catalyst for a change in market leadership.

In our 2025 outlook, we reiterated our recommendation to rebalance as the supporting factors were unchanged in our view. Today, however, we are seeing evidence that some of the key drivers of growth leadership, such as aggressive US monetary-policy easing and US leadership in artificial intelligence (AI) development, are softening. This has led to large cap growth’s performance lagging value year to date. While this period is short, it emphasizes the importance of maintaining a balanced allocation to include US large-cap value.

Investors Starting to Embrace “Higher for Longer”

Already in 2025, the Federal Reserve (Fed) held its January meeting and Fed Chair Powell appeared before Congress in February for his semiannual testimony. In both instances, he reiterated that the central bank “doesn’t need to rush to adjust interest rates” and would be “patient before lowering borrowing costs further.” The Fed’s message was quickly reflected in market-based expectations.

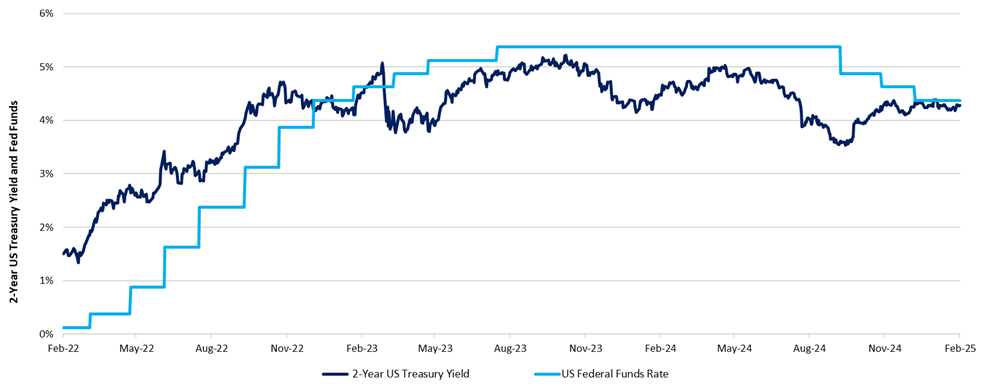

As the chart below illustrates, the 2-year US Treasury yield, which traded below the fed funds rate for over a year on the expectation that interest rates would be moving lower imminently, has recently converged with the fed funds rate.

US Federal Funds Rate vs US 2-year Treasury Yield

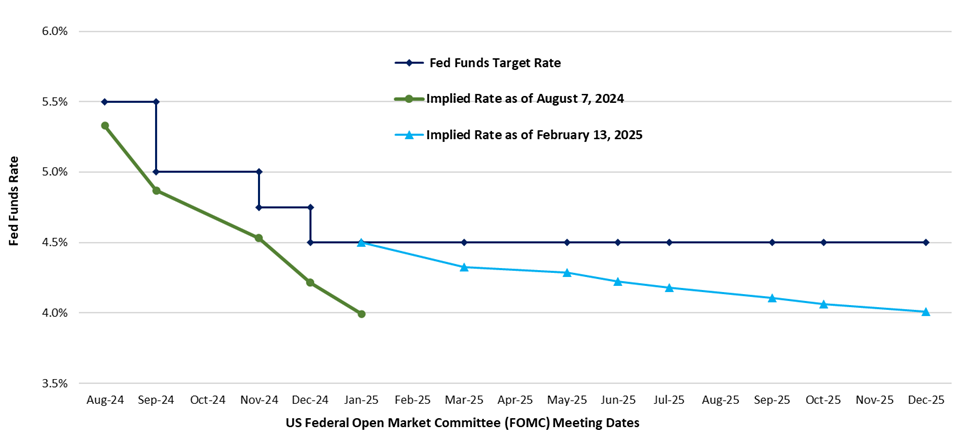

In addition, the market-implied fed funds rate indicates that investors now expect rates to fall later and less than previously thought. In August 2024, the market expected the rate to be 4% by January 2025. However, following the January Fed meeting and Chair Powell’s February testimony, the market now anticipates reaching 4% by December 2025, almost a full year later.

Current Federal Funds Rate vs Market Implied Federal Funds Rate

Changes in interest-rate expectations have typically been a big driver of relative style performance, but it has been particularly pronounced since the global financial crisis. The Fed’s low- and zero-interest rate policy helped growth outperform value in the 12 years leading up to the Covid-19 pandemic, and again after inflation peaked in 2022. With interest-rate expectations beginning to reflect the Fed’s higher-for-longer stance, we think value-oriented securities are poised to deliver competitive returns relative to growth.

Magnificent Seven Taking a Breather?

