Key Points

- Historical analysis indicates that when interest rates bottom following a rate-cutting cycle, the value index often experiences a greater percentage increase in 12-month forward earnings-per-share (EPS) estimates relative to the growth index.

- Value stocks generally outperform growth stocks in both rising and falling rate periods.

- The large-cap value universe typically contains companies with established earnings and robust cash flows, making them potentially more resilient in economic downturns.

- Value stocks tend to have lower valuations as they are less reliant on optimistic future growth expectations, providing a necessary buffer against market fluctuations.

The Federal Reserve’s (Fed’s) monetary policy has long been a force in shaping economic conditions and influencing financial markets. In addition to determining borrowing costs, the Fed’s interest-rate moves have historically had an impact on investment strategies and overall market performance. Over the last few years, the global pandemic, geopolitical tensions and supply-chain disruptions have also affected the investment backdrop, driving meaningful changes.

The Fed’s 50-basis-point rate cut in September had been a long-awaited and highly anticipated move, and rightfully so. Marking the first in four years, the rate cut was followed by a second cut of 25-basis points in November. These decisions, aimed at alleviating economic pressures, came amid an uncertain and volatile investment landscape. The first rate cut shifted market expectations, prompting investors to begin adjusting their portfolios to prepare for a potential ‘soft landing,’ in hopes that the Fed could circumvent a US recession. The second cut immediately followed the election of Donald Trump as the 47th US president. Post election, the 10-year Treasury rate has advanced, and market expectations for further aggressive cuts in interest rates have softened. In our view, if Trump’s policies prove to be inflationary, the bottoming of the rate-cutting cycle could come sooner than previously anticipated.

Where can investors turn for stability in this complex environment? We believe that strategically allocating capital to US large-cap, value-oriented stocks could be a compelling option.

History Can Rhyme

Our global research team employs a bottom-up, fundamentals-based research process. While our approach is largely centered on fundamentals, our research team also recognizes the importance of understanding how macroeconomic factors, such as interest-rate changes, can distinctly affect industry conditions.

In our view, history may not repeat itself to a tee, but it can sometimes rhyme. Thus, we thought it would be prudent to examine previous cycles of significant rate cuts, given the rate cuts projected between September 2024 and September 2025; in particular, we analyzed cycles when cuts in interest rates exceeded 200 basis points in a one-year period. Given that material cuts in interest rates over a relatively short period of time are usually associated with slowing economic growth (or the potential for it), we found that strategically allocating capital to US large-cap, value-oriented stocks could be beneficial for investors given their historical resilience, relatively more attractive valuations, and the potential for earnings downgrades.

High Growth Valuations Amid Economic Uncertainty

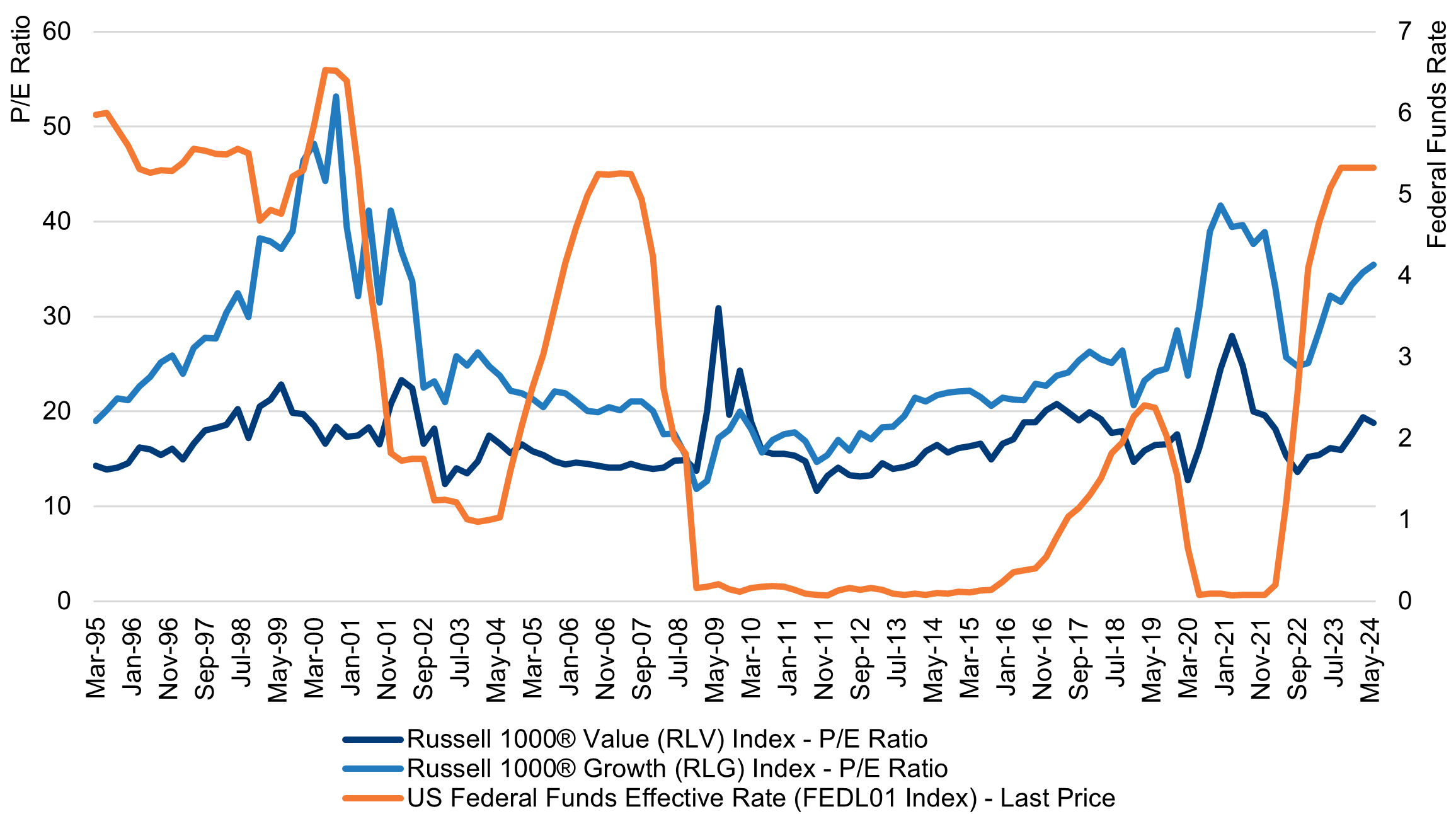

In our opinion, attempting to time the market using valuation data is a futile exercise. However, valuations can help analysts and portfolio managers better understand company-specific factors in a broader context. Investors are currently navigating a landscape marked by exceptionally elevated valuations, particularly within high-profile growth stocks such as the ‘magnificent seven,’ which have contributed substantially to recent market gains. This surge has caused average price-to-earnings (P/E) ratios to exceed historical norms, reminiscent of the dot-com bubble when many technology stocks were valued at P/E ratios of above 50 times earnings. These heightened valuations, which contrast with the largely steadier valuations of larger-cap value-oriented investments, could prompt the market to adjust its expectations. This may be an opportune time for investors to reassess their allocations and consider the benefits of increasing value exposure to balance an investment strategy.

Against this backdrop, growth investors may be overexposed to stocks that are trading at unsustainable levels and susceptible to multiple contractions. During the dot-com bubble, P/E ratios for the Russell 1000® Growth (RLG) Index reached over 50 times earnings. Current ratios sit at around 35 times earnings, which is still far above the RLG index’s long-term average of 21 times earnings. Following the bursting of the dot-com bubble, P/E valuations for the RLG index plummeted, as depicted in the chart below. With P/E ratios for the index climbing to similar levels today, we believe now is a good time for investors to consider some diversification within their equity allocations.

This may be an opportune time for investors to reassess their allocations and consider the benefits of increasing value exposure to balance an investment strategy.

Price-to-Earnings (P/E) Ratios Through Time

Source: Newton Investment Management, Bloomberg, as of June 28, 2024.

