Economic And Market Background

In what is set to be the biggest election year in history, with four billion people – more than half the world’s population – going to the polls,1 financial-market participants were on edge during the second quarter as a series of high-stakes votes spurred market volatility.

Although it subsequently recovered, India’s stock market experienced its worst day in more than four years at the start of June after Prime Minister Narendra Modi’s Bharatiya Janata Party unexpectedly lost its parliamentary majority,2 putting at risk an aggressive reform agenda. In France, President Emmanual Macron called a snap parliamentary election after the far-right National Rally made major gains at the expense of his centrist alliance in the June European Parliament elections. With the prospect of a new government adding significantly to France’s already large debt pile, the spread on 10-year French government bonds (the extra return investors demand to buy France’s debt over Germany’s) reached its highest level since the 2012 eurozone crisis.3

Meanwhile, UK Prime Minister Rishi Sunak called a general election for July 4, an earlier date than many had predicted, and a stumbling performance from US President Joe Biden in a TV debate with his rival Donald Trump at the end of June heightened the uncertainty surrounding the November election in the world’s largest economy.

Nevertheless, global equity markets made further gains over the quarter, driven by technology stocks and especially the ‘magnificent seven’ mega-cap businesses, which helped the S&P 500 and Nasdaq indices of US stocks to reach new record highs in June. Notably, Nvidia, the leading supplier of chips used to train artificial intelligence (AI) models, briefly became the world’s most valuable company on June 18 as its market capitalization reached more than $3.3 trillion.4 The company’s shares rose by a staggering 150% over the first six months of the year, and the stock alone has been responsible for around 30% of the S&P 500’s gains over the same period.5 The dominance of a small number of technology names has fueled growing concerns over market concentration.

Equity markets did come under pressure at times, especially in April, as hopes of interest-rate cuts were dampened amid signs of continued strength in the US economy and stubborn inflation. On top of this, geopolitics returned to the fore as tensions in the Middle East between Israel and Iran briefly escalated, driving a spike in energy prices.

Towards the end of the quarter, the US Federal Reserve (Fed) reaffirmed a hawkish narrative as it left interest rates unchanged at its June meeting, with the median forecast from its policymakers projecting just one rate cut before the end of the year.6 However, with US monthly inflation unchanged in May according to the Fed’s preferred personal consumption expenditures (PCE) measure, as a small increase in the cost of services was offset by the biggest fall in goods prices in six months,7 hopes were boosted for an economic ‘soft landing’ in which inflation cools without triggering a recession and a sharp rise in unemployment.

Elsewhere, the European Central Bank (ECB) moved ahead of its US and UK counterparts as it lowered borrowing costs for the first time in almost five years, reducing its deposit rate by 0.25% to 3.75%,8 although it would not commit to a specific path for future cuts, partly owing to persistent price and wage pressures. In contrast, the Bank of Japan opted to keep its short-term target rate unchanged at 0-0.1% at its June meeting, although it announced that it would provide more details in late July of a plan to start trimming bond purchases.9 Affected in part by the continuing interest-rate differential with the US, the yen slumped to a 38-year low against the US dollar during the quarter.

With market participants adjusting their expectations for near-term rate cuts downwards, government bonds struggled over the quarter, with the yield on the benchmark 10-year US Treasury rising by around 18 basis points. Gold, meanwhile, made its third successive quarterly gain, hitting a record high in May.10