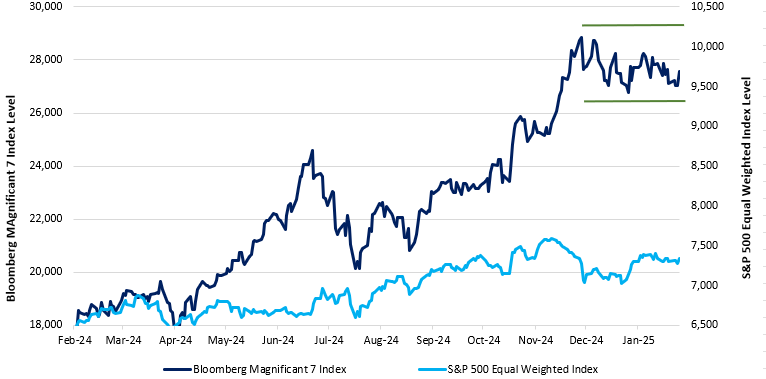

US equity market gains over the past year were driven primarily by the M7. More recently, a subset has separated themselves owing to their leadership in AI innovation, development and spending. Lately, however, these stocks have taken a bit of a breather as investors review their assumptions about US leadership in AI. The key catalyst for this was the emergence of Chinese AI developer DeepSeek, which boasted a new platform that is reportedly more economic and energy-efficient than its US counterparts.

One-Year Performance of the Magnificent Seven vs the S&P 500® Equal-Weighted Index

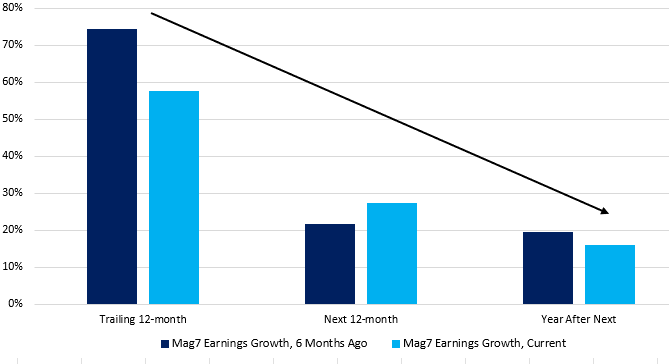

Investors are likely to further scrutinize the M7 companies’ future earnings growth to determine if expected earnings can still support lofty valuations. Looking at the earnings data through the end of January, this pause among the M7 seems warranted. As the chart below illustrates, earnings growth, while still relatively strong, is forecast to decelerate over the coming year.

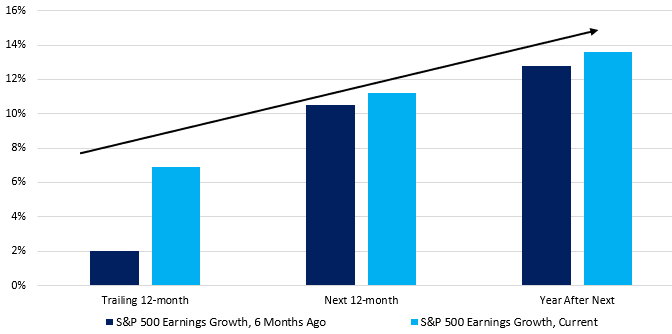

Earnings Growth Still Strong, but Decelerating

Meanwhile, earnings growth for the broader market is being revised higher from where consensus expected it six months ago and looks set to accelerate higher through 2026, which would support the case to balance out exposure beyond a small set of companies.

Earnings Growth Accelerating

Conclusion

We believe companies and investors continue to adjust to US inflation and interest rates normalizing—not to pre-Covid levels, but to those before the global financial crisis. We expect inflation to remain higher and more persistent than in the previous 12 years, likely prompting the Fed to keep rates elevated. The macro environment, combined with concentration risk in the M7 stocks, changing momentum in earnings growth and concerns about lofty valuations, leads us to reiterate our view that investors should rebalance toward value-oriented stocks. Within the value space, we believe companies with strong and improving fundamentals, attractive valuations and business momentum will prove to be solid investment opportunities and lead to better investment outcomes for our clients. We think our consistent and repeatable investment process is well suited to identify these types of opportunities.

Authors

Chris Hazelton

Global investment strategist

Newton US large cap value & income team

Insights from the Newton US large cap value & income team

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell this security, country or sector. Please note that strategy holdings and positioning are subject to change without notice. MAR007128. Exp 3/30. For additional Important Information, click on the link below.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC ("NIMNA" or the "Firm"). NIMNA is a registered investment adviser with the US Securities and Exchange Commission ("SEC") and subsidiary of The Bank of New York Mellon Corporation ("BNY"). The Firm was established in 2021, comprised of equity and multi-asset teams from an affiliate, Mellon Investments Corporation. The Firm is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand "Newton" or "Newton Investment Management". Newton currently includes NIMNA and Newton Investment Management Ltd ("NIM") and Newton Investment Management Japan Limited ("NIMJ").

Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.

Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment and past performance is no indication of future performance.

Information about the indices shown here is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison.

This material (or any portion thereof) may not be copied or distributed without Newton’s prior written approval.

In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario and the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations.

Comments