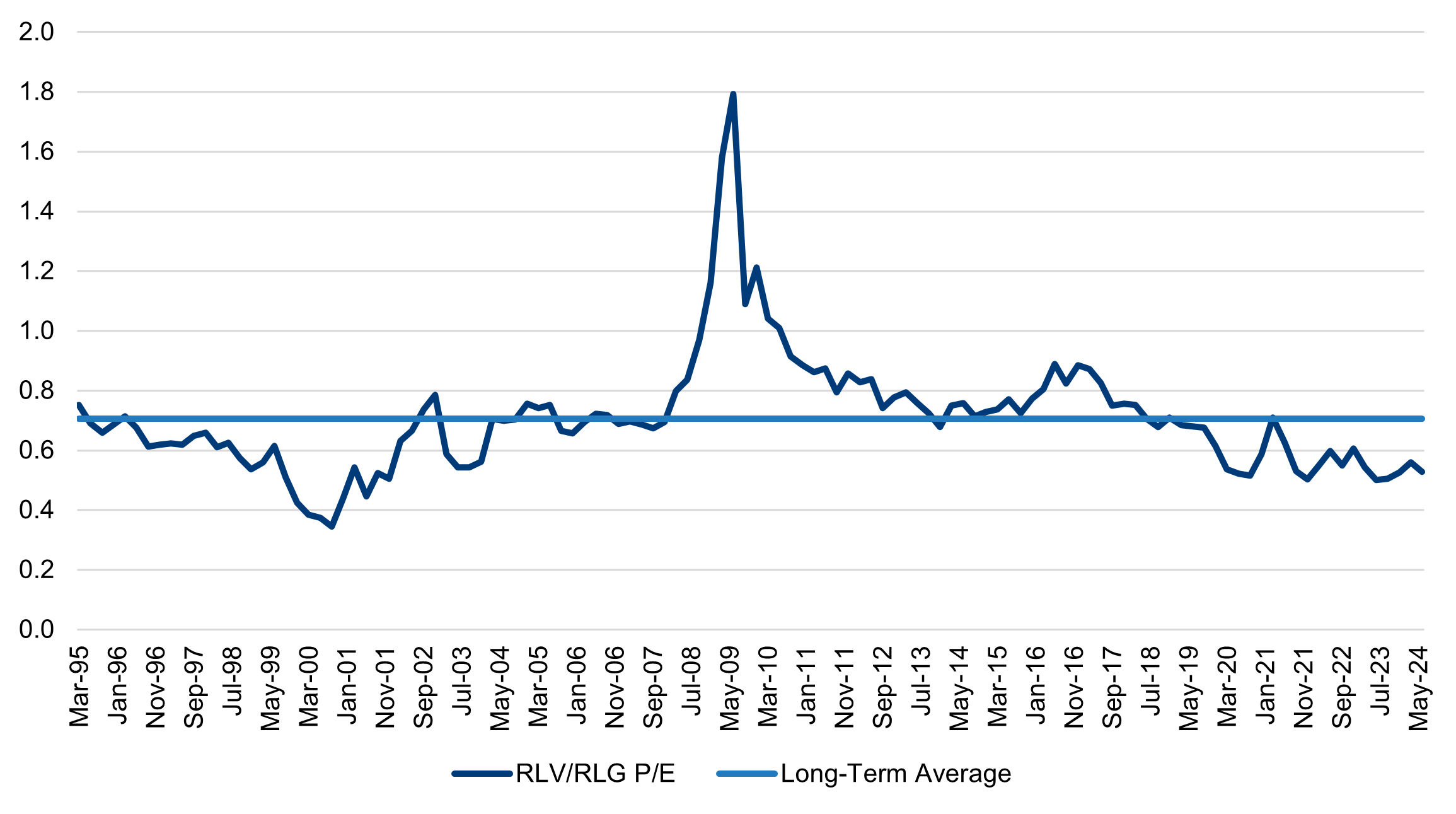

The Undervaluation of Value Stocks

The chart below shows the valuations of the Russell 1000® Value (RLV) Index relative to the RLG index over the last 30 years. Viewing these relative valuations throughout history highlights how undervalued value stocks are compared to growth stocks; currently, the discount sits at 0.53 versus the long-term average of 0.71. As market sentiment shifts, value stocks, and particularly those trading at low multiples, could see heightened interest from investors.

Premium/Discount for Price-to-Earnings (P/E) Ratio: Russell 1000® Value (RLV) Index Vs. Russell 1000® Growth (RLG) Index

Source: Newton Investment Management, Bloomberg, as of June 28, 2024.

Estimate Revisions

In our opinion, the graph below further supports a strategic shift to increased large-cap value exposure. Historical analysis indicates that when interest rates bottom following a rate-cutting cycle, the RLV index often experiences a greater percentage increase in 12-month forward earnings-per-share (EPS) estimates relative to the RLG index. Given the likelihood that Trump implements policies that prove to be inflationary, this trough in the rate-cutting cycle could come sooner than initially expected. Following the bottoming of interest rates in the aftermath of the 2008 global financial crisis, the RLV index saw an increase of 84% in 12-month forward EPS estimates, while the RLG index saw gains of 47%. Similarly, following the end of the rate-cutting cycle in 2020, the RLV index saw 12-month forward EPS estimate growth of 53%, while the RLG index saw growth of 37%.

12-Month Forward Earnings-Per-Share (EPS) Estimates

Source: Newton Investment Management, Bloomberg, as of June 28, 2024.

Continuing economic uncertainty exacerbates this risk of earnings revisions. Currently, US real gross-domestic-product (GDP) growth is expected to slow from above trend in 2024 to below trend in 2025; in addition, real income growth has softened, and the labor market is showing signs of cooling.1

The Resilience of Large-Cap Value

Amid the continuing uncertainty and shifting interest-rate dynamics, large-cap value stocks have consistently demonstrated their resilience across various market conditions. In analyzing performance of the cheapest 30% of US stocks versus the most expensive 30% of US stocks sorted by price-to-book ratio during previous rate cycles, research reveals an interesting dynamic: value stocks generally outperform growth stocks in both rising and falling rate periods. In nine out of the 11 periods of falling rates analyzed, value outperformed growth.2 This consistent outperformance supports our conviction in the enduring strength of US large-cap, value-oriented stocks. It also underscores the appeal of value stocks as a long-term investment strategy, especially given the unpredictability of the current environment.

The stability of value stocks offers several advantages in times of market volatility. The large-cap value universe typically contains companies with established earnings and robust cash flows, making them more resilient in economic downturns. Value stocks tend to have lower valuations as they are less reliant on optimistic future growth expectations, providing a necessary buffer against market fluctuations, as we mentioned in our previous blog post. Additionally, the Fed has embarked on what is expected to be a steady series of interest-rate cuts, and although this rate-cutting cycle could be shorter than initially expected, it makes the dividends offered by many value stocks more attractive, particularly in low interest-rate environments when investors seek steady income and growth over time in favor of fixed-income investments.

Positioning for Future Success

We believe that the current economic climate, marked by inflated growth-stock valuations, the potential for earnings revisions and the historical strength of large-cap value stocks, presents a compelling case for large-cap value investing. By strategically allocating to larger-cap, valued-oriented stocks, investors may find some stability and growth amid the uncertainty of the investment landscape.

Our approach, focused on finding value at the intersection of strong and improving fundamentals, attractive valuations and positive business momentum, positions us to benefit from these strengths as the landscape continues to evolve. We believe large-cap value investments allow us to capitalize on current market dynamics, while also providing a level of protection against inevitable fluctuations in the future environment. In our view, as markets continue to adjust to interest-rate changes and the potential for economic shifts, large-cap value stocks stand out as a pillar of resilience.

1 Economic Outlook US Q4 2024: Growth and Rates Start Shifting to Neutral, S&P Global, September 24, 2024, https://www.spglobal.com/ratings/en/research/articles/240924-economic-outlook-u-s-q4-2024-growth-and-rates-start-shifting-to-neutral-13258419

2 History Bodes Ill for Growth Stocks After Big Rally: Nir Kaissar, Bloomberg Opinion, January 2, 2024

Eric Brock, CEO of Ondas Holdings, joins Double Take to explore how drones have become essential to the global economy and how they are integrated into industries like agriculture, public safety, energy and entertainment.

Listen on

Key points

- Donald Trump’s new US administration is expected to focus on extending tax cuts, implementing pro-growth policies, deregulation, and taking a tougher stance on China.

- The election outcome has led to a rally in risk assets, and Trump’s policies are likely to be supportive of US equities in the short term.

- However, the potential for a wider fiscal deficit, in combination with higher tariffs and immigration restrictions, could challenge the current consensus on disinflation and have consequences for economic volatility.

Donald Trump has secured victory in his third US presidential bid, and with it the popular vote. This outcome reinforces the anti-incumbent trend seen across the world, with voters expressing their discontent on issues such as inflation, immigration, and lack of trust with public institutions. Trump will re-enter the White House in an evolving geopolitical landscape, as countries grapple with continuing conflicts in Eastern Europe and the Middle East, as well as tensions in Asia.

In the early days of Trump’s second term, his administration is likely to begin taking steps to extend tax cuts, deliver business-friendly, pro-growth policies and deregulation, and take a tougher stance on China. He is also likely to pursue executive orders on tighter immigration policy, energy policy, and higher trade tariffs.

As the election outcome became increasingly apparent, risk assets rallied while the US dollar strengthened. There has been a wide consensus view that a Trump victory will be positive for financial markets. However, there are several other key factors to consider when assessing the longer-term outlook, which we consider here.

A boost for US equities?

Trump’s Republican Party has won the Senate and looks very likely to take control of the House of Representatives, though several House races are yet to be called. A Republican sweep would allow Trump’s administration to get to work implementing its full policy platform. Front and centre are tax cuts and deregulation, both of which should benefit the profitability and competitiveness of US producers. This should be positive for US equities, both in absolute and in relative terms, as it should be supportive for the US dollar. Additionally, Trump has promised to use tariffs to support US producers.

While Trump has proposed to extend his 2017 tax cuts on individual incomes, to repeal the deduction cap on state and local taxes, and to cut corporate taxes, the ultimate make-up of the House will play a role in the size and scope of any tax bill. That said, all roads point to a bigger budget deficit, and the private sector will therefore need to absorb ever more US government debt. As has become increasingly clear, financial-market participants’ willingness to absorb that debt is considerably less when nominal GDP growth is high. Therein lies the irony: economic populism, whether implemented by Trump or Joe Biden, involves pro-cyclical fiscal policy. This approach increases nominal growth but, in turn, results in investors requiring a higher interest rate to lend money to the US government.