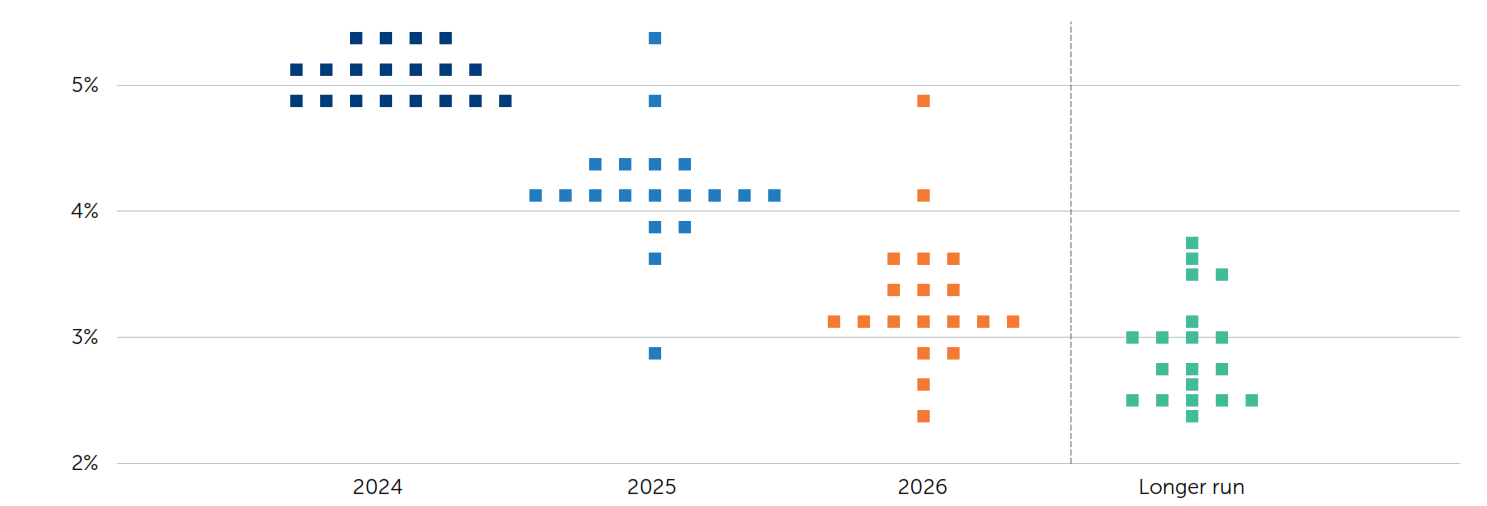

Interest-Rate Projections by Members of the Federal Open Market Committee

Each dot indicates the value of an individual participant’s judgement of the appropriate target level for the federal funds rate at the end of the specified calendar year or over the longer run.

Source: US Federal Reserve, June 12, 2024.

Total Returns (%) to June 30, 2024

| Asset class | Index | 3 months | 6 months |

| North American equities | MSCI North America | +3.8 | +14.3 |

| European equities | MSCI Europe | +0.9 | +6.4 |

| UK equities | MSCI United Kingdom | +3.7 | +6.9 |

| Japanese equities | MSCI Japan | -3.8 | +6.5 |

| Asia-Pacific ex Japan equities | MSCI AC Asia Pacific ex Japan | +6.6 | +8.6 |

| Emerging-market equities | MSCI Emerging Markets | +5.4 | +7.7 |

| Corporate bonds | ICE BofA Global Corporate | -0.1 | -0.8 |

| Global government bonds | JP Morgan Global Government Bond | -1.9 | -4.6 |

| Gold (US$) | Gold ($/ozt SIX) | +4.2 | +12.6 |

Source: FactSet, July 1, 2024. All equity market returns are US-dollar total returns.

Regional Overview

Figures from the US Commerce Department’s Bureau of Economic Analysis indicated that the US economy grew at 1.4% during the first quarter of 2024, its slowest pace in almost two years.11 However, while the trade deficit widened, domestic demand remained resilient, with a pickup in business investment and a continued housing recovery. According to the Labor Department, non-farm payrolls rose by 272,000 in May, far ahead of consensus expectations.12

Hiring has been strong across the breadth of the economy, with the health-care sector providing the biggest employment gains as companies have sought to increase staffing levels after losing workers during the Covid pandemic. Wage growth also accelerated, rising 4.1% year on year.

The Fed expects inflation to decline gradually, with the PCE price index forecast to be virtually unchanged from its current level at the end of the year, as growth remains slightly above trend and unemployment stays low. The Federal Open Market Committee indicated in its June policy statement that while “modest further progress” has been made towards its 2% inflation objective, interest-rate reductions would not be appropriate until it has “gained greater confidence” that price pressures will continue to ease.13

In contrast to its US counterpart, the European Central Bank decided to begin its easing cycle in June but has similarly cautioned over the timing of any future moves, stressing how it will continue to follow a “data-dependent and meeting-by-meeting approach”, with many economists predicting there will be no more than two further cuts this year.

The eurozone’s economy jumped back from a mild recession in the first quarter as Germany, its largest economy, returned to growth, while the French and Spanish economies also gained some momentum.14 There was further positive news, with a key indicator showing that business activity had expanded at its quickest rate in a year in May, as a result of an expanding services industry. The HCOB purchasing managers’ index rose to 52.2 and remained above 50 (the level which separates growth from contraction) for the third consecutive month.15

Nevertheless, with Europe’s manufacturing sector still in contraction, overall growth is expected to be sluggish. The International Monetary Fund (IMF) has forecast that the eurozone’s GDP will rise by just 0.8% in 2024, not least because consumer sentiment in France and Germany remains weak.

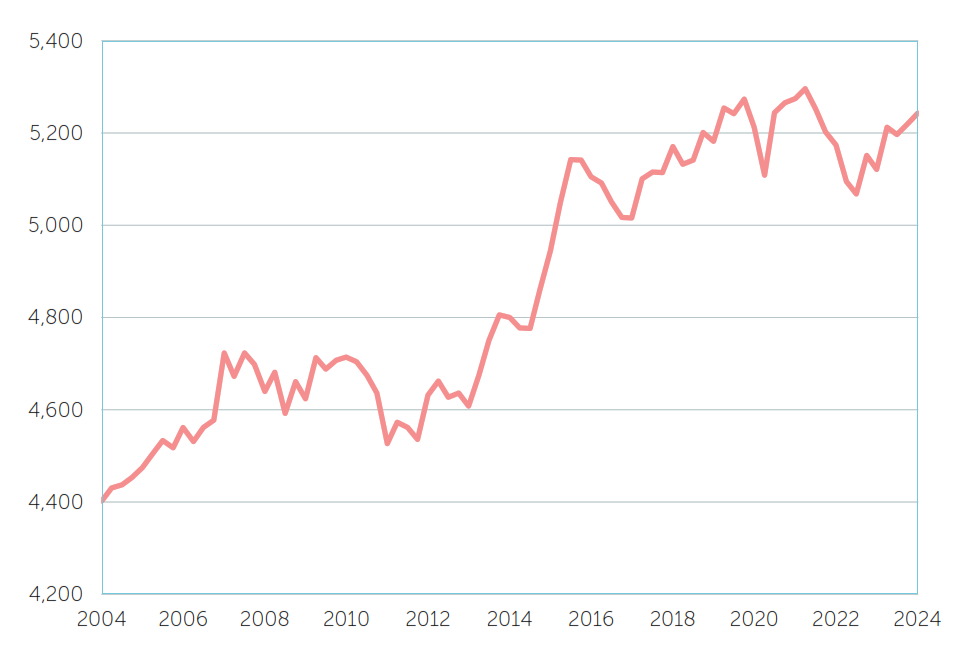

Ahead of its general election, the UK received some positive economic news which indicated that the economy had bounced back from recession, with GDP expanding by 0.7% in the first three months of the year from the previous quarter, according to the Office for National Statistics.16 Real (inflation-adjusted) household disposal income per head also increased by 2.4% over the last year, boosted by fast wage growth in a tight labor market. Nevertheless, it was still 0.6% lower than in the final quarter of 2019, just before the start of the pandemic.