Inflation and interest-rate risks

In combination with higher tariffs and restrictions on immigration, higher deficits have the potential to generate a cyclical inflationary impulse. To be clear, the conditions necessary for a repeat of the inflation rates seen in 2021 and 2022 are not likely to stem from Trump’s policy agenda. However, a reacceleration of inflation would force a serious rethink of the now-consensus view that continued disinflation will track inflation back to the US Federal Reserve’s (Fed) target and thus allow for an extended easing cycle. We are not yet at the point at which investors are countenancing interest-rate hikes from the Fed, but it appears very much on the central bank’s agenda to price out the rate cuts that it had previously pencilled in for 2025 at its September summary of economic projections.

A reacceleration of inflation would force a serious rethink of the now-consensus view that continued disinflation will track inflation back to the US Federal Reserve’s target and thus allow for an extended easing cycle.

Additionally, investors would be likely to demand more of a yield pickup over short rates to take on interest-rate risk. As such, the new administration’s policy agenda, while likely to be positive for nominal growth over the short term, could increase the risk of further increases in interest rates and interest-rate volatility, both of which could have consequences for financial-market and economic volatility. In this context, it appears that the bond market is already beginning to reflect the Fed’s inability to ease policy as much as it has indicated it would like to, with government bond yields moving higher.

This time it’s different

It has been widely opined that a new Trump administration will benefit financial markets, based on historical performance following Trump’s first victory in 2016. However, while this may appear logical, the backdrop looks very different today.

Prior to Trump’s 2016 victory, global growth was slowing, evident in the commodity and emerging-market bust of 2014-15. Eighteen months of cross-market volatility had ensured that many market participants had deleveraged, leaving aggregate exposure to risk assets at historically depressed levels. Additionally, the then Fed Chair Janet Yellen had performed a dovish policy pivot in early 2016 which created the space for a broad, simultaneous easing of policy in the US, Europe and China. In turn, 2017 was the first period of synchronised global growth since the 2008 global financial crisis, and stocks soared.

We are currently several years into an economic cycle and market participants are heavily exposed to risk assets. Additionally, the growth outlook is not what it was in late 2016 following globally coordinated easing of monetary and fiscal policy.

Today, the regional outlook is increasingly divergent, and the imposition of higher tariffs by the US could mean lower growth elsewhere, particularly in China and Europe. China will probably respond with further policy announcements, and Europe is likely to ease monetary policy given fiscal constraints. We expect interest-rate differentials to diverge further as growth outside the US comes under further pressure.

Maintaining a long-term perspective

Overall, while the immediate investment implications of the US election result appear benign, it will be important to consider broader economic factors. The Trump administration’s pro-growth policies, including tax cuts and deregulation, could provide additional support for US equities. However, the potential for higher tariffs, immigration restrictions and increased deficits may lead to cyclical inflationary pressures. This could challenge the current consensus on disinflation and force a re-evaluation of the Fed’s easing cycle, potentially affecting economic stability over the longer term.

Against a complex backdrop, as investors also seek to navigate other challenges including heightened geopolitical tensions, it will be critical to remain vigilant and adaptable in seeking to identify the opportunities and avoid the risks.

Key Points

- Donald Trump’s new US administration is expected to focus on extending tax cuts, implementing pro-growth policies, deregulation, and taking a tougher stance on China.

- The election outcome has led to a rally in risk assets, and Trump’s policies are likely to be supportive of US equities in the short term.

- However, the potential for a wider fiscal deficit, in combination with higher tariffs and immigration restrictions, could challenge the current consensus on disinflation and have consequences for economic volatility.

Donald Trump has secured victory in his third US presidential bid, and with it the popular vote. This outcome reinforces the anti-incumbent trend seen across the world, with voters expressing their discontent on issues such as inflation, immigration, and lack of trust with public institutions. Trump will re-enter the White House in an evolving geopolitical landscape, as countries grapple with continuing conflicts in Eastern Europe and the Middle East, as well as tensions in Asia.

In the early days of Trump’s second term, his administration is likely to begin taking steps to extend tax cuts, deliver business-friendly, pro-growth policies and deregulation, and take a tougher stance on China. He is also likely to pursue executive orders on tighter immigration policy, energy policy, and higher trade tariffs.

As the election outcome became increasingly apparent, risk assets rallied while the US dollar strengthened. There has been a wide consensus view that a Trump victory will be positive for financial markets. However, there are several other key factors to consider when assessing the longer-term outlook, which we consider here.

A Boost for US Equities?

Trump’s Republican Party has won the Senate and looks very likely to take control of the House of Representatives, though several House races are yet to be called. A Republican sweep would allow Trump’s administration to get to work implementing its full policy platform. Front and center are tax cuts and deregulation, both of which should benefit the profitability and competitiveness of US producers. This should be positive for US equities, both in absolute and in relative terms, as it should be supportive for the US dollar. Additionally, Trump has promised to use tariffs to support US producers.

While Trump has proposed to extend his 2017 tax cuts on individual incomes, to repeal the deduction cap on state and local taxes, and to cut corporate taxes, the ultimate make-up of the House will play a role in the size and scope of any tax bill. That said, all roads point to a bigger budget deficit, and the private sector will therefore need to absorb ever more US government debt. As has become increasingly clear, financial-market participants’ willingness to absorb that debt is considerably less when nominal GDP growth is high. Therein lies the irony: economic populism, whether implemented by Trump or Joe Biden, involves pro-cyclical fiscal policy. This approach increases nominal growth but, in turn, results in investors requiring a higher interest rate to lend money to the US government.

Inflation and Interest-Rate Risks

In combination with higher tariffs and restrictions on immigration, higher deficits have the potential to generate a cyclical inflationary impulse. To be clear, the conditions necessary for a repeat of the inflation rates seen in 2021 and 2022 are not likely to stem from Trump’s policy agenda. However, a reacceleration of inflation would force a serious rethink of the now-consensus view that continued disinflation will track inflation back to the US Federal Reserve’s (Fed) target and thus allow for an extended easing cycle. We are not yet at the point at which investors are countenancing interest-rate hikes from the Fed, but it appears very much on the central bank’s agenda to price out the rate cuts that it had previously penciled in for 2025 at its September summary of economic projections.

A reacceleration of inflation would force a serious rethink of the now-consensus view that continued disinflation will track inflation back to the US Federal Reserve’s target and thus allow for an extended easing cycle.

Additionally, investors would be likely to demand more of a yield pickup over short rates to take on interest-rate risk. As such, the new administration’s policy agenda, while likely to be positive for nominal growth over the short term, could increase the risk of further increases in interest rates and interest-rate volatility, both of which could have consequences for financial-market and economic volatility. In this context, it appears that the bond market is already beginning to reflect the Fed’s inability to ease policy as much as it has indicated it would like to, with government bond yields moving higher.

This Time It’s Different

It has been widely opined that a new Trump administration will benefit financial markets, based on historical performance following Trump’s first victory in 2016. However, while this may appear logical, the backdrop looks very different today.

Prior to Trump’s 2016 victory, global growth was slowing, evident in the commodity and emerging-market bust of 2014-15. Eighteen months of cross-market volatility had ensured that many market participants had deleveraged, leaving aggregate exposure to risk assets at historically depressed levels. Additionally, the then Fed Chair Janet Yellen had performed a dovish policy pivot in early 2016 which created the space for a broad, simultaneous easing of policy in the US, Europe and China. In turn, 2017 was the first period of synchronized global growth since the 2008 global financial crisis, and stocks soared.

We are currently several years into an economic cycle and market participants are heavily exposed to risk assets. Additionally, the growth outlook is not what it was in late 2016 following globally coordinated easing of monetary and fiscal policy.

Today, the regional outlook is increasingly divergent, and the imposition of higher tariffs by the US could mean lower growth elsewhere, particularly in China and Europe. China will probably respond with further policy announcements, and Europe is likely to ease monetary policy given fiscal constraints. We expect interest-rate differentials to diverge further as growth outside the US comes under further pressure.

Maintaining a Long-Term Perspective

Overall, while the immediate investment implications of the US election result appear benign, it will be important to consider broader economic factors. The Trump administration’s pro-growth policies, including tax cuts and deregulation, could provide additional support for US equities. However, the potential for higher tariffs, immigration restrictions and increased deficits may lead to cyclical inflationary pressures. This could challenge the current consensus on disinflation and force a re-evaluation of the Fed’s easing cycle, potentially affecting economic stability over the longer term.

Against a complex backdrop, as investors also seek to navigate other challenges including heightened geopolitical tensions, it will be critical to remain vigilant and adaptable in seeking to identify the opportunities and avoid the risks.

Key points

- Donald Trump’s new US administration is expected to focus on extending tax cuts, implementing pro-growth policies, deregulation, and taking a tougher stance on China.

- The election outcome has led to a rally in risk assets, and Trump’s policies are likely to be supportive of US equities in the short term.

- However, the potential for a wider fiscal deficit, in combination with higher tariffs and immigration restrictions, could challenge the current consensus on disinflation and have consequences for economic volatility.