UK Households: Real Disposable Income per Head

Chained volume measure £, seasonally adjusted

Source: UK Office for National Statistics, June 28, 2024

At its June meeting, the Bank of England’s Monetary Policy Committee (MPC) voted to keep interest rates on hold, although its policy minutes indicated the decision had been “finely balanced” for some MPC members.17 Headline consumer price inflation returned to its 2% target in May for the first time in almost three years, but the central bank expects it to rise again later in the year once the effects of past energy price declines have fallen out of annual inflation data. Services price inflation has remained significantly higher at 5.7%, and pay growth remains elevated.18

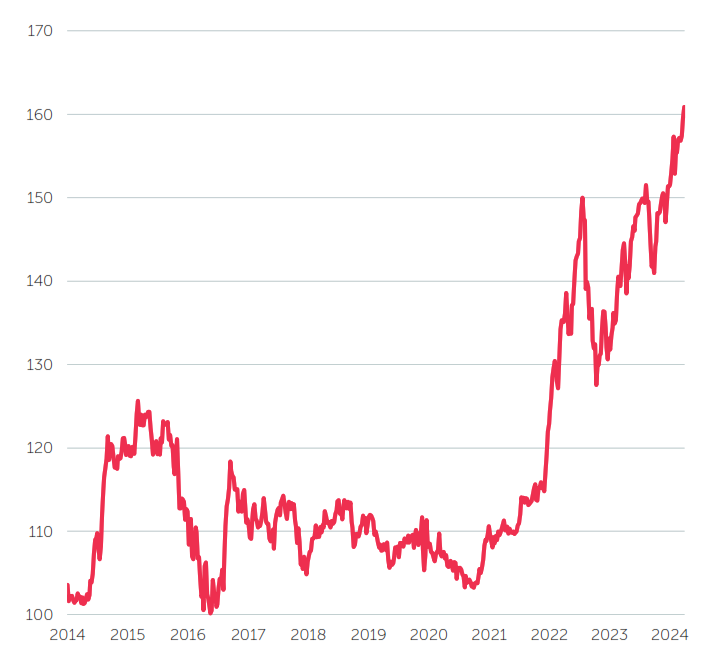

While the Bank of Japan (BoJ) kept interest rates on hold in June, it hinted that a hike may be on the cards at its meeting scheduled for the end of July, as it also seeks to start cutting its bond purchases and reducing the size of its enormous balance sheet, which currently represents around 125% of the country’s GDP.19 The weakening yen has put further pressure on the BoJ as rising import costs threaten to push inflation well above its 2% target.

The central bank’s decision will be complicated, however, by a revision to GDP data which suggested that Japan’s economy may have shrunk by 2.9% on an annualized basis in the first quarter.20 This was more than initially reported and is likely to result in a cut to growth forecasts. Domestic consumption has been weak as households and small businesses have been squeezed by the higher costs of imported goods, although the tourism sector and exports have benefited from a more competitive exchange rate. Policymakers are hoping that large pay rises agreed with Japanese companies in April, and planned income tax cuts, will provide a boost during the second half of the year.

US Dollar/Japanese Yen Rate

Source: FactSet, July 2024

After China’s GDP jumped by 5.3% in the first quarter compared to the previous year, beating expectations, the IMF upgraded its growth forecast, saying it expects China’s economy to grow by 5% in 2024.21 In May, China announced what it termed “historic” steps to stabilize its troubled property sector. State-owned firms are set to buy some apartments, while China’s central bank is introducing a relending facility for affordable housing and is further lowering mortgage interest rates and downpayment requirements. While these policy measures could take time to take effect, data for May suggested a further worsening in the property sector, with both investment and new home prices declining further.

Manufacturing investment showed strong growth of 9.6% in the first five months of the year,22 underpinned by policy support, and exports have helped to boost the economy. However, the European Union’s announcement in June that it intends to impose tariffs of up to 38% on imports of Chinese electric vehicles highlights potential trade challenges to come.23

Investment Implications

During the year so far, and indeed for most of 2023, financial-market participants have been considering when economies would react negatively to increases in interest rates. The impact of higher rates appears to have been gradual, which has led some central banks to start cutting rates and others to talk about cutting them later this year. With inflation having declined from its peak, central banks have some leeway to reduce rates from their elevated levels.

For risk assets such as equities, the gradual economic slowdown, easing of inflation and ‘dovish’ central bank narrative have been sufficient to extend rallies. As market participants continue to debate the likelihood of a more significant economic slowdown, they will be evaluating the legacy of the build-up in government debt and stubborn inflation levels, as well as the potential impact of political change. We believe this trio of influences will continue to cause volatility in markets in the second half of 2024 and beyond.