Donald Trump has secured victory in his third US presidential bid, and with it the popular vote. This outcome reinforces the anti-incumbent trend seen across the world, with voters expressing their discontent on issues such as inflation, immigration, and lack of trust with public institutions. Trump will re-enter the White House in an evolving geopolitical landscape, as countries grapple with continuing conflicts in Eastern Europe and the Middle East, as well as tensions in Asia.

In the early days of Trump’s second term, his administration is likely to begin taking steps to extend tax cuts, deliver business-friendly, pro-growth policies and deregulation, and take a tougher stance on China. He is also likely to pursue executive orders on tighter immigration policy, energy policy, and higher trade tariffs.

As the election outcome became increasingly apparent, risk assets rallied while the US dollar strengthened. There has been a wide consensus view that a Trump victory will be positive for financial markets. However, there are several other key factors to consider when assessing the longer-term outlook, which we consider here.

A boost for US equities?

Trump’s Republican Party has won the Senate and looks very likely to take control of the House of Representatives, though several House races are yet to be called. A Republican sweep would allow Trump’s administration to get to work implementing its full policy platform. Front and centre are tax cuts and deregulation, both of which should benefit the profitability and competitiveness of US producers. This should be positive for US equities, both in absolute and in relative terms, as it should be supportive for the US dollar. Additionally, Trump has promised to use tariffs to support US producers.

While Trump has proposed to extend his 2017 tax cuts on individual incomes, to repeal the deduction cap on state and local taxes, and to cut corporate taxes, the ultimate make-up of the House will play a role in the size and scope of any tax bill. That said, all roads point to a bigger budget deficit, and the private sector will therefore need to absorb ever more US government debt. As has become increasingly clear, financial-market participants’ willingness to absorb that debt is considerably less when nominal GDP growth is high. Therein lies the irony: economic populism, whether implemented by Trump or Joe Biden, involves pro-cyclical fiscal policy. This approach increases nominal growth but, in turn, results in investors requiring a higher interest rate to lend money to the US government.

Inflation and interest-rate risks

In combination with higher tariffs and restrictions on immigration, higher deficits have the potential to generate a cyclical inflationary impulse. To be clear, the conditions necessary for a repeat of the inflation rates seen in 2021 and 2022 are not likely to stem from Trump’s policy agenda. However, a reacceleration of inflation would force a serious rethink of the now-consensus view that continued disinflation will track inflation back to the US Federal Reserve’s (Fed) target and thus allow for an extended easing cycle. We are not yet at the point at which investors are countenancing interest-rate hikes from the Fed, but it appears very much on the central bank’s agenda to price out the rate cuts that it had previously pencilled in for 2025 at its September summary of economic projections.

A reacceleration of inflation would force a serious rethink of the now-consensus view that continued disinflation will track inflation back to the US Federal Reserve’s target and thus allow for an extended easing cycle.

Additionally, investors would be likely to demand more of a yield pickup over short rates to take on interest-rate risk. As such, the new administration’s policy agenda, while likely to be positive for nominal growth over the short term, could increase the risk of further increases in interest rates and interest-rate volatility, both of which could have consequences for financial-market and economic volatility. In this context, it appears that the bond market is already beginning to reflect the Fed’s inability to ease policy as much as it has indicated it would like to, with government bond yields moving higher.

This time it’s different

It has been widely opined that a new Trump administration will benefit financial markets, based on historical performance following Trump’s first victory in 2016. However, while this may appear logical, the backdrop looks very different today.

Prior to Trump’s 2016 victory, global growth was slowing, evident in the commodity and emerging-market bust of 2014-15. Eighteen months of cross-market volatility had ensured that many market participants had deleveraged, leaving aggregate exposure to risk assets at historically depressed levels. Additionally, the then Fed Chair Janet Yellen had performed a dovish policy pivot in early 2016 which created the space for a broad, simultaneous easing of policy in the US, Europe and China. In turn, 2017 was the first period of synchronised global growth since the 2008 global financial crisis, and stocks soared.

We are currently several years into an economic cycle and market participants are heavily exposed to risk assets. Additionally, the growth outlook is not what it was in late 2016 following globally coordinated easing of monetary and fiscal policy.

Today, the regional outlook is increasingly divergent, and the imposition of higher tariffs by the US could mean lower growth elsewhere, particularly in China and Europe. China will probably respond with further policy announcements, and Europe is likely to ease monetary policy given fiscal constraints. We expect interest-rate differentials to diverge further as growth outside the US comes under further pressure.

Maintaining a long-term perspective

Overall, while the immediate investment implications of the US election result appear benign, it will be important to consider broader economic factors. The Trump administration’s pro-growth policies, including tax cuts and deregulation, could provide additional support for US equities. However, the potential for higher tariffs, immigration restrictions and increased deficits may lead to cyclical inflationary pressures. This could challenge the current consensus on disinflation and force a re-evaluation of the Fed’s easing cycle, potentially affecting economic stability over the longer term.

Against a complex backdrop, as investors also seek to navigate other challenges including heightened geopolitical tensions, it will be critical to remain vigilant and adaptable in seeking to identify the opportunities and avoid the risks.

Key Points

- In our view, normalization in the macroeconomic environment should lead to normalization in relative performance between growth and value stocks.

- Even in periods of multiple contraction for expensive stocks, multiples for cheap stocks have remained relatively flat, suggesting a certain degree of downside protection.

- Allocating to value could offer investors diversification and help minimize the impact of a market drawdown while also participating in the market’s upside.

When should I start to buy value stocks? As value investors, this is one of the most frequently asked questions we have received thus far in 2024, and our reply has remained consistent—always.

Earlier this year, the question was usually raised in the context of the robust market leadership of large-cap growth stocks, which saw share prices and valuations pushed to levels reminiscent of the late 1990s tech bubble. More recently, since the start of the third quarter, markets saw an abrupt reversal in the relative performance of growth versus value, akin to 2022, when the Russell 1000® Value index substantially outpaced the S&P 500® and Russell 1000® Growth indices.

Money in Motion

For a more constructive response to the question above, we would need to identify catalysts that could unseat growth and shift market leadership. A question to consider might be, “What prompts money in motion?” Historically, this has been achieved through macroeconomic data and monetary policy, major geopolitical events, a global financial crisis and a global pandemic, among other phenomena.

Everyday financial metrics such as company valuations rarely effect market-leadership changes. In our view, valuation is a poor market-timing tool—expensive stocks can stay expensive, or get more expensive, and cheap stocks can stay cheap, or get cheaper. In a ‘Goldilocks’ environment, valuations tend to take a back seat to exuberance and matter less, until they matter more.

Hindsight Is 20/20

In our experience, one of the most effective ways to spot a market turn is through hindsight. For this reason, we believe that rebalancing is imperative and that allocating to value stocks is practical in all market environments. As you may have already gathered, we are not proponents of market timing. We are quick to acknowledge that we do not have an edge on the macroeconomic environment or on the types of catalysts mentioned above.

We focus more on microeconomic factors, including fundamental company research, to inform the macroeconomic views that flow into our investment and portfolio-construction decision-making. We embrace skepticism and concentrate on durable change on the margin. For instance, if a company tells us that its costs have been incrementally rising, and we discover that its peers are echoing a similar sentiment, we can infer that costs are climbing for a broader swatch of companies and consumers. This approach gives us a direct read into inflation trends occurring throughout the broader economy. While perhaps backward looking, we believe these direct observations can serve as better indicators than the retroactive, key economic data preferred by the Federal Reserve (Fed). Fed Chair Jerome Powell’s “transitory” inflation remarks back in 2021, which did not pan out as expected, are a case in point.

In our experience, one of the most effective ways to spot a market turn is through hindsight. For this reason, we believe that rebalancing is imperative and that allocating to value stocks is practical in all market environments.

If our team lacks an edge, or the will to time the market, then why do we believe that the time is always right to buy value? In our view, the following reasons support our case.

1. We believe that normalization in the macroeconomic environment should lead to normalization in stock-market performance.

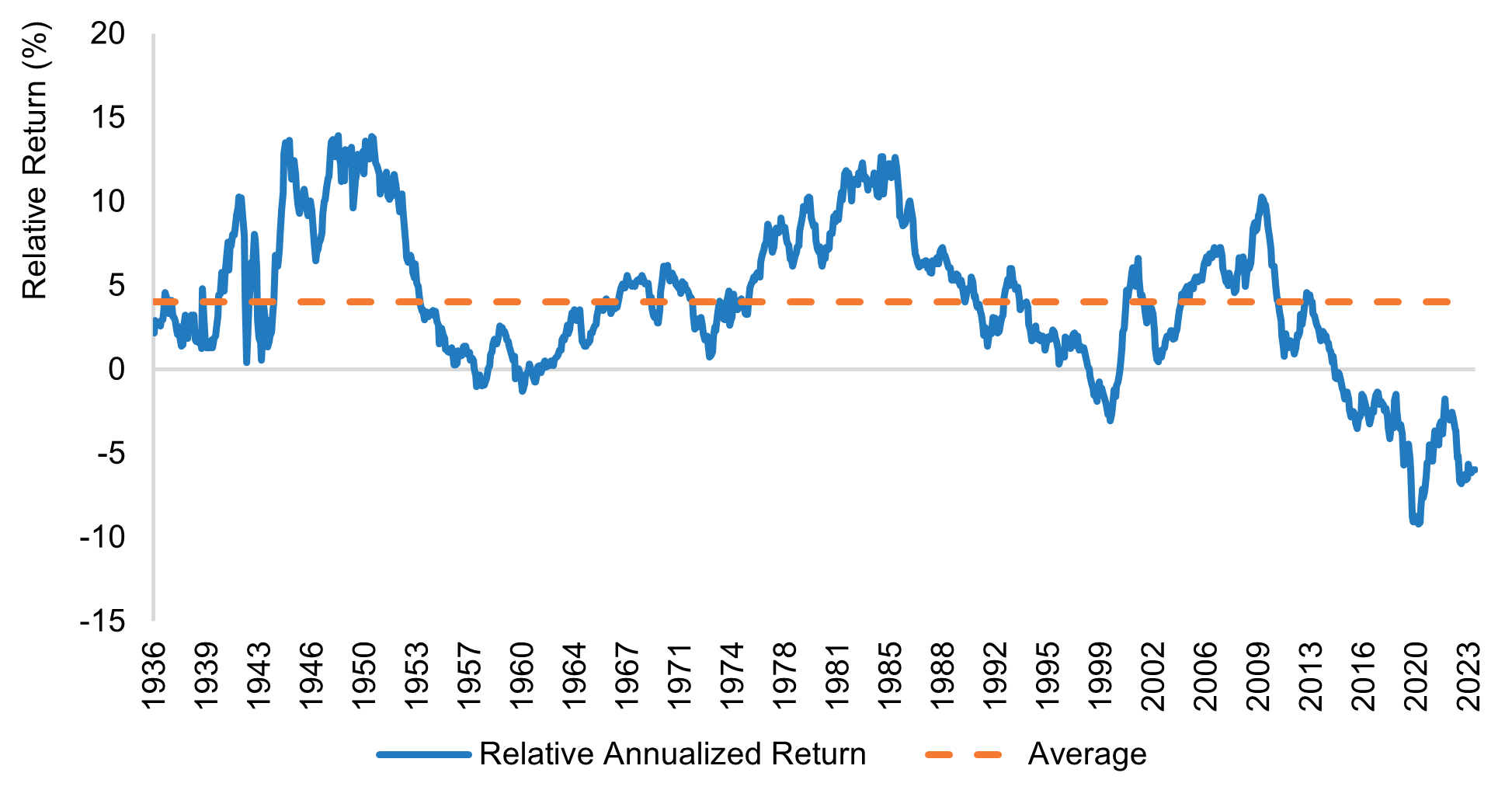

First, we believe that mean reversion theory, also known as reversion to the mean, should play out as the macroeconomic environment normalizes. Over the last 90 years, value has outperformed growth on a rolling 10-year basis by roughly 400 basis points, as depicted by the dotted orange line in the chart below. Within this time frame, we have seen multiple market cycles, recessions, soft patches, booming economies, bull markets, bear markets, etc., arise. Notably, in the last 15 years, growth materially outpaced value. In our view, the robust performance of growth stocks over that period was largely driven by extremely accommodative monetary policy and quantitative easing—in other words, free money—put in place following the global financial crisis to stabilize the financial system and the global economy.

As the macroeconomic environment has begun to normalize to pre-global financial crisis levels, monetary policy has become more restrictive and quantitative easing has been replaced with quantitative tightening. Namely, the era of free money has come to an end. We believe this development could be a catalyst that brings the relative performance of value versus growth closer to historical averages, though this may take some time to materialize.

Relative Return of Value to Growth

For illustrative purposes only. Source: Newton Investment Management and Alliance Bernstein, as of May 31, 2024. Blue line represents Value/Growth 10-Year Rolling Relative Return. This is a “relative” chart of Growth and Value; the indices used are proprietary to Alliance Bernstein. Value is defined as the lowest quintile of price-to-book (P/B) ratio, while Growth is defined as the highest quintile of P/B ratio.

We do not expect value to outperform growth at levels seen in 2009, the mid 1980s, or the late 1940s and early 1950s. However, we do believe that as the macroeconomic environment normalizes, so should relative performance.

2. “Expensive” stock prices are getting more expensive.

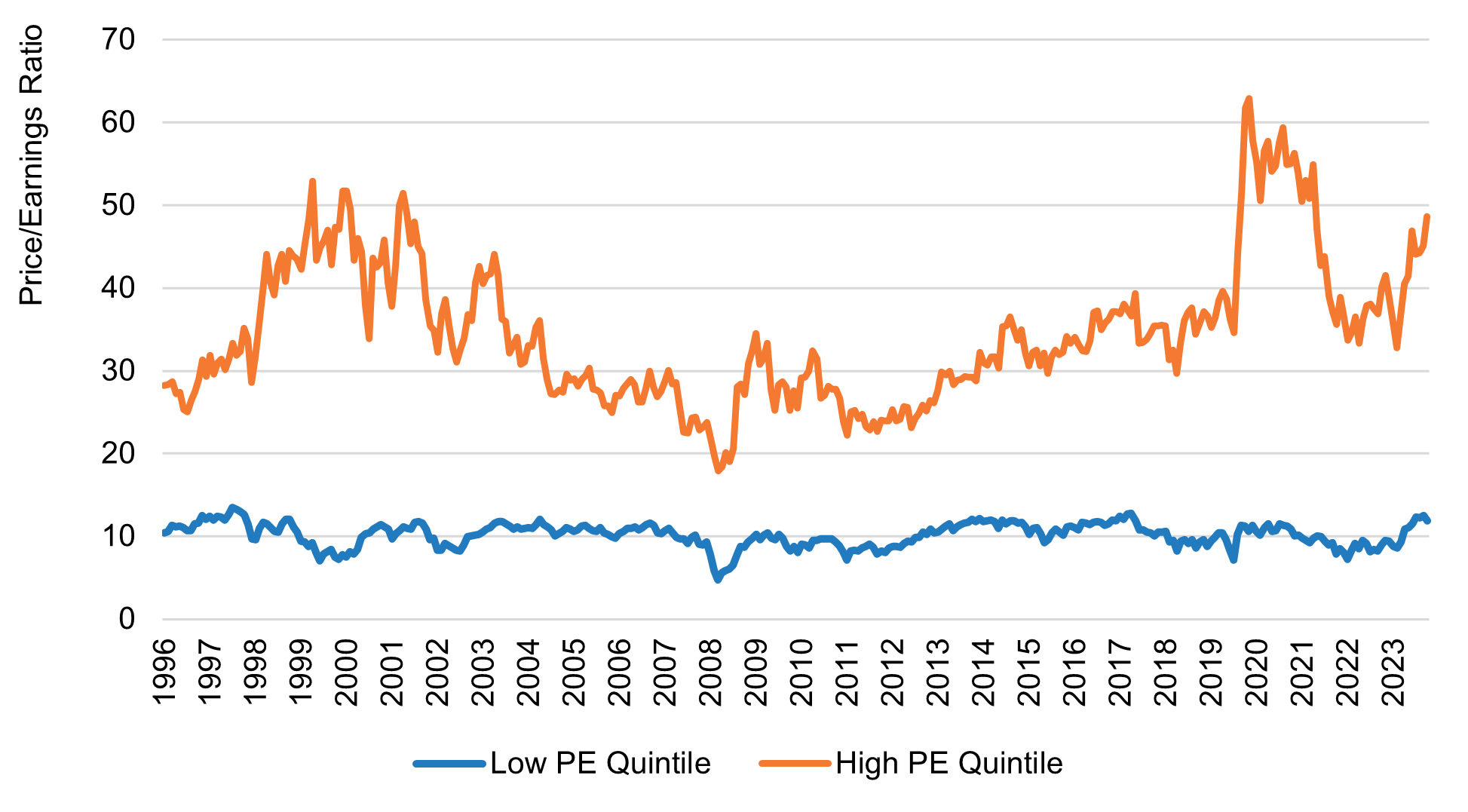

Another reason we believe investors should allocate to value is because value stocks can bring balance to a portfolio. Value stocks are relatively less expensive than growth stocks, with lower price-to-earnings (P/E) ratios; yet they are still solid investments. A P/E ratio can be a useful barometer for determining what factors the market is pricing into a company’s stock price from an earnings-power perspective. Value stocks are often considered cheap, while growth stocks are typically pricier, as investors tend to bid up prices of growth stocks to get ahead of their greater earnings-growth prospects.

The chart below shows the gap between the most expensive and least expensive quintiles of stocks in the S&P 500®, as measured by their P/E ratios. As the chart illustrates, there have been periods in time when expensive stocks have become more expensive relative to both cheap stocks and their own history. For instance, expensive stocks have recently begun to approach highs akin to the 1990s dot-com bubble, largely driven by investor exuberance around the ‘magnificent seven’ group of large-cap growth tech stocks and the disruptive potential of artificial intelligence. However, it is important to note that when expensive stocks have skyrocketed historically, they often later experienced multiple contractions (i.e., lower P/E levels), as waning enthusiasm caused share prices to retreat.

Expensive Stocks Are Looking Expensive

Source: Newton Investment Management, FactSet, as of June 30, 2024.