In terms of the outlook for growth, the much-heralded ‘soft landing’ appears to be within reach, especially if central banks are quick to take the top off their high cash rates. However, in our view, the odds of a downturn becoming more severe and developing into a proper hard landing are higher than the possibility of world economic growth reaccelerating and pushing inflation (and then interest rates) to new highs. On balance, the soft-landing scenario still appears most likely, but it has previously proved a difficult act for central bankers to pull off.

Once employment slows, along with investment, it can affect consumer confidence and therefore spending, leading businesses to reduce their inventories and, in turn, employment. This then depresses consumer sentiment further, and a full-blown recession can quickly emerge. The good news is that central banks have significant room to cut interest rates to arrest an accumulation of negative sentiment.

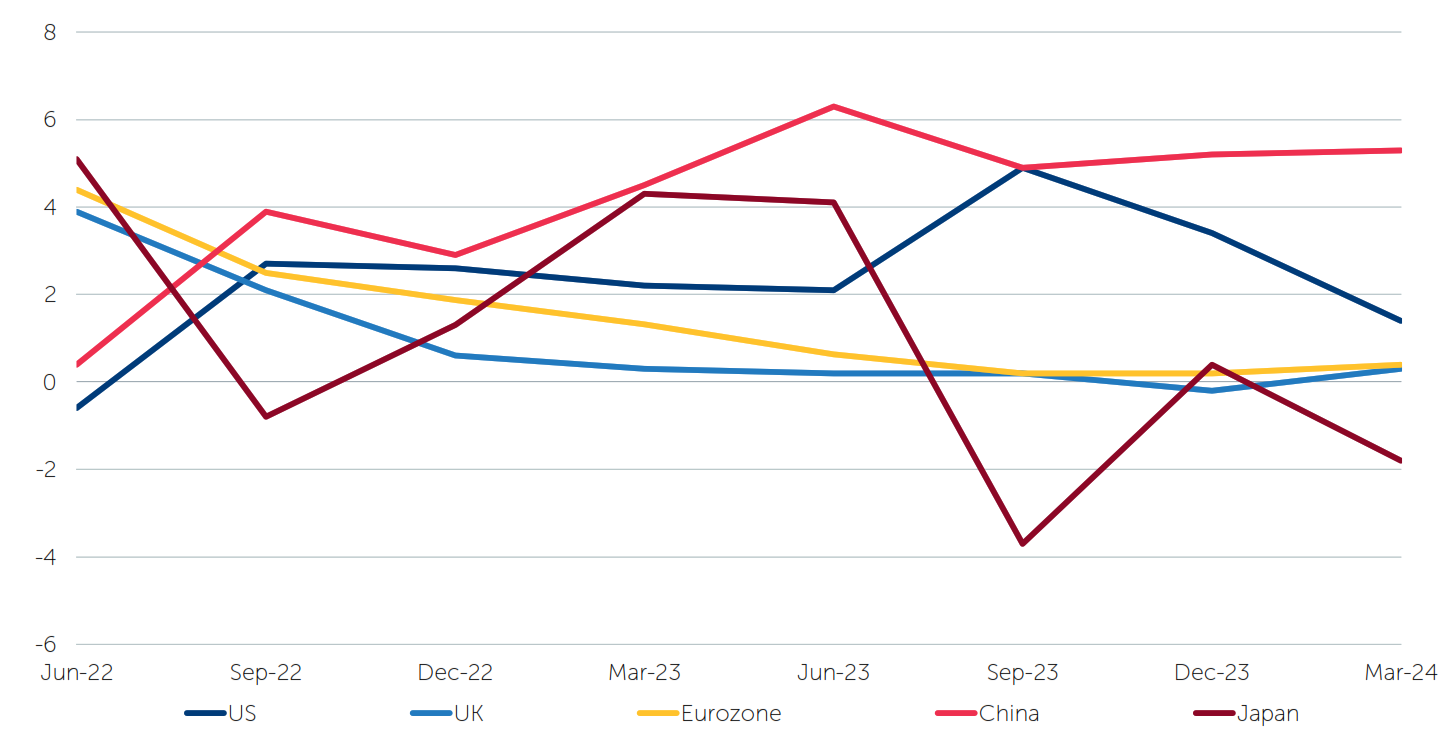

One feature of the current economic landscape is the continued global divergence in growth. Notably, the US economy has experienced persistently strong GDP growth, benefiting from its domestic energy sources, large fiscal stimulus and innovation in its technology sector. Europe has struggled as it has had to contend with (until recently) higher energy costs, combined with a lack of innovation. China, meanwhile, has continued to work through the legacy issues related to the crisis in its property sector. Heavy investment in new technologies, however, has given it the edge in producing electric vehicles and renewable-energy infrastructure, thereby exporting deflation to the rest of the world and prompting tariff increases from some countries. Other emerging-market economies are a mixed bag, but many have the ability to cut domestic rates if inflation continues to fall.

Real GDP Growth

% change, year on year

Source: FactSet, July 2024

Political noise has been an increasing concern for markets since the 2008 global financial crisis and the eurozone sovereign debt crisis that followed. Growing wealth inequality, as income and living standards stagnated for many while the wealthy benefited from rising asset prices, left many voters disenchanted with incumbent, largely centrist, governments, and fueled demand for more radical policies. The economic effects of the Covid pandemic later accelerated this trend. Once in office, populist politicians have tended to be as hamstrung by debt and low productivity as their predecessors, and many get ejected, prompting voters to look for the next party or leader that promises an easy or radical fix to complex problems.

Political change can be unnerving for market participants if they do not know what comes next, but recent developments have rarely led markets to avert their focus from the economy and rates. After an initial wobble, markets have tended to continue their upward journey. The exceptions to this trend can come when governments threaten the durability of their debt (as occurred with former UK Prime Minister Liz Truss’s short-lived government in 2022) or interfere with the independence of their central banks (as happened in Turkey in 2023).