The remarkable consistency of cheap stocks over the same period is also noteworthy. While cheap stocks look cheap relative to pricier stocks, they also continue to look cheap relative to their own history. Even in periods of multiple contraction for expensive stocks, multiples for cheap stocks have remained relatively flat, suggesting a certain degree of downside protection.

3. Growth and value investing is not a zero-sum game.

We also believe that allocating to value makes sense due to the changing dynamics of the risk-reward ratio between growth and value since the Covid-19 pandemic. In the ten years leading up to the pandemic, growth was the clear market leader, as accommodative monetary policy and the Fed put gave investors the confidence to ‘buy the dip’ during periods of market volatility. As the table below shows, growth delivered an impressive 15.2% annualized return while experiencing relatively mild average drawdowns of 7.6%. Based on our conversations with investors and clients, the consensus view was that value performance during this time was flat at best and negative at worst. Yet, over the same period, value delivered an annualized return of 11.8%, a respectable absolute return in our view. However, we do understand the sentiment, as value lagged growth by over 300 basis points on a relative basis.

Since the pandemic, and the shift in both the macroeconomic environment and monetary policy, value has closed the gap. While growth has still outperformed, the margin has been cut in half. More notable, perhaps, are the drawdown statistics; over this period, the average drawdown for value is nearly 400 basis points less than that of growth. Circling back to our previous remarks on the multiple-contraction potential of expensive growth stocks, we see that allocating to value could offer investors some diversification and help minimize the impact of a market drawdown on a portfolio while still participating in the market’s upside.

Source: Newton Investment Management and Morningstar, as of August 31, 2024.

A Balanced Approach

Since the beginning of this year, we have advocated for taking a balanced approach to investing. This was predicated on the rising uncertainty around several macroeconomic factors including economic growth, inflation and monetary policy, all of which could bring heightened volatility to markets and investor returns. We believe the same logic applies when constructing holistic investment portfolios, favoring a reasonable balance between growth and value stocks, particularly against the current backdrop of rising valuations and concentration risk among growth indices and benchmarks.

Identifying Idiosyncratic Opportunities

From a value-investing perspective, we refer to “balance” as accounting for and neutralizing macroeconomic risk, while relying on our investment process to identify compelling idiosyncratic opportunities. We continue to lean on our strengths and strive to be good stock pickers, while minimizing unintended and uncompensated risks.

Pulling back from the immediate term, we continue to believe that companies and investors alike are adjusting to the normalization of both inflation and interest rates in the US, not to pre-Covid levels but to pre-global financial crisis levels. In our view, inflation is likely to be higher and more persistent than it was in the 12 years leading up to the pandemic, and as a result, the Fed may keep interest rates elevated. While inflation has moderated from peak levels and is headed in the right direction, and while monetary policy is likely to follow, we firmly believe that the days of benign inflation and free money are behind us. In the future, we believe that fundamentals, valuations, and the ability to generate in-house liquidity via solid free cash flow should play a larger role in separating the winners from the losers. As always, we favor companies sitting at the nexus of strong and improving fundamentals, attractive valuations and catalyst-driven business momentum.

Key Points

- Small-cap stocks may be well positioned to benefit from Federal Reserve (Fed) interest-rate cuts, as higher rates have challenged the asset class’s profitability and caused them to significantly lag their larger-cap counterparts.

- Initial public offerings (IPOs) are on the upswing; through the first half of 2024, 94 companies have gone public with $18.5 billion in capital raised, an 80% increase from the proceeds raised in the first half of 2023. Based on this data, the total number of IPOs in 2024 is projected to be 188 on an annualized basis, an improvement over 2022 and 2023 but still below the 254-per-year average of the last 20 years.1

- Despite challenges such as high interest rates, global economic shifts, employment trends and the upcoming US presidential election, US capital markets remain among the most robust worldwide. In our view, rate cuts and a stable, albeit slower-growing, economy following the election could support a further rebound in IPO activity in 2025.

In recent years, small-cap stocks have underperformed their larger-cap counterparts. Likewise, the initial public offering (IPO) market, which feeds fresh companies into the small-cap segment more than any other segment of the equity market, has been lackluster. Despite their lag in performance, small caps have always played an important role in portfolio diversification, providing investors with exposure to smaller but faster-growing companies with greater ties to the local economies in which they operate. Small-cap stocks are key to achieving proper diversification, particularly when paired with investments in larger, often slower-growing, multinational companies. Like large caps, small caps provide diversified exposure to equity markets, and, in our view, the relatively lower correlation between the two market-cap segments, historically, underscores the diversifying benefits of small caps.

Yet, over the last two decades as economic shifts have continued to reshape the financial landscape, small caps have largely been overlooked. In our view, this underdog scenario could present a compelling opportunity for investors, particularly in the new environment. The state of valuation discrepancies, monetary policies, interest rates and IPO activity all have implications for the small-cap market. As ongoing developments in the global economy continue to transform market dynamics, we believe that small caps are poised to benefit, with growing potential to capitalize on evolving opportunities.

As of July 10, we may have hit the start of an inflection between large and small caps. Is this a true pivot, or an anomaly? That is the question at hand. Nevertheless, in our view, the extended weakness in small caps, which is now in its 14th year by some estimates, is due for a correction.

Improving Market Conditions

We believe that multiple market conditions have aligned in a way that should favor small-cap stocks for the foreseeable future, especially given economic shifts that have ensued post pandemic. With the reopening of economies across the globe, and the resulting distortion in supply-demand dynamics, large-cap stocks have far outpaced their small-cap counterparts in valuation growth, leading to a disparity not seen since the dot-com bubble of the late 1990s. Interestingly, the technology sector has significantly contributed to the more recent upward trajectory of large-cap valuations, highlighting the skewed valuation dynamics across the broader market.

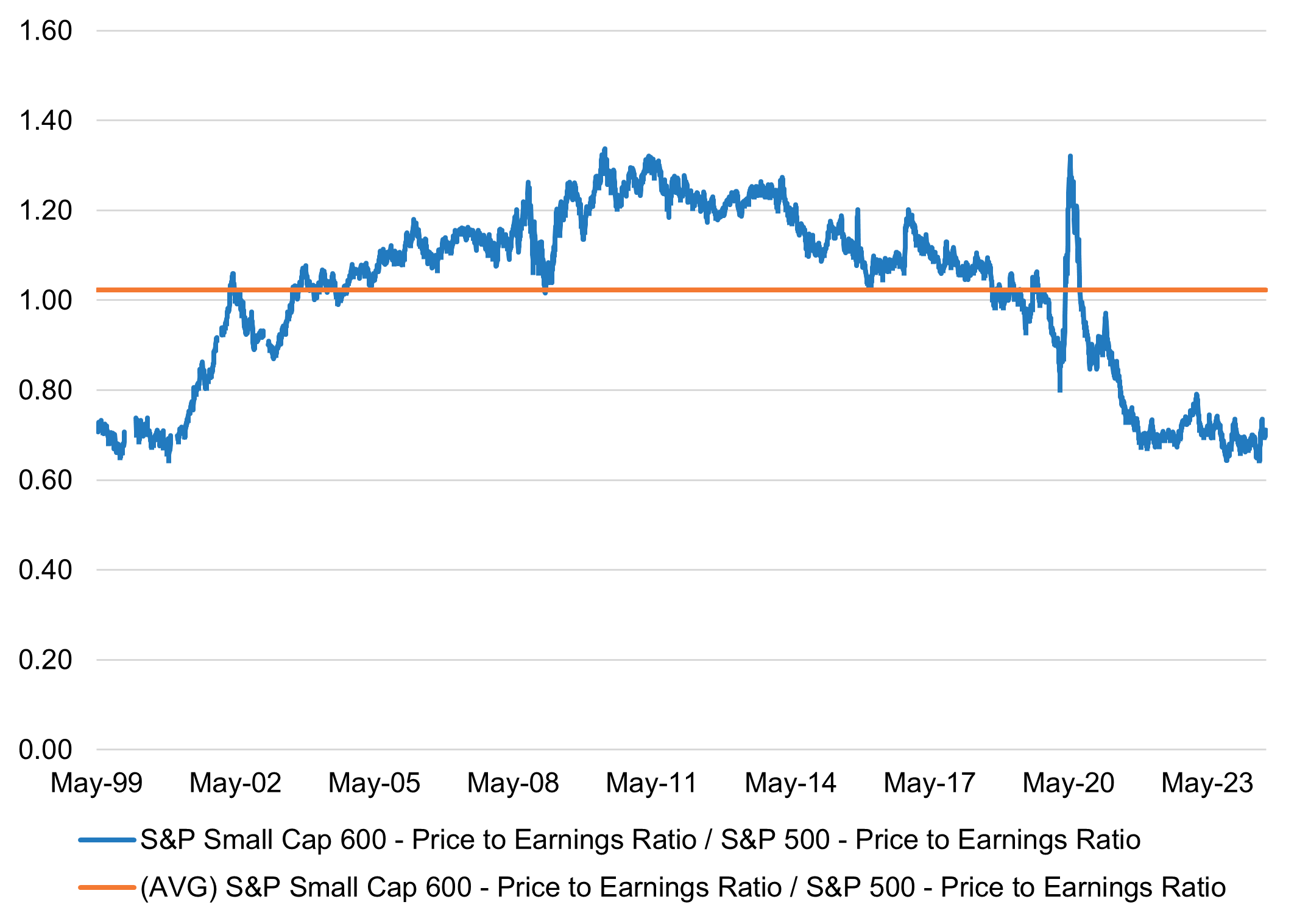

As the graph below illustrates, the current price-to-earnings (P/E) multiple discount of the S&P SmallCap 600® relative to the S&P 500® stands at around 0.71, compared to the long-term average of 1.02, which indicates that small caps are likely to be undervalued.