In the past, investors could usually look beyond a forthcoming election and invest through any short-term volatility, but now we are increasingly seeing elections with the potential (albeit still small) to cause a major upset.

In addition to politics, the outlook is clouded by high levels of government debt which must somehow be serviced. While we are not suggesting current levels of debt are unsustainable, the cost of servicing this debt has risen significantly over the last two years. In the UK, government debt interest payments now represent a greater cost (as a percentage of GDP) than education, defense or economic investment. The UK is not alone, and many governments face the same challenge of needing to increase health and defense spending while trying to pay for past support through a higher interest bill. This will severely limit any government’s ability to stimulate economic growth in the future. Some relief can come from lower official rates, but with inflation likely to remain consistently above 2% targets in many economies, interest-rate relief will have its limits.

When government debt increases, private-sector debt tends to fall, and this has indeed happened over the period since the global financial crisis. This puts the private sector in a better credit position and means that the next economic slowdown is more likely to be a cyclical one, which can be tackled with lower rates, rather than a systemic version that can be more difficult to bounce back from.

Conclusion

The global economy appears to have been more resilient than many had anticipated, with the US in particular seemingly absorbing the impact of higher interest rates, at least for now. As a result, a soft economic landing remains in prospect, especially as central banks have some flexibility to lower interest rates.

However, while inflation has moderated, it remains above target in major economies, which is limiting that flexibility. The mounting effects of higher rates are likely to weigh on economic activity as the year progresses, and elevated debt levels will make it difficult for governments to offer significant stimulus should a bigger downturn develop.

Investors must also contend with rising international and domestic political tensions which could spark market volatility, especially as key elections, notably in the US, approach.

With the ‘benign’ low-inflation and low-rate conditions of the previous decade now firmly behind us, there is likely to be greater divergence in the performance of economies, asset classes, and individual securities. We believe it will therefore be critical for investors to identify the long-term growth opportunities in areas supported by structural demand and pay close attention to fundamentals in order to separate the winners from the losers.

A politician thinks of the next election. A statesman, of the next generation.

James Freeman Clarke, American minister, theologian and author, 1810-1888

1 2024 is the biggest election year in history, The Economist, November 13, 2023.