Forward Price to Earnings Premium/Discount (S&P 600 vs. S&P 500)

Source: FactSet. As of August 29, 2024.

This valuation gap presents an opportunity for small caps to potentially generate higher returns, as market forces attempt to correct this imbalance. At Newton, our dedicated small-cap analysts strive to consistently identify promising stocks that are often overlooked by the broader market to capitalize on these conditions. Despite the earnings-growth deceleration across small-cap companies in 2023, which was partially attributable to rising interest rates, we believe the combination of historically low valuations and potential for upward earnings revisions creates a more constructive investment environment for small-cap stocks. While small caps typically exhibit greater volatility, they also offer significant growth potential compared to their more established large-cap counterparts. This growth potential becomes especially attractive during market corrections, when undervalued small-cap companies can deliver substantial returns as valuations adjust.

At Newton, our dedicated small-cap analysts strive to consistently identify promising stocks that are often overlooked by the broader market to capitalize on these conditions.

Valuation Discrepancies: Public Versus Private Markets

Another notable valuation disparity exists between public and private markets. In recent years, private markets have witnessed a surge in both the number and value of deals transacted. This was especially true in 2021, when many private companies were accepting inflated valuations to emulate soaring public-market valuations. However, while public-market valuations have retreated from peak levels in recent years, private-company valuations have held relatively steady.

This divergence has created a challenging environment for dealmaking in the venture-capital world. Bid-ask spreads have widened, as management teams resist lowering valuations and investors sidestep inflated prices. Deal activity has slowed, and as a result conditions for limited partners have tightened. This scarcity of capital has particularly affected late-stage private companies, contributing to the growing backlog of companies waiting to go public; consequently, the IPO market has remained subdued. In our view, this backlog could potentially spawn considerable investment opportunities once market conditions become more favorable.

IPO Market Activity

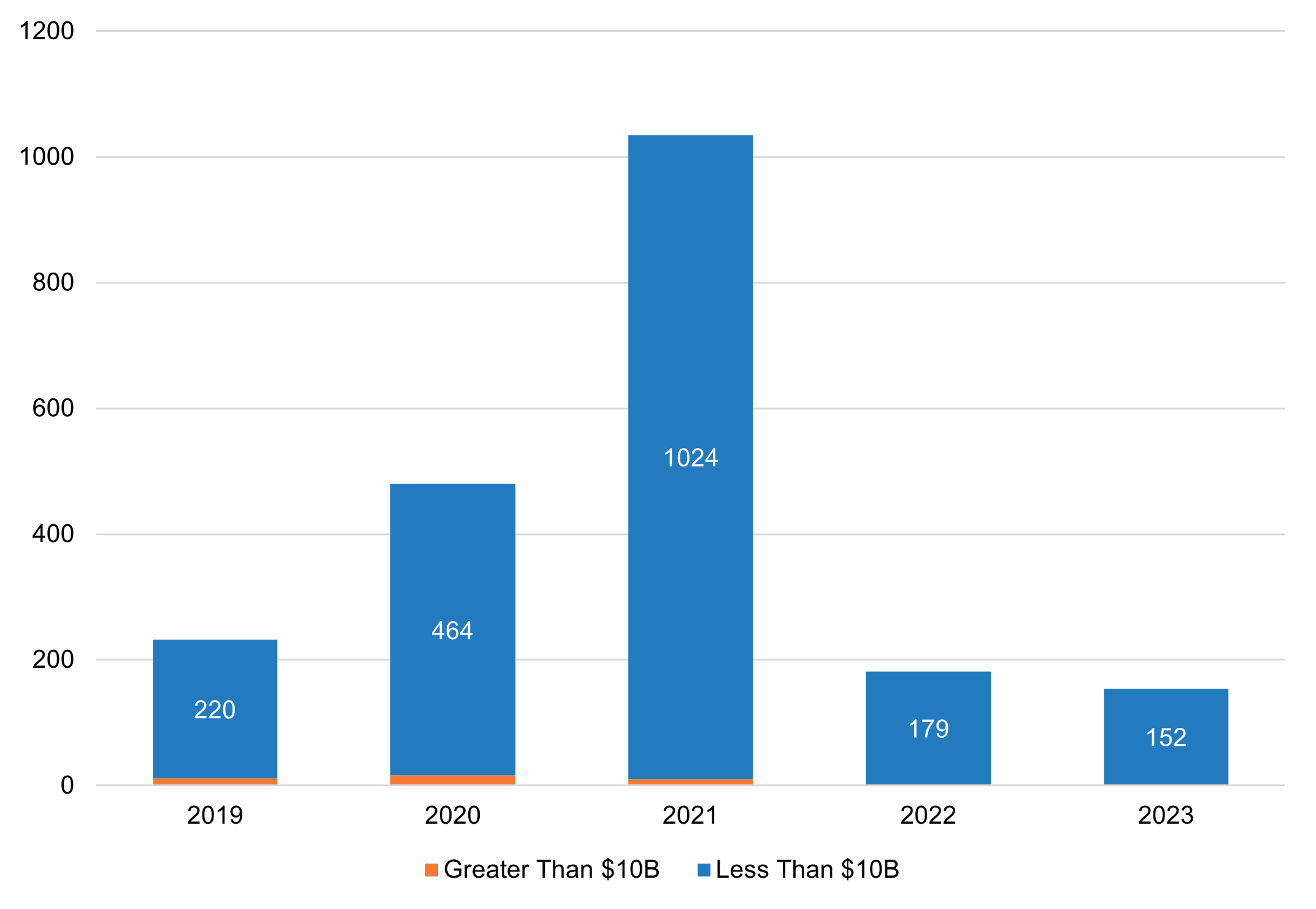

Over the last decade—with the exception of the 2021 boom in special purpose acquisition companies—the IPO market has been rather anemic. Many investors believe that IPOs tend to churn out new public companies at larger-cap valuations; on the contrary, IPOs are much more likely to feed directly into the small-cap market. As reflected in the chart below, which depicts the last five years of IPO activity by market cap, the majority of IPOs roll out at valuations of less than $10 billion.

Number of IPOs Last Five Years by Large Cap (>$10B) and Small-Mid Cap (<$10B)

Source: Stock Analysis, IPO Statistics. Data as of December 31, 2023.

Small Caps and IPOs

The relationship between the IPO market and small caps has always been symbiotic. Small-cap companies, which provide heavily idiosyncratic opportunities, are often relatively unknown to investors due to the lack of coverage by Wall Street. Street analysts are not just choosing to ignore small caps; there are simply too many companies to cover, particularly as research budgets have grown tighter over time.

The IPO market, which takes companies from being privately held to the public market, is an important feeder to the small-cap space. Despite pre-IPO roadshows and fanfare, public investors generally lack deeper knowledge into these companies, which often carry a heightened set of both risks and opportunities. Due to this lack of readily available information, small caps have typically represented one of the most fertile market segments for alpha generation across public equities.

A Brighter Outlook for IPOs

The IPO market is slowly showing signs of recovery, with a growing backlog of companies preparing to make their public debuts. Anticipated improvements in conditions surrounding inflation and interest rates are supporting the 2024 IPO outlook for the remainder of the year, though the US presential election and continuing geopolitical tensions could pose challenges. As market valuations normalize and bid-ask spreads narrow, the IPO market is expected to regain momentum either later this year or in early 2025. Historically, small caps have dominated the number of IPOs, suggesting that the resurgence of the IPO activity may introduce a new wave of small-cap companies into the market.

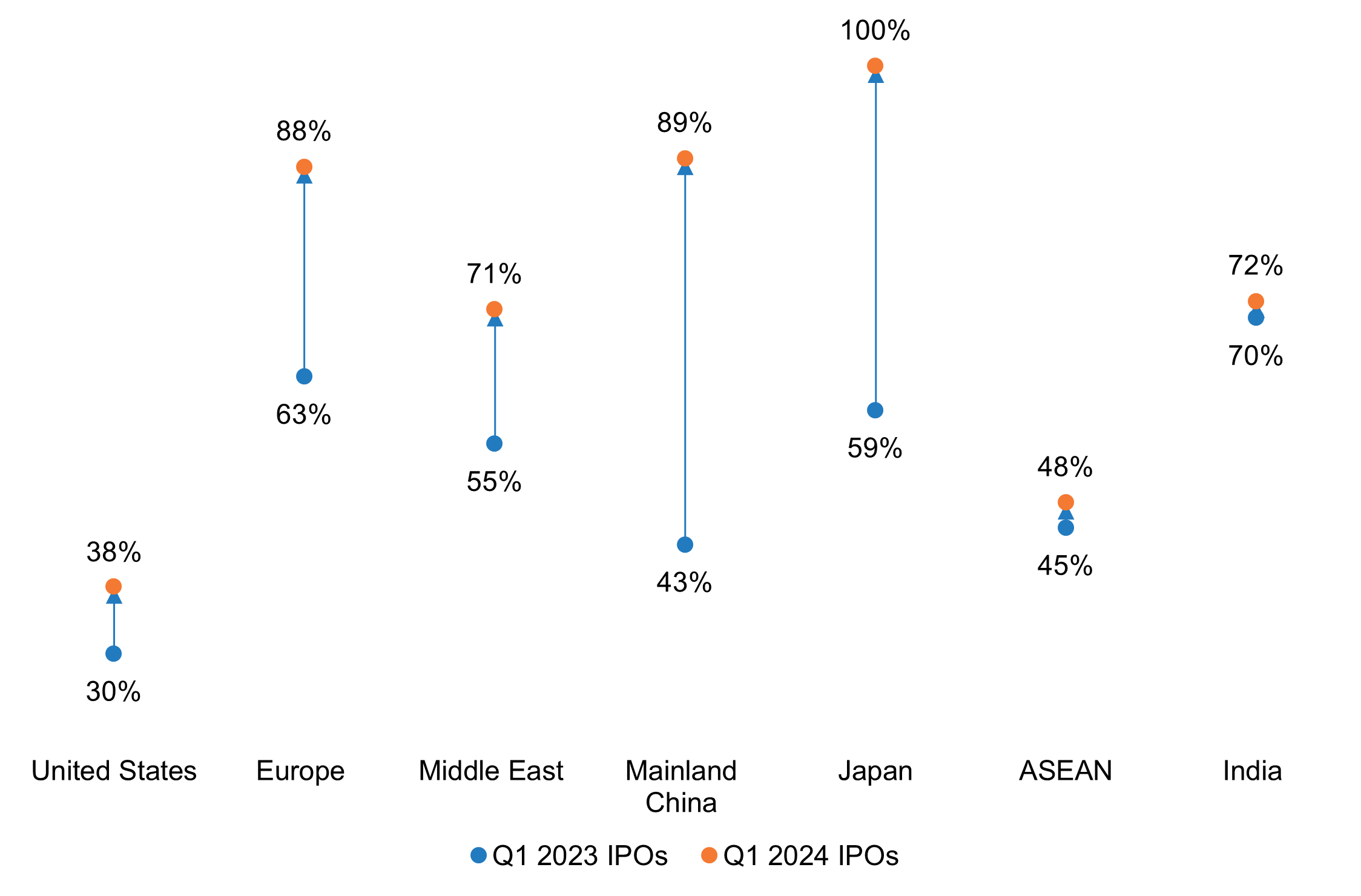

We believe a robust IPO market would benefit investors focused on small-caps stocks, providing access to a range of new companies with solid growth potential. The positive performance of recent IPOs, many of which have seen their stock prices exceed their offer prices (as depicted in the chart below), points to improving market valuations and investor sentiment toward riskier opportunities. A resurgence in the IPO market would also provide small-cap investors with enhanced liquidity, making it easier to buy and sell small-cap stocks, and thus leading to more efficient pricing in the market.

After-Market Performance by Region

Percentage of Current Share Price Above Offer Price

Data source: EY. As of March 27, 2024.

Interest Rates and Monetary Policy

Investor attention is currently focused on interest rates, with the Federal Reserve (Fed) announcing its decision to lower interest rates by half a percentage point on September 18, 2024. We believe small caps stand to benefit from a reduction in rates, as the decline in borrowing costs should offer greater relief to these companies that rely more heavily on external capital for funding their growth, expansion and innovation. Small-cap companies tend to be more exposed to higher interest rates, as they typically have higher leverage and more floating-rate debt than large caps.

Additionally, equities are usually more appealing to investors relative to fixed-income investments during periods of lower interest rates. Reduced interest rates help promote business expansion and assist in enhancing profitability for small-cap companies, making them a potentially attractive growth opportunity. Reduced borrowing costs could allow these companies to invest in new projects and expand operations more accessibly.

A Compelling Opportunity for Small Caps

In our view, the current market environment presents a compelling opportunity for small-cap companies. Due to the valuation disparities that exist between large and small caps, and between public and private markets, we believe that small caps could potentially outperform their large-cap counterparts in the future. We believe improvements in conditions surrounding interest rates and inflation could further benefit small caps. Additionally, the resurgence of the IPO market, which fuels the small-cap segment more than any other cap segment with new companies, underscores the potential for significant returns and highlights that this may be an opportune time to invest in small caps.

1 IPO Trends: First Half of 2024 and Beyond, Stout, August 26, 2024, https://www.stout.com/en/insights/article/ipo-trends-first-half-2024-beyond

Key Points

- The market is once again expecting the Fed to aggressively cut interest rates in an attempt to salvage its economic “soft landing” and avoid a US recession.

- With this reset of interest-rate expectations, many investors are reevaluating their portfolio positioning, particularly across crowded trades, including the “Magnificent Seven” mega-cap businesses, artificial-intelligence stocks and US large-cap growth companies.

- We firmly believe that the days of free money are behind us and that companies and investors alike should consider this in their investment decisions.

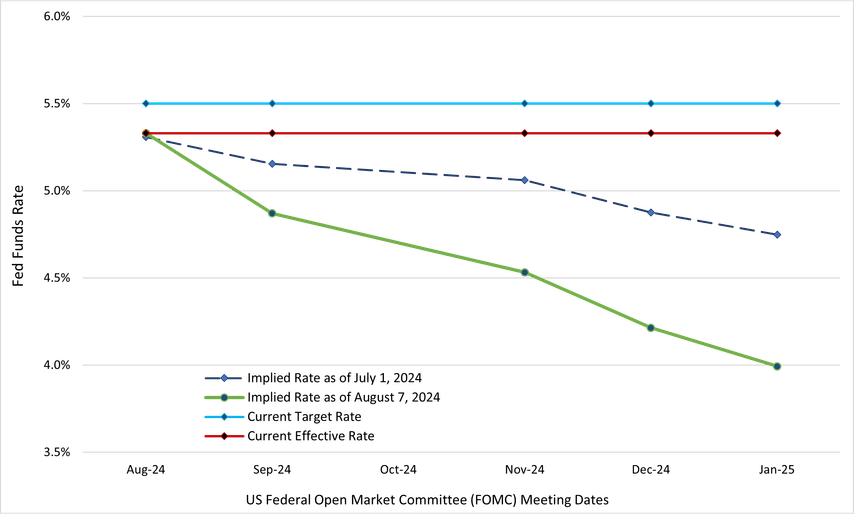

What a difference a month and a slew of fresh economic data can make. In early July, the market’s expectation for monetary policy finally started to align with the US Federal Reserve’s (Fed’s) guidance, following an extended period of dislocation. Cue the release of some softer economic data, and the market is once again expecting the Fed to aggressively cut interest rates in an attempt to salvage its economic “soft landing” and avoid a US recession.

Current Federal Funds Rate vs. Market-Implied Federal Funds Rate

Source: Newton Investment Management and Bloomberg, as of August 7, 2024.

A Swing in Equity Markets

With this reset of interest-rate expectations, many investors are reevaluating their portfolio positioning, particularly across crowded trades, including the “Magnificent Seven” mega-cap businesses, artificial-intelligence stocks and US large-cap growth companies. The readjustment has caused a meaningful swing across equity markets, with value outperforming growth and small caps outperforming large caps—a near reversal from the first half of 2024.

Relative Cumulative Returns Reverse in July

Source: Newton Investment Management and Morningstar, as of August 7, 2024.

A True Stock Market Rotation?

Is this the start of a true stock market rotation, or just a rebalancing? Time will tell. Meanwhile, we maintain our “balanced” approach to the market and value investing, particularly as the dispersion of potential outcomes remains quite high, in our view.

Stepping back from the immediate term, we believe that recent volatility can be partially attributed to a broader shift that the market and investors are making. This adjustment involves the ongoing normalization of inflation, interest rates and economic growth in the US—not to pre-pandemic levels, but to pre-global financial crisis levels. In other words, we expect inflation to be higher and more persistent than it was in the 12 years leading up to the pandemic, which may result in higher interest rates. Additionally, economic growth may regain some of its cyclicality, which had been depressed by extremely accommodative monetary policy. Speaking frankly, we firmly believe that the days of free money are behind us and that companies and investors alike should consider this in their investment decisions.

From an investment perspective, as fundamental, bottom-up stock pickers, we continue to view these macroeconomic factors through the lens of the companies in which we seek to invest. While we are undoubtedly monitoring the overall impact of macroeconomic events on the financial markets, we are even more keen to understand how these factors could affect individual companies. We are asking questions such as: how might our portfolio holdings perform if the Fed cuts rates once, or six times, over the next six months; how might a hard, soft or no landing for the US economy affect earnings and cash flows; and are we striking the right balance between offense and defense in the overall portfolio?

A Wider Dispersion of Returns

Similar to macroeconomic outcomes, this new environment is prompting a wider dispersion of returns among companies. As a result, we believe that fundamentals, valuations and business momentum should play a larger role in separating the winners from the losers. As always, we continue to favor companies sitting at the nexus of robust or improving fundamentals, attractive valuations and catalyst-driven business momentum.