2 Indian shares post worst day in 4 years as polls show unexpectedly narrow Modi win, Reuters, June 4, 2024.

3 French debt risk premium hits highest since 2012 crisis ahead of election, Reuters, June 28, 2024.

4 Nvidia eclipses Microsoft as world’s most valuable company, Reuters, June 18, 2024.

5 Tech boom leads global markets through first half of 2024, Reuters, July 1, 2024.

6 Fed leaves rates unchanged, sees only one 2024 cut despite inflation progress, Reuters, June 12, 2024.

7 US inflation cools in May, boosting hopes of Fed rate cut, Reuters, June 28, 2024.

8 ECB cuts rates, keeps next move under wraps, Reuters, June 6, 2024.

9 Bank of Japan to trim bond buying, keeps rates steady, Reuters, June 14, 2024.

10 Source: FactSet, July 1, 2024.

11 Gross Domestic Product (Third Estimate), Corporate Profits (Revised Estimate), and GDP by Industry, First Quarter 2024, Bureau of Economic Analysis, June 27, 2024.

12 US job gains surge past expectations, wage growth quickens, Reuters, June 7, 2024.

13 Federal Reserve issues FOMC statement, federalreserve.gov, June 12, 2024.

14 Euro zone rebounds from recession as inflation steadies, Reuters, April 30, 2024.

15 Euro zone business activity expands at fastest rate in a year, Reuters, June 5, 2024.

16 UK economy picks up in early 2024, too late for election boost, Reuters, June 28, 2024.

17 Bank of England keeps rates at 5.25% ahead of UK election, Reuters, June 20, 2024.

18 UK inflation drops to 2% target for first time since 2021, Reuters, June 19, 2024

19 Bank of Japan opens door for a hawkish double surprise, Reuters, June 26, 2024

20 Japan downgrades Q1 GDP on construction data corrections, Reuters, July 1, 2024

21 IMF upgrades China’s GDP growth forecasts but warns of risks ahead, Reuters, May 29, 2024.

22 China’s factory output disappoints, property sector stuck in doldrums, Reuters, June 17, 2024.

23 EU to put tariffs of up to 38% on Chinese electric vehicles as trade war looms, The Guardian, June 12, 2024.

All data is sourced from FactSet unless otherwise stated. All references to dollars are US dollars unless otherwise stated.

Important information

For Institutional Clients Only. Issued by Newton Investment Management North America LLC (“NIMNA” or the “Firm”). NIMNA is a registered investment adviser with the US Securities and Exchange Commission (“SEC”) and subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”). The Firm was established in 2021 and is part of the group of affiliated companies that individually or collectively provide investment advisory services under the brand “Newton” or “Newton Investment Management”. Newton currently includes NIMNA, Newton Investment Management Ltd. (“NIM”) and Newton Investment Management Japan Limited (“NIMJ”).This document is provided for general information only and should not be construed as investment advice or a recommendation. You should consult with your advisor to determine whether any particular investment strategy is appropriate. Statements are current as of the date of the material only. Any forward-looking statements speak only as of the date they are made, and are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking statements. Material in this publication is for general information only. The opinions expressed in this document are those of Newton and should not be construed as investment advice or recommendations for any purchase or sale of any specific security or commodity. Certain information contained herein is based on outside sources believed to be reliable, but its accuracy is not guaranteed.Any reference to a specific security, country or sector should not be construed as a recommendation to buy or sell investments in those securities, countries or sectors. Please note that portfolio holdings and positioning are subject to change without notice. The companies referenced may or may not represent securities purchased or sold for advisory clients. It should not be assumed that an investment in the companies discussed was or will be profitable. In Canada, NIMNA is availing itself of the International Adviser Exemption (IAE) in the following Provinces: Alberta, British Columbia, Manitoba and Ontario, including the foreign commodity trading advisor exemption in Ontario. The IAE is in compliance with National Instrument 31-103, Registration Requirements, Exemptions and Ongoing Registrant Obligations. MAR006373 Exp 07/2